Has Death Knell Sounded for MCX’s CurrentC?

MCX, led by a consortium of large retailers such as Walmart, Target and Best Buy, has announced it’s ending the beta test of its mobile payments service CurrentC, and accounts will be deactivated June 28. Although accounts will be closed, the CurrentC Website includes a cryptic message about its future. After thanking beta test participants in Columbus, Ohio, the site says, “Please stay tuned for new information on CurrentC as our future plans evolve.” In a customer Q&A, the site says: “We have not yet determined the future timing of CurrentC but we will keep you posted.”

MCX, led by a consortium of large retailers such as Walmart, Target and Best Buy, has announced it’s ending the beta test of its mobile payments service CurrentC, and accounts will be deactivated June 28. Although accounts will be closed, the CurrentC Website includes a cryptic message about its future. After thanking beta test participants in Columbus, Ohio, the site says, “Please stay tuned for new information on CurrentC as our future plans evolve.” In a customer Q&A, the site says: “We have not yet determined the future timing of CurrentC but we will keep you posted.”

Few in the payments industry were surprised by the latest announcement, according to Marianne Berry, managing director, payment insights, Auriemma Consulting Group. “Last October’s announcement that Chase Pay would incorporate some aspects of CurrentC was viewed as a life preserver for the faltering product,” she tells Paybefore. “Feedback from CurrentC’s pilot was not good. Consumers found the POS experience to be confusing and clunky.”

MCX was formed in 2012 and the CurrentC app has faced delays and several other mobile wallets beating it to market. Best Buy and Walmart announced April 2015 they would be accepting Apple Pay, although both retailers maintained they were still behind MCX. Then, some members began developing their own mobile payment services, such as Walmart; however, the retailer said it still supported the CurrentC project.

Walmart Pay, for example, is a symptom of larger problems with MCX and not a cause, according to James Wester, research director, worldwide payment strategies, IDC. Retailers have their own loyal customers, but those relationships have to be nurtured, “and those merchants can’t be expected to sit by idly, with their own resources underutilized, while MCX faces delays and problems. A partner-branded app like Walmart Pay was inevitable,” he notes.

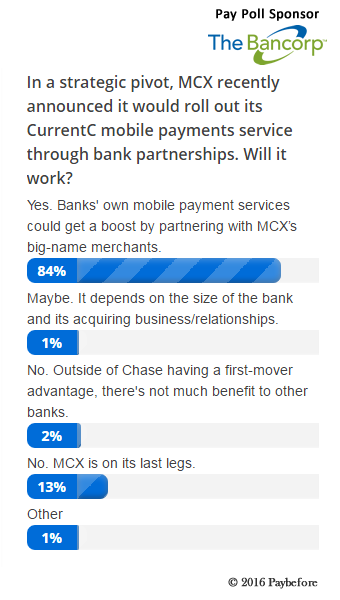

Last month, the retail group announced it was postponing CurrentC’s rollout (again) and turning its attention to agreements with financial institutions, such as its partnership with Chase. In a recent Paybefore reader poll on whether this bank-focused strategy would work, an overwhelming majority of respondents, 84 percent, said, “Yes.” The next highest response at 13 percent was “No. MCX is on its last legs.”

|

It’s been said that more can be learned from failure than achievement, so what’s the lesson here? According to industry analysts: Creating payment products is hard, but companies must move quickly.

Berry says CurrentC simply took too long to roll out and, in the interim, Apple Pay came to market. What’s more, “it was never clear why the consumer should want to use CurrentC. The impetus for the product was merchant dissatisfaction with payment card economics and data-sharing—concerns the consumer doesn’t really care about.”

Wester agrees MCX needed to hasten CurrentC’s rollout. “If you announce something, ship it quickly. If you can’t do that, don’t announce it,” he says. “Delays signal things no one wants to associate with payments: uncertainty, instability, etc.”

If this does mark the end of CurrentC, it joins other mobile payment ventures on the trash heap. For example, Softcard, launched by telcos AT&T, T-Mobile USA and Verizon, was acquired last year by Google, which promptly shuttered the mobile wallet app shortly after. Telco-backed wallets also have struggled in Europe, including O2 and Weve.

But like Paybefore readers, not everybody is ready to pronounce MCX dead. In a Paybefore Viewpoint published last week, Rick Oglesby, president of AZ Payments, wrote: “The deal with Chase is the key enabler for proving the value of the new network. If the collective organizations can work together to build a solution that benefits all parties involved, they can demonstrate the value of direct merchant-to-financial institution relationships and create a model that can be replicated across more and more banks.”

Related stories: