FTR 2015 – EU regulation with global impact

Marc Recker, Deutsche Bank, provides the lowdown on FTR 2015

What is FTR 2015 and how does it affect banks operating in the cross-border payments space? Marc Recker, Head of Market Management, Institutional Cash Management at Deutsche Bank, explores.

The challenges and complexities of complying with anti-money laundering (AML) and counter terrorist financing (CFT) regulations are certainly not new in the financial industry. Over the past few years though, the expectations of global regulators have increased considerably. The reputational threat as well as fines being levied, mean that financial institutions not only have to have comprehensive AML/CFT measures and solutions in place, but importantly they must be kept abreast of regulatory and legislative updates as well as best practices.

Interpreting regulatory updates sounds easy in theory, but at times there can be ambiguous terminology, different views of interpretation or certain grey areas. One of the most important regulatory topics currently related to money laundering and terrorist financing in the cross border payments business is the EU Funds Transfer Regulation 2015 (Regulation [EU] 2015/847), commonly referred to as FTR 2015.

What is FTR 2015?

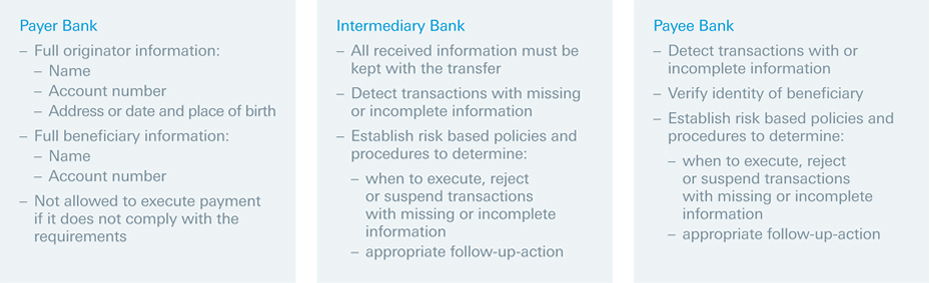

FTR 2015 lays down rules on the information on payers and payees, accompanying transfer of funds, in any currency, for the purpose of preventing, detecting and investigating money laundering and terrorist financing. These regulatory requirements apply as of 26 June 2017. It repeals the preceding Regulation (EC) No 1781/2006 (“FTR 2006”), thereby updating and extending those requirements. In particular, FTR 2015 imposes additional requirements on intermediary payment service providers, requires additional transmission of information on the payee, and sets higher qualitative standards on payment service providers to implement effective procedures to detect missing / non-sufficient information.

The European Supervisory Authorities (EBA, EIOPA, ESMA) are tasked with issuing guidelines on measures to be taken in relation to FTR 2015. In particular, with regard to the effective risk-based procedures payments service providers have to implement for determining whether to execute, reject or suspend a transfer of funds that lacks the required information. The consultancy phase is scheduled to start in September with guidelines expected in December 2016.

Does the FTR affect all banks operating in the cross-border payments space? What are the impacts?

FTR 2015 applies to all payment service providers (e.g. credit institutions, payment institutions, electronic money institutions) that are established in the European Economic Area (EU countries, Iceland, Liechtenstein and Norway). The terminology “established” refers to the location of the account maintaining unit, i.e. it is not relevant where the entity has its registered seat. Regionally, FTR 2015 applies to all payment transactions (domestic and cross-border) where at least one payment service is established in the European Economic Area (EEA). It is, therefore, important that financial institutions conducting fund transfers into or through the EEA acknowledge they are affected.

Are far as the impact is concerned, as long as today’s FTR 2006 requirements have been fully and consistently implemented the extended FTR 2015 requirements would require diligent but manageable implementation efforts. Non-consistent interpretation and implementation of FTR 2015 requirements in the market and by regulators, however, could lead to disruptions in payment processing. It is therefore very important to know the roles and responsibilities of actors within the payment chain and especially that of your correspondent bank as well as their approach.

Deutsche Bank’s view on implementation is to reduce complexity and to foster straight-through-processing. We will, therefore, to the fullest extent possible not make use of FTR 2015 exceptions that allow the sending of limited information (e.g. in case of not-linked transactions below €1,000) but instead will apply a maximum transparency approach.

In our role as a leading EUR and USD clearer we are obliged to establish policies to determine when to execute, reject or suspend transactions with missing or incomplete information together with follow-up action. However, unless there are exceptional circumstances, we will do our utmost to avoid rejecting or suspending a payment.

For the most part, the extended FTR 2015 requirements will not require substantial changes to processes. It is, however, important to keep in mind applicability as of 26 June 2017 as well as the aforementioned guidelines from the European Supervisory Authorities. Furthermore, collaboration between authorities, banks and their clients will be crucial to in order to gain consistent interpretation and implementation. Leading providers will be expected to take the initiative, demonstrate their thought leadership and provide guidance to clients as we move towards the deadline.