Blockchain in investment banking: simplification of systems and processes

Blockchain has the potential to greatly benefit the entire capital markets ecosystem. But the industry should learn to walk – when it comes this emerging technology – before it can run. Infosys’ Kashmira Ajgaonkar, senior consultant, and Swaran Kumar Patnaik, principal consultant, explore.

Blockchain technology is the use of cryptography and distributed messaging platform to share blocks of records or data in chorological chain and thus creation of shared ledger among trade counterparties for transaction verification and authentication purpose. Once the transaction is approved by all the parties to the transaction, the block of transaction will then get added under the chain.

In other words, blockchain is a database of transactions shared by all the participants who sign in the consortium or network. This shared database is simultaneously replicated on the computers/nodes involved in the consortium only after validating and agreeing to any changes or addition in the chain by all the parties.

Since blockchain uses cryptography at transaction level and is open for all to view/authorise; no single party can do any fraud. Blocks, so added leaves behind a digital trail which can’t be deleted; only can be altered or modified if required.

In capital markets, there are two major functional areas that can benefit from blockchain:

- trade reconciliation;

- KYC/AML procedures.

These are currently highly manual and time consuming. Real-time reconciliations/settlements of cash securities and sharing KYC information on blockchain can save a bank’s resources spent on manual processes and trade errors.

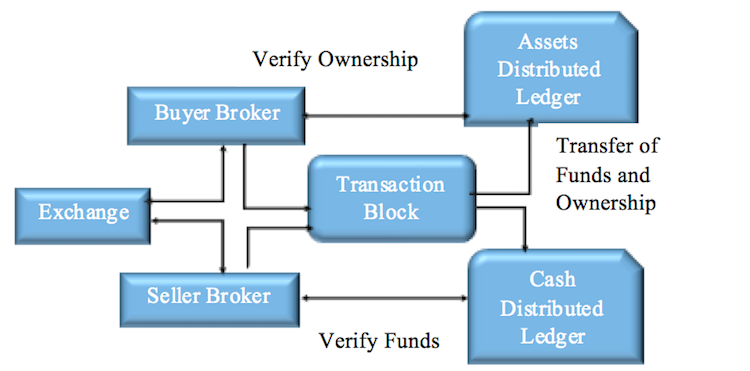

Reconciliations and settlements – spot transactions (equities)

The below diagram illustrates blockchain-based equity settlements where reconciliations can be done by both parties on the transaction block itself and upon agreement, transfer of funds and security can take effect.

Currently, there are many reconciliation tools available in the market, but resolving the conflicts in reconciliation at a later point in time is labor intensive and tedious process.

According to a recent report by Goldman Sachs, “Blockchain – putting theory into practice”, total global cost savings by use of blockchain technology for reconciliations of cash securities such as equity, repo and leveraged loans are expected to be $11-12 billion annually.

Process description on blockchain:

Process description on blockchain:

- Exchange will match the orders.

- Parties to the trade will mutually validate authenticity of each other to eliminate the counterparty risk.

- Reconciliation with counterparty can be done on transaction.

- Upon consensus, asset ledger will be updated with transfer of ownership and cash ledger will be adjusted for funds transfer.

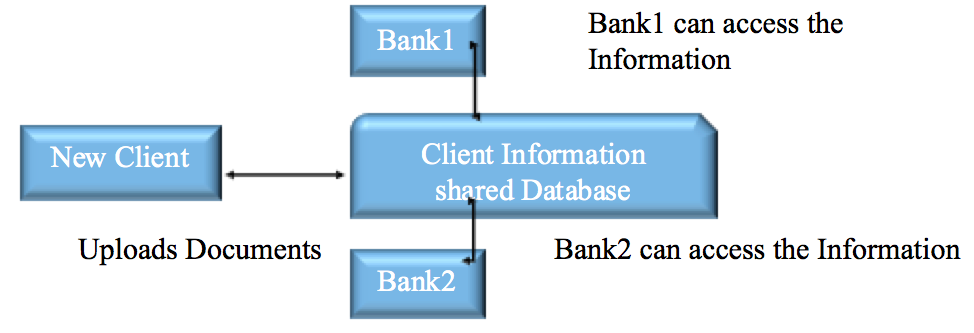

KYC and AML procedures

Every bank is mandated to perform its own KYC checks as per jurisdiction rules. Blockchain-based shared client database will help banks while onboarding a new client who has been KYC compliant by another bank previously. The bank can access the common documents and information uploaded by client in this database.

Transactions history available on the blockchain can also be monitored and in case of any AML suspicion, comment can be updated against the client in this shared database.

According to the aforementioned report by Goldman Sachs, total global cost savings on KYC and AML compliance by use of blockchain in this area are expected to be around $3-5 billion annually.

Process description on blockchain:

- Client will upload the KYC documents and information required in the shared database.

- Client will authorise Bank 1 to access the documents/information required for KYC.

- Bank can also update the comments against AML for the client.

- Client will authorise Bank 2 to view and access the documents/information required for KYC and also the comments updated by Bank 1.

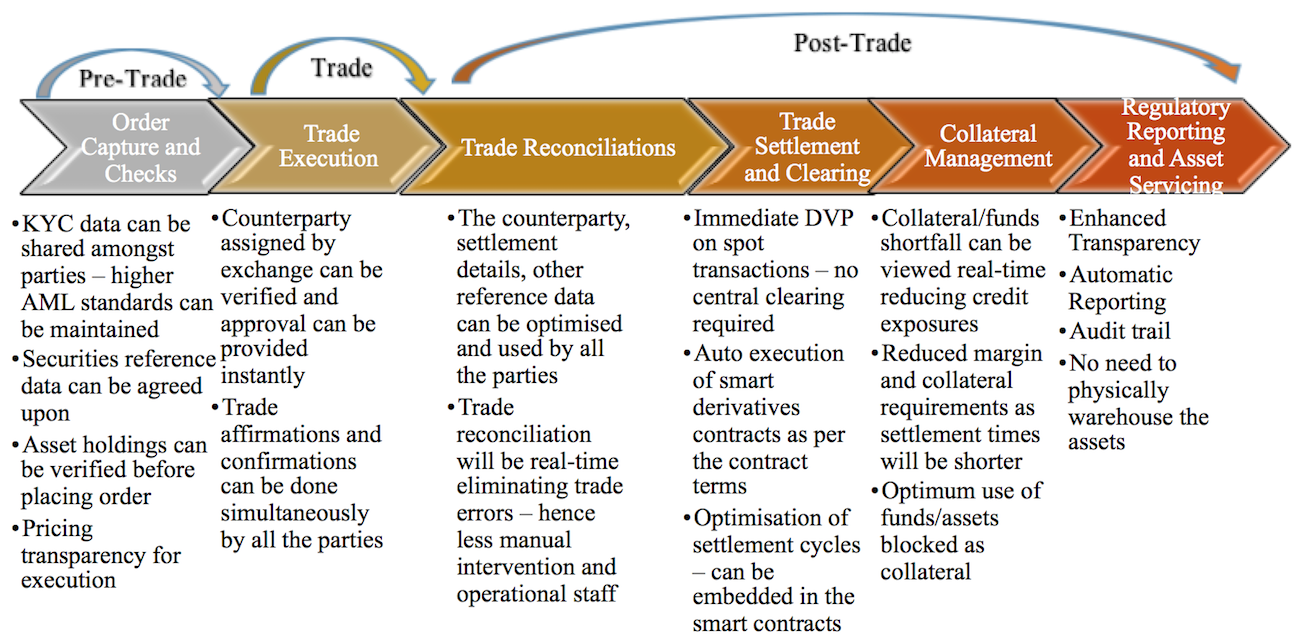

Deriving value

Multiple processes and systems across the trade lifecycle can potentially derive value from the blockchain implementation. It can deliver significant cost savings through simplifying the processes, reducing the need for third party intervention, deliver a quick/real-time verification process, reduce errors and enhance transparency and automation.

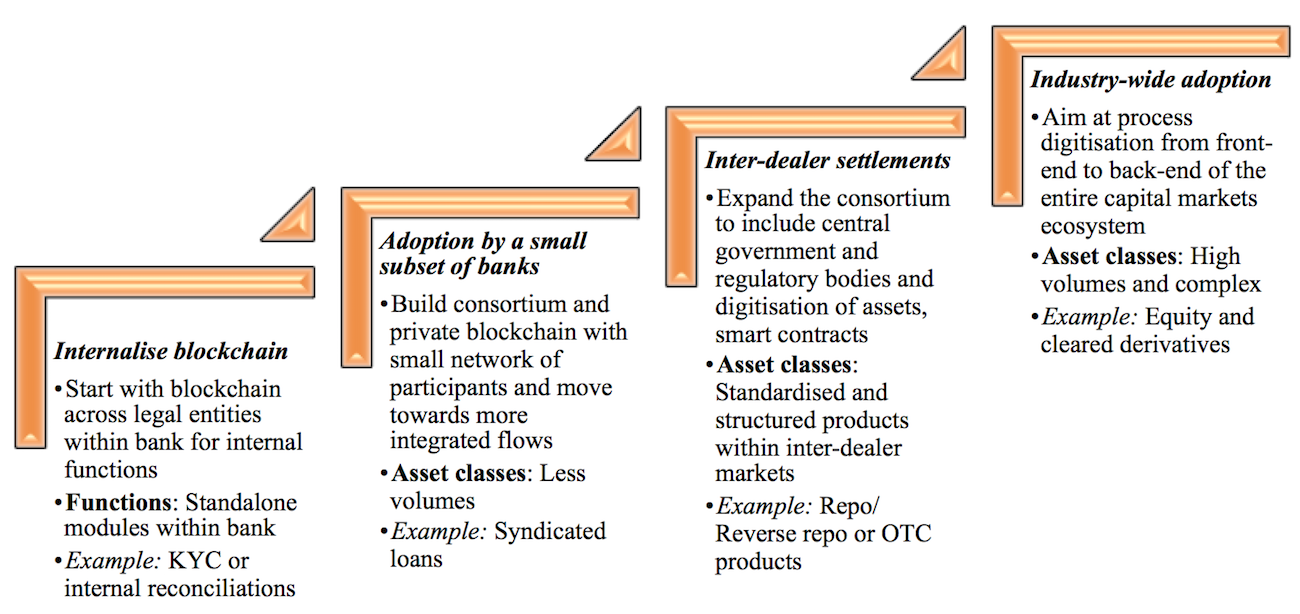

The way forward

Considering the complexity and regulatory uncertainty around it, banks will have to be cautious. Starting small with internal application of blockchain, banks can then expand it to other external participants at a later stage. A step-by-step adoption approach, experimenting with internal systems initially, focusing on lesser complex asset-classes first, and adopting an iterative model along the implementation phases, will aid a smoother transition.

In addition to the above, other areas which are critical during the implementation include the use of industry leading utilities, running a production parallel, using comparison tools, having a back-up plan and utilising cloud technologies.

These techniques ensure costs remain under control, clarity is gained and issues are uncovered at appropriate stages giving ample time to seek a calculated solution.