Citi Prepaid Talks Samsung Pay Rewards, Tipping Point for Incentives

Most of the talk around Samsung Pay’s new points-based loyalty program has been about whether it can spur mobile wallet adoption. But the in-app delivery of a virtual prepaid rewards card could mark a substantial shift for the incentives business, according to Brad Garfield, global product head for Citi’s corporate and public sector prepaid cards.

Most of the talk around Samsung Pay’s new points-based loyalty program has been about whether it can spur mobile wallet adoption. But the in-app delivery of a virtual prepaid rewards card could mark a substantial shift for the incentives business, according to Brad Garfield, global product head for Citi’s corporate and public sector prepaid cards.

“I don’t think of it as just driving mobile wallet adoption,” Garfield tells Paybefore. “I think of how it’s just the tip of the iceberg in the transformation of the incentives space—being able to deliver the payment directly into the mobile wallet experience without it requiring multiple steps.”

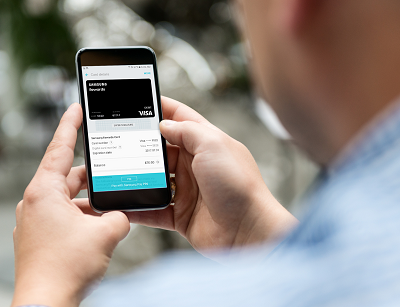

Citi Prepaid, a division of Citi Holdings, worked with Samsung Pay to launch the Samsung Rewards Visa Card, which is one redemption option for the new loyalty program. But as Garfield notes, it’s the instant delivery of the card into the mobile wallet that’s most compelling. And, given the Citi Holdings division’s pending acquisition by Germany-based Wirecard, virtual rewards cards have the potential to be implemented into mobile wallets globally.

The program with Samsung enables the device manufacturer and mobile wallet provider to motivate specific behavior—from buying a certain device or accessory to using the wallet more often—without any added steps for the customer to redeem their rewards. Samsung Pay users only need to read and accept the terms and conditions before they can spend the funds on their rewards cards. Additional funds can be added from new promotions and can be used at any merchant that accepts Visa and Samsung Pay.

“The first of its kind, Samsung Rewards is an exciting new opportunity for us to give new users a reason to try out the service while rewarding loyal Samsung Pay customers for using a service that they already enjoy. There’s even an option to redeem Rewards points with an instantly provisioned Samsung Rewards Visa Prepaid Card, offering consumers unmatched choice and flexibility as well as a frictionless experience,” said Nana Murugesan, vice president and general manager of services and new business at Samsung Electronics America. “It’s another way that Samsung—with unwavering support from our partners, like Citi—continues to drive innovation in the digital wallet experience, while cementing its place in the broader Samsung mobile ecosystem.”

Until now, consumers could add rewards cards to their mobile wallets manually (if the issuer was supported in the wallet), but that extra step creates unnecessary friction, according to Garfield. Instant card provisioning will be transformative, he predicts. And he doesn’t think it will take long to drive up to 50 percent of the company’s incentive card volume to the mobile wallet.

“We’re focused on the user experience and how we can help our corporate clients pay someone faster. We know that if you can tie the desired action more directly to the reward, you’re better able to drive behavior,” Garfield says. “If there’s no delay in the delivery of an incentive payment, that helps close the loop.” Not only does speed help Samsung achieve its objectives, but with added promotions and deals, the company can drive customers to key channel partners, potentially adding a revenue stream.

“What we’re finding with Samsung is that [the company is] seeing the majority of spend at some of [its] key retail partners,” he adds. To top it off, customer service calls are a fraction of what they are with a typical plastic card-based program, Garfield says. That’s because there are no calls to activate the card or to check balances. The virtual card can be used immediately, and balance and transaction details are available in the mobile wallet app.

“This changes the paradigm of the consumer incentives industry, which largely has been based on a breakage model,” says Garfield. “We are actively trying to change that and move to a model that’s based more on spend back to clients and channel partners, and having that become the revenue source. With virtual cards delivered directly to a mobile wallet, we can provide an incentive program at a lower cost, with faster delivery and more effectively direct the spend, all while ensuring a great consumer experience. Being able to do that with any mobile wallet is something we’d like to accomplish.”

That may seem like a lofty goal, but once Citi Prepaid is integrated with new parent company Wirecard, it will be able to help corporate clients reach a vast number of consumers via the mobile wallet channel. Wirecard supports several mobile wallets, including its Pay Award-winning Orange Cash in Europe, is integrated with Apple Pay and has successfully launched its own mobile payment brand boon., which is a host-card-emulation (HCE)-based solution in various European countries.

But how would clients reach customers who don’t yet use a mobile wallet? Garfield says the client could integrate an HCE solution within its own native app leveraging Wirecard’s software development kit (SDK) and APIs, or default to a plastic card for those who don’t have an eligible mobile device.

One reason the Samsung Pay partnership works so well is because the target customers are Samsung Pay users. But as mobile wallets gain momentum, Garfield believes the opportunities for instant card provisioning to those mobile wallets will only get bigger. Eventually, the opportunity could extend to other corporate payments, such as payroll cards when ATM acceptance of mobile wallets reaches scale, Garfield suggests. “Our partnership with Samsung Pay is just the beginning,” he says.

Related stories:

- APEX Interview Series: Brad Garfield, Citi Prepaid Services, on Customers Driving Prepaid Innovation

- Wirecard Stakes Claim in North America with Citi Prepaid Buy

- Viewpoint: Virtual Reality