Analysis: the trend toward best practice in institutional FX settlement

Marisa Kurk, senior managing director and COO of Mesirow Financial Currency Management group, explores best practices in foreign exchange (FX) settlement.

Since its inception in 2002, the merits, usage, and popularity of the CLS settlement service have risen substantially. CLS remains consistent in its original approach; gathering the support and usage of the global bank community to provide a centralised, real time, payment-versus-payment (PvP) settlement network that allows for streamlined, straight through processes and protection from settlement risk for FX trades.

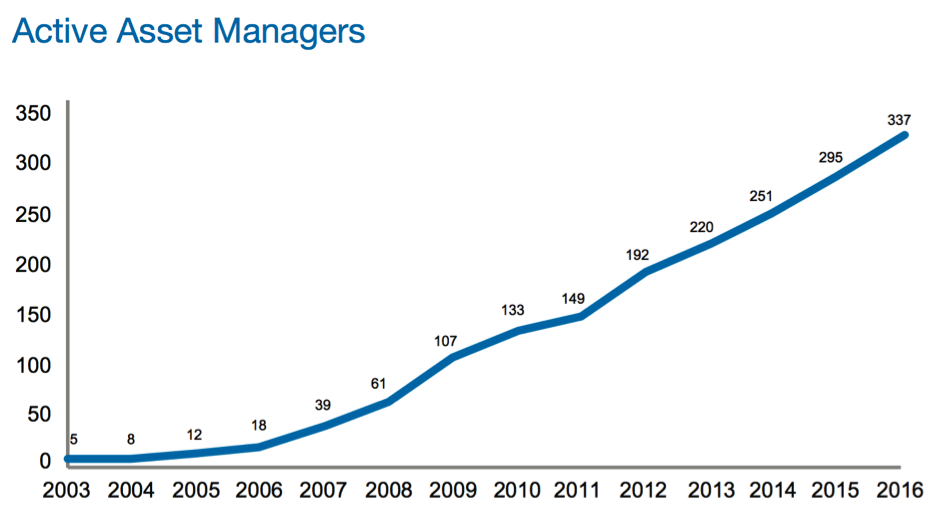

In particular, the CLS system has been widely adopted and promoted by the asset management marketplace. According to internal CLS statistics, in 2003, just after the launch of CLS, five asset managers participated in CLS. In 2016, the number had increased exponentially to 337 asset managers.

CLS third party asset managers data refers to any non-member asset manager that has settled in CLS in the past 12 months

The statistics surrounding the rise in adoption of CLS speak for themselves. However, the rationales behind these statistics deserve further discussion. To begin with, the traditional benefits of centralised settlement risk mitigation have become well established in the industry.

In the early years of CLS, the case was still being made for the basic tenets of enhanced CLS protection – reduction of operational settlement risk, enhancement of straight through processing, less time and economic savings these bring. Nearly 15 years later, these basic benefits are well known and well accepted by the industry.

As we head midway into the second decade of CLS, asset managers and large funds alike are seeing enhanced benefits of using CLS’s PvP service for their FX settlement beyond these original tenets. One cannot begin this discussion without acknowledging that the trend toward asset globalisation and higher foreign content in domestic portfolios continues to rise, raising the profile and need for FX transactions and hedging within institutional portfolios. Yet beyond the rise in popularity of foreign investments and the traditional benefits of CLS, additional reasons and market trends have encouraged the adoption of CLS and have established it as best practice for FX settlement.

CLS for currency management

While it is commonly understood that CLS may be utilised as a mechanism to mitigate settlement risk for deliverable foreign exchange forward transactions, the asset management space has also adopted the use of CLS for currency forwards that are being rolled so that they may collect the profit and loss and forego the actual intake of the deliverable currency.

For those who are not familiar with the overall mechanics of CLS versus the manual settlement process, it is important to understand that when a trade is scheduled to be settled outside of the CLS system it is confirmed with the bank counterparty at the time of execution. Further processing is then required prior to settlement to deliver those specific settlement details and instructions with the specific bank counterparty on the other side of the trade. However, when a trade is scheduled to settle via the CLS system, all necessary trade details are tagged at the time of the trade confirmation and no further instructions are required prior to settlement.

The CLS process is centralized regardless of trading counterparty, unlike processes outside of CLS which are often entity specific. Although the risk of a mismatch of PvP exchange in the case of gross settlement is obviously not present in situations where a contract is rolled forward, the mechanics of the settlement tagging at the time of trade confirmation and pre-processing in advance of the settlement are just as applicable here. Additionally, asset managers will notice that the operational efficiencies and straight through processing benefits of CLS are still applicable for these operations. Accordingly, CLS use has been further adapted for this extended use case.

Broader counterparty rosters

A secondary reason for the increase in adoption of CLS is the heightened market awareness of the benefits of counterparty diversification when looking at both counterparty risk and the pursuit of best execution. Settlements outside of CLS often require manual processes tailored to each counterparty bank for each settlement per bank and per value date.

Using CLS enables a participant to employ a broad counterparty roster with far greater ease. Specifically, using CLS allows for uniform processes and no specific per-counterparty instructions in preparation for settlement. Including additional banks to a counterparty panel requires no additional workflow when settling via CLS. Accordingly, market participants can easily set up rosters of several, if not dozens of counterparty banks, when opting for settlement in CLS. This broader roster gives market participants the flexibility to pursue their own unique counterparty risk metrics and allows a fuller roster of banks to compete for each transaction.

Focus on best execution

The increased importance of achieving best execution and further scrutiny of all components of transaction costs within the FX marketplace is yet another consideration. Using CLS allows execution agents to transact each trade more competitively, which can result in lower transaction costs. This is not only achieved by being able to set up a broader panel of counterparty banks as highlighted above, but by allowing for true competition on each trade, even when a position is opened at one bank but it is found to be more beneficial to close the position or roll it with a different bank. This is made possible as CLS allows custodians to accommodate multilateral netting at a client level and not just at an individual bank level when settlements occur directly instead of across the CLS system.

When using CLS, custodian banks can allow clients to net their total required payments at the CLS level, not the bank counterparty or lower level, resulting in broader option sets with each transaction. This option and opportunity for cost savings can also be seen when positions need to be moved from one bank counterparty to another. Again, when transactions settle via CLS, positions can be opened at one counterparty bank and closed at another without the additional layer of trading and costs. As new global regulations increase requirements around achieving best execution, the need for additional tools such as CLS become even more important to the marketplace.

Further CLS considerations and conclusion

While the many benefits of CLS are undeniable, there are still a few considerations institutions need to weigh to determine if CLS is appropriate for them. First, a client’s individual custodian is the transacting party which makes settlement via CLS possible.

Often there are additional custodial charges for using CLS. This is dependent on the custodian and individual client package and agreement. However, custodians may choose to waive these fees, as they benefit from reduced operational risk. Custodial charges for CLS may also be quite nominal when compared to the pricing of CLS charges on the overall transaction price. However, it is a cost that should be evaluated.

Another factor to consider is that not all currencies are eligible for settlement in CLS. Accordingly, for clients that have both CLS and non-CLS currencies, two processes may be needed for settlement. Clearly the wide spectrum of benefits will still be realized for CLS currencies, but plans and managers in such situations will have to accommodate two different processes, those for CLS currencies and those for non-CLS currencies.

Fifteen years after its inception, CLS has seen its adoption and acceptance rate grow. The additional benefits of using CLS have increased awareness and demand among many institutional asset managers and clients who see CLS’s PvP settlement as part of their best practices in FX management.

Some participants have gone so far as to make it a mandatory requirement in managing FX. The continued market trends of enhanced risk mitigation across an ever-broadening spectrum, further attention to counterparty selection, best execution and transaction costs make CLS’s role in the FX market increasingly important moving forward.

As the FX marketplace continues to evolve, CLS will continue to play a more central role for best in class operations.

About the author

About the author

Marisa has nearly 15 years of FX experience, delivering industry best practices to client portfolios, provides strategic risk management insights to clients, and managing specialized counterparty, legal and regulatory risks.

As COO, Marisa also oversees the functions of client service including the provision of client reporting as well as client and prospect material. Marisa received her Master’s Degree in Finance at DePaul University Kellstadt Graduate School of Business.

She graduated with a BA in Economics from Eastern Illinois University and was a member of the Departmental Honors Program for Economics.

About Mesirow Financial Currency Management

As a leading, independent currency specialist, Mesirow Financial Currency Management delivers innovative, customised currency risk management solutions to institutional clients globally. With the expertise to provide objective, strategic advice, Mesirow Financial partners with our institutional clients to implement best practice currency risk programs for their unique set of circumstances.

Mesirow Financial delivers a full range of currency risk applications – passive and active risk management – customized to suit a client’s particular context and objectives. Our team of currency professionals has a broad depth of experience across areas of portfolio management, trading, operations and client management.

The solidity of the team, combined with access to senior professionals is highly valued by clients, ensuring long-standing, strategic relationships.