How blockchain could change the global remittance industry

Alex Koles, Evolve: the scope of blockchain for remittance is increasing in emerging markets

Blockchain technology is replacing the current centralised business model of the financial services industry. Banks and financial institutions are exploring ways to implement blockchain tech to reduce transaction costs, increase transaction speed, eliminate multiple transactions and mitigate fraud.

Cryptocurrencies promise to provide an innovative solution to the current issues facing the remittance market. The most widely used cryptocurrency is Bitcoin, though competitors such as Litecoin, Ethereum and Ripple also operate in the global payments landscape. The prospect of a fast, secure, low-cost and genuinely international payments system is encouraging businesses and individuals globally to consider the benefits of cryptocurrency settlement.

Blockchain technology can speed up and simplify the cross-border payments process, cutting out many of the traditional middlemen and making money remittance more affordable. Until now, the costs of remittance were approximately 5%. However, blockchain reduces the transaction costs to less than 1%. More importantly, blockchain provides guaranteed, real-time transactions across borders, reducing the risk of loss due to currency fluctuations.

Banks and fintech companies are exploring the use of blockchain technology and cryptocurrencies for cross-border payments.

Banks and fintechs are considering the distributed ledger technology (DLT) as the backbone of a new cross-border payments infrastructure to solve inefficiencies and provide faster, more affordable services.

Banks have great incentives to experiment with and implement blockchain technology in their current remittance systems. Transactions on foreign exchange markets alone total $4.8 trillion daily. And according to World Bank statistics, global remittances will grow to $616 billion in 2018, up from $601 billion in 2016. Remittances to low- and middle- income countries are expected to grow to $466 billion in 2018, an increase of $25 billion from 2016. A reduction of costs in cross-border payments by just 5% will result in $16 billion in annual savings.

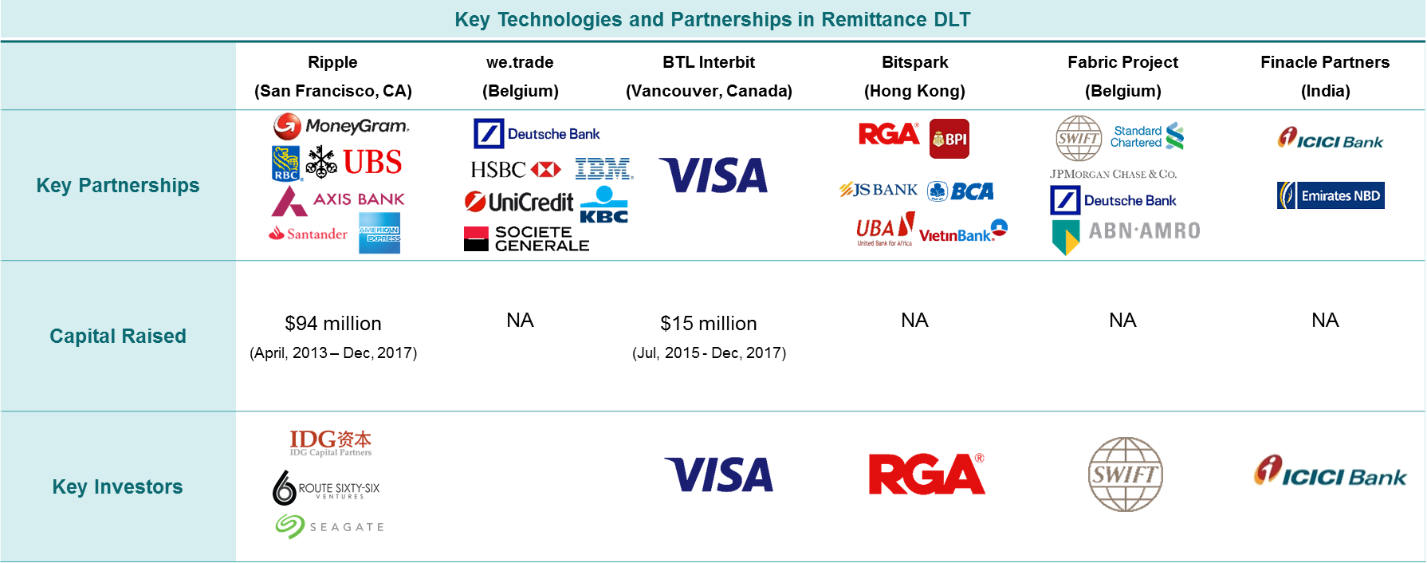

Development of innovative technologies, such as Ripple’s cryptocurrencies (XRP) and BTL Group’s Interbit platform and cryptocurrency BTL, represent a real threat to the legacy Swift interbank payment system. Ripple (XRP) is a real-time gross settlement system, currency exchange and remittance network created by the Ripple cryptocurrency that acts a bridge currency to enable instant and nearly free global financial transactions of any size. BTL Group’s Interbit is an enterprise-grade private blockchain development platform that powers the cross-border settlement solution in collaboration with Visa Europe. BTL Group’s solution also allows high volume and high-velocity simulations of cross-border transfers. Visa and BTL are now inviting a small number of European banks to participate in the project and test the solution.

Recent examples of banks experimenting with blockchain technology in their bid to replace legacy payment systems include:

- Since January 2017, seven major European banks, along with IBM, have partnered on a new blockchain-based permissioned trade finance platform, Digital Trade Chain (DTC). This platform will manage open account trade transactions from initiation to settlement for both domestic and international commerce. Recently, Spain’s Santander joined the partnership. The eight founding banks established a joint venture called we.trade to rebrand the platform for an international launch.

- Santander is the first bank in the UK to use blockchain technology to transfer live international payments through a mobile app. The solution uses technology provided by Ripple, the creator and developer of the blockchain-based Ripple payment protocol and exchange network.

- A host of other major banks, including UBS, Royal Bank of Canada (RBC) and National Bank of Abu Dhabi (NBAD), have adopted Ripple to improve their cross-border payments. They view Ripple’s payment protocol and exchange network as a valid mechanism for offering real-time affordable money transfers.

Ripple is one of the most widely used blockchain technologies for cross-border payments. Banks can confirm and validate cross-border payment details in real-time prior to initiating a transaction through a “permissioned ledger” in Ripple’s technology which requires legal entities to validate transactions. The banks can then confirm delivery at settlement through end-to-end tracking. More than 100 financial services firms, including American Express, Santander and MoneyGram, have entered into agreements to use Ripple’s technology.

Source: CapitalIQ, PitchBook

Blockchain technology for remittance increases transparency and safety.

Fraud is a substantial problem for the financial industry. One of the significant advantages of blockchain technology is the challenge it presents for hackers and fraudsters to penetrate the system. Transactions on the blockchain are fixed making fraudulent attempts to change them easy to detect. The links between the blocks and their content are protected by cryptography so previous transactions cannot be destroyed or forged.

Currently, cross-border payments are conducted through a network of correspondent banks or money transfer providers. There is no central clearing system for these transactions and they can only occur during bank business hours. They are also subject to processing fees from multiple intermediary banks involved in the transfer process. Money transfer operators (e.g. Western Union) are available as a costlier alternative for faster international transfers.

Blockchain technology addresses the cross-border payment issues described above. Based on DLT, a public ledger where every transaction that occurs on the network is recorded, identical copies of transaction records are maintained on each of the networks’ computers. All parties can review previous entries and record new ones. The transactions are grouped in blocks and recorded sequentially in a chain of blocks, hence the name “blockchain”.

Cross-border remittances using blockchain technology enable both the sender and recipient to know exactly where their money is. There are no lags during the transfer process because the decentralized blockchain technology effectively removes the intermediary banks and also provides guaranteed, real-time transactions across borders.

Emerging markets are primed to benefit from blockchain technology in their prospering remittance markets.

Remittances are a central pillar for the population in many Asian economies. The remittances sent by migrant workers in developed countries to their home countries in emerging markets made up a large portion of many Asian nations’ GDPs. The World Bank estimates migrant workers sent $450 million back home in 2017. However, analysts believe that $32 billion in remittances aren’t even sent because of high transactional and regulatory costs associated with cross-border money transfers.

Blockchain technology is fast-emerging as the solution for safe, quick and cost-efficient money transfers in the Asian remittances industry. Some of the innovations taking place in emerging markets will result in reduced costs and increased efficiency for international remittances. We see this momentum in several areas:

- In Papua New Guinea, the central bank is exploring blockchain technology and cryptocurrencies to overcome previously insurmountable technological hurdles and widen the financial services choices available to its people.

- Hong Kong-based remittance platform Bitspark announced a partnership with Reinsurance Group of America, Inc (RGAx). The two companies will offer insurance services to underserved markets. Both companies also emphasized their desire to use blockchain technology to provide remittance services, including cash-based, to emerging markets.

- Toast, a Singaporean remittance start-up, raised $850,000 in a seed funding round led by Aetius Capital and ACE & Company, a private equity firm also known for investing in financial comparison site CompareAsia and online payments start-up TransferWise. New York-based investment firm One Zero Capital also participated in the round.

The scope of blockchain for remittance is increasing in emerging markets, which are characterised by low banking penetration, strong demand for financial services, high levels of mobile penetration, and a less-developed financial infrastructure. Together, these conditions can be a powerful catalyst for the adoption of blockchain-based financial solutions that boost financial inclusion and growth across many capital markets globally.

By Alexander Koles is CEO, founder and managing director of Evolve Capital Partners, a specialised investment bank focused globally on industries at the intersection of finance and technology

How does a person manage a remittance if there are no, or few banks? How do they get money into the blockchain? IE; Cash-in. How does the receiver get it back out?

great content useful to all the aspirants of blockchain !