Why blockchain could revolutionise trade finance documentation

Michael Hogan, MUFG

After beginning life simply as the technology that underpinned Bitcoin, the last four years have seen blockchain go through a metamorphosis.

Today, it’s considered by many to be the future of financial technology and continues to be the subject of deeper exploration and understanding, as evidenced by many new and ongoing proofs of concept. The terminology for the technology has also evolved. blockchain was used to reference the Bitcoin ledger and is still commonly used as a popular catch-all term. However, the term ‘distributed ledger’ is more accurate. Blockchains are one form of a distributed ledger, not all of which employ blockchain in their format.

Chris Harrison, MUFG

The technology has the potential to disrupt traditional business models by removing the need for complex reconciliations or trusted centralised counterparties and third parties, as all parties in the network derive their position from a single source of information agreed by that network. The costs of developing, maintaining and operating multiple proprietary systems are therefore removed.

It also challenges established ways of recording and transferring ownership and value, and in doing so provides opportunities for significant efficiency and further cost gains.

New platforms have been heavily influenced by financial service providers and a desire to efficiently match corporate needs with the benefits provided by a single source of transparency and certainty.

Evolution of the distributed ledger solution

The blockchain underlying bitcoin is an example of a “permission-less ledger”, where anyone can join, conduct and/or verify transactions. The ledger is open for all to see (it’s also possible to have a “permissioned ledger” that requires a party to have authority to join the network).

With both types of ledger, transactions and data are shared across the entire network; neither ledger supports private transactions.

As more and more businesses explore using a distributed ledger solution, hybrid solutions are also flourishing. These are bridging the gap between what corporates need to conduct business and the original benefits of the blockchain technology; solving the issue of information access while retaining the benefits of trust and reconciliation.

One example is the development of smart contracts. The need in many cases for access to full data to only be allowed to those involved with a transaction has led to the development of smart contracts that define which parties can perform certain parts of the transaction. This is a clear departure from the original transparency to all provided by distributed ledgers and marks how the technology is evolving to suit business needs.

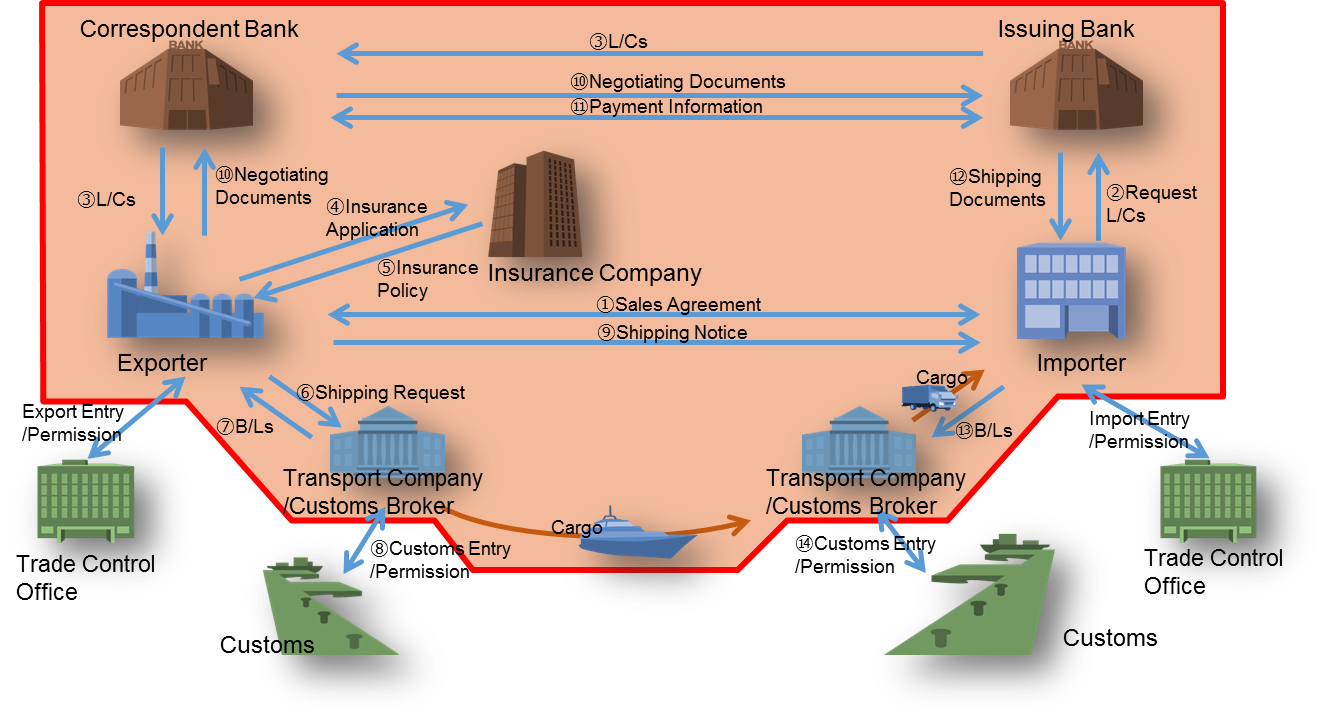

Revolutionising paperwork

It has long been accepted that the trade finance industry is ripe for digital development. The current centuries-old practice (see diagram A below) still relies on paper documentation to evidence the contact of sale and the movement and ownership of goods/services. This in turn requires the manual exchange and checking of paper documentation by a series of parties before a related but separate settlement can be made.

Diagram A

Diagram A

These processes suffer greatly from built-in inefficiencies and it is not surprising at all that escrow payments, trade finance and processing and document store have all been identified as potentially benefitting from the application of blockchain. Fuelled by smart contracts to mediate payments, goods delivery and shipment updates, an new solution is being crafted by the industry, which is much more suitable for modern day trade financing.

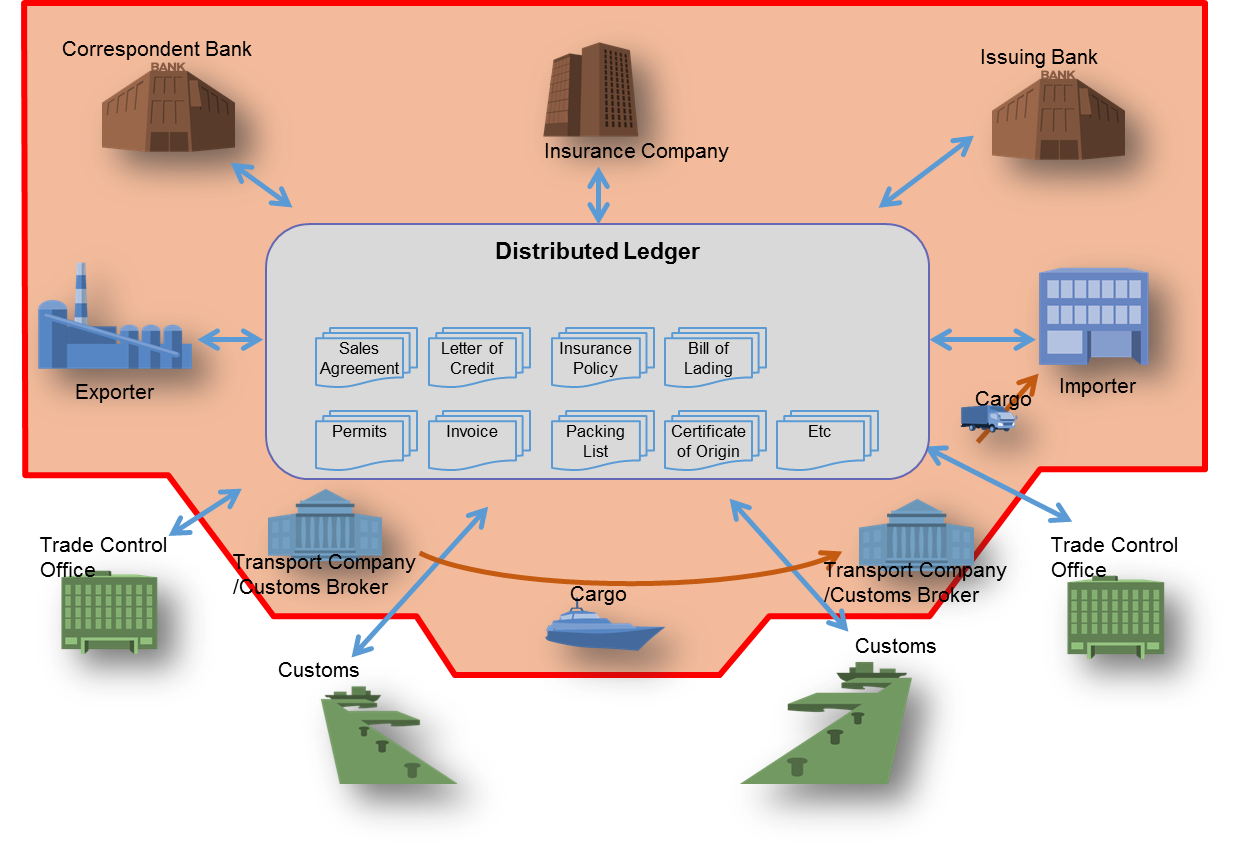

Corporates, banks and financial technology companies are now endeavoring to develop proof of concepts (POCs). These efforts are concentrated on using smart contracts to digitalise trade documents and registering these new documents into the blockchain or distributed ledger (see diagram B below).

Diagram B

Nor does it need to stop there. The use of blockchain can also be used for asset transfer, fraud prevention, know your customer (KYC) routines and anti-money laundering (AML) programmes.

Adopting blockchain within the trade finance ecosystem will reap significant benefits including:

- a single source of truth on a distributed ledger;

- improved operational efficiency for corporates, banks and all parties in the ecosystem;

- provision of greater comfort for liquidity providers to finance transactions.

And while blockchain solutions for trade finance are still at an early stage, there are already important lessons that can be made.

- There is a need to have a common standard given that trade finance documents come in various forms and there are different platforms with different standards. This is a practical, yet important, issue when it comes to the commercialisation of the technology. The International Organisation for Standards (IOS) has already appointed a committee to develop these standards, prioritising the following areas: digital currencies, trade finance, remittances and commodity exchange.

- Despite the fact that new networks could improve the operational efficiency, many corporates, logistics companies and banks in the trade ecosystem may have to change their systems and processes to adopt the new technology. This will take time.

- There is a need for collaboration. Financial services are currently leading the field; of the current 40 global consortia, 26 are from financial services. Each consortium is focusing on its own ways of use and proprietary code or working with existing public blockchains or permissioned ledgers with vendors. Many are facing similar challenges at different stages or their development.

- While blockchain per se may deliver solutions to reduce or eliminate the need for legal and regulatory oversight, where trade finance transactions are involved parties will still need clarity regarding statutory protection of their rights and obligations. This will inevitably involve the Central Banks to ensure that the trade ecosystem is able to operate without raising any regulatory concerns.

As the technology journey continues, it is likely that more solutions will evolve to marry the benefits originally promised by Bitcoin and blockchain with the pragmatic needs of the market.

However, the technology still needs to be tested for volume, scalability and security in a live environment. Some concepts are expected to go live this year, but mainstream use remains further off.

Standards, regulation and a network all need to be fully achieved before the technology achieves widespread adoption.

By Michael Hogan, regional head of transaction banking, and Chris Harrison, regional director of transaction services, MUFG