The five attributes of a successful digital banking experience

In a time of rapid advancement in technology, channels and customer expectations, how do you maintain a competitive advantage? In large part, the answer will come down to mobile and digital services.

Those that get it right will increase engagement, loyalty and brand awareness. Those that get it wrong might alienate and drive away customers.

Current and future customer expectations

A clear view into how well banking providers are meeting the needs of their customers can be found in an annual survey by global financial services technology provider FIS.

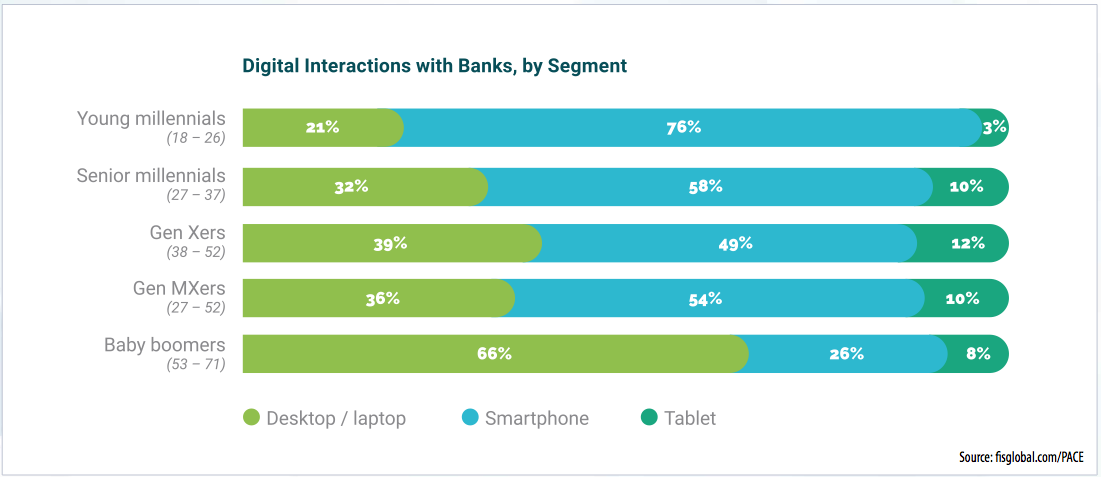

For the 2018 “Performance Against Customer Expectations (PACE)” report, FIS surveyed more than 1,000 UK consumers. Mobile banking was identified as the main branch: Most consumers between 18 and 52 turn first to their mobile devices when interacting with their bank.

The five attributes of digital success

But what factors need to be considered to create powerful digital self-service apps and similar differentiators?

Ahead of everything else is 24/7 borderless convenience, which means relevant services, any time, anywhere. For digital customers there can be no equivalent of a queue.

That convenience stems from the design of the app but also from slick operations in the background. For standard and cumbersome processes including KYC and AML, artificial intelligence (AI) now allows real-time verification of various documents, potentially using third-party systems. By so doing, banks can optimise the customer experience and significantly reduce costs and time-to-market.

This brings us to the second attribute: data aggregation. It is key to create a highly personalised financial management experience. Many customers want a consolidated, single view to manage their finances. Personalised tools enriched by AI-supported analytics mechanisms are becoming a prerequisite to support financial planning.

With open APIs, financial information from multiple sources – including third-parties – can be combined efficiently. For instance,

Slovakia-based Tatra Banka, a subsidiary of Raiffeisen Group, has launched a third-party application for mobile on-boarding, claiming it is up to 70% faster than standard bank operations. Using machine learning, neural networks and biometrics, the images on identification documents are matched with uploaded photos of the customers. Using the devices’ cameras, the biometrics technology scans customers’ eye movements, facial features, and light conditions and authenticates their identity.

More generally, the back-end also plays an important role. “The winners will be institutions with an API-ready core banking architecture that integrates with components on a plug and play basis,” says Christian Höpker, head of digital, Europe at FIS. “With the updated Payment Services Directive – PSD2 – platforms that allow aggregation and the integration of third-party services are essential for digital banking.”

This means harnessing the potential of the third attribute – Open Banking. With consent for access to data by verified third-parties, customers can benefit from more information and tools to optimise their financial services, carry out faster transactions and receive recommendations based on their specific financial circumstances.

BBVA, for instance, recently became the first bank in Spain with products from different financial service providers on its app. BBVA’s tool uses the income and spending of users to provide analysis of their finances. The capability now spans other accounts, cards, investment funds, pension plans, deposits, securities, mortgage and consumer finance products.

Pushed by PSD2, security is the next attribute to focus on. The directive requires physical security, access control as well as data and systems integrity and confidentiality – aligned with GDPR and its reinforced data protection guidelines. Preventive security measures are to be established, as well as multi-layered controls such as four-eyes principle and two-factor authentication. With these measures in place, even cautious consumers should recognize that open banking-related benefits finally outweigh its risks.

A proper combination of the above attributes can significantly increase a bespoke banking experience. Advanced analytics enable a deeper understanding of customer behaviour and facilitate customized offers. New services may include tailored dashboards, leveraging themed animations and relevant third-party data to keep the banking experience interesting and engaging.

Finally, there needs to be consideration for the wider and visionary customer experience. Banking has started to move to the centre of society. The inclusion of social content improves the customer experience and loyalty, covering integrated videos or help from customer forums, as well as social platforms for customers to share their own experiences.

The next level is likely to be “invisible banking”, making banking a seamless part of life, such as by leveraging voice banking applications that don’t require a single touch on a device to manage personal finances.

All steps should be done strategically. KPMG advises (“Forging the Future” report, 2017), to have “a clear fintech strategy that aligns to organisational objectives, considers current assets and capabilities, and includes an execution plan for addressing gaps and managing a transformation that may never have a defined end-point as fintech will continue to evolve”.

Conclusion

As with any trend, there are threats and opportunities. This is nothing short of a consumer-led revolution and those banks that do not embrace it will lose. Loyalty has to be earned, not taken for granted.

It could be argued that the most likely losers are large, branch-centric banks, but it isn’t that black and white. Major banks are only too aware of the threat. A global survey by KPMG of more than 160 financial institutions

concludes: “Whether it’s providing new ways to enhance the customer experience, responding to regulatory change, underpinning new payments or digital delivery models, making service delivery faster and more cost-effective, or improving the efficiency of back-office functions – the myriad fintech solutions now available, or in development, are helping to rapidly reinvent the entire value chain of financial services.”

Increasingly large banks are nurturing, partnering or buying innovative fintechs and providing similar services. An alternative model is to create a digital offshoot bank within the parent bank brand.

FIS’s Christian Höpker concludes: “The likelihood is that many of the new entrants will be consumed by other banking organisations. Established banks will respond and rise to the new challenges, but some inflexible organisations also might disappear. Open APIs enable financial institutions to embrace fintechs rather than competing with them, as well as to offer new services to customers quicker and not wasting too much of their own capacity.”

This article is also featured in the November 2018 issue of the Banking Technology magazine.

Click here to read the digital edition, it is free!