Why is digitised cash better than stablecoins?

Since the birth of the first cryptocurrency, Bitcoin, many have sought to unlock the promise of the underlying technology innovation to streamline national currency transactions. With global payments annual revenues estimated at $1.9 trillion according to a 2018 McKinsey report, the potential prize for those who can do so is massive.

Future work in digital identity may lead to additional features and functionality.

The underlying technology is distributed ledger technology (DLT). Many of the earliest efforts to apply DLT – including blockchain, which is one form of DLT – focused on using cryptocurrencies to circumvent established payment rails. Though attractive for those who want to stay anonymous, this approach soon revealed an inability to comply with regulations. The concept of a stablecoin was born.

Let’s make transactions more complicated – not.

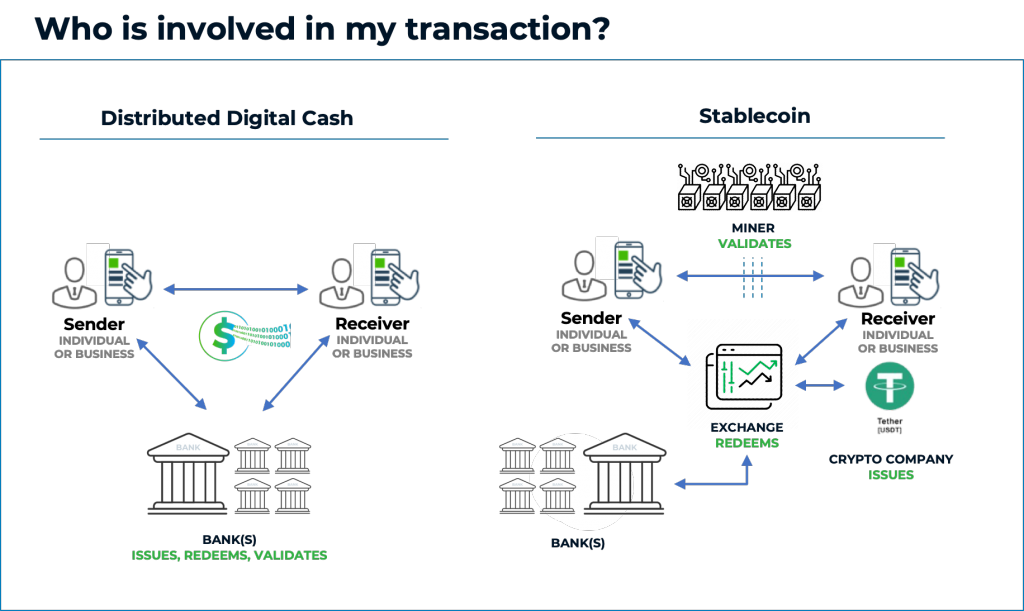

To understand the challenges of stablecoins, it helps to understand how a cryptocurrency transaction typically works. First, a sender buys the cryptocurrency or stablecoins; next, they transfer them; and finally, the receiver sells the stablecoins they received. In principle, if the stablecoin is pegged to a dollar, then a stablecoin dollar is more technologically secure than unencrypted dollars, yes?

However, converting funds into and out of stablecoins requires its own additional liquidity. The price of a coin is pegged to a fixed price by varying underlying liquidity levels to adjust to changing underlying demand. In addition, stablecoins incur third party costs for the entity managing the coins related to operations, technology and compliance.

A better approach is to match the solution to the problem from the outset. If the problem being solved is to provide certainty to immutable transactions of regulated currency, it is more elegant – and practical – to design DLT solutions to fully comply with existing regulations. Digitised cash is such an approach.

Stablecoin vs. digitised cash – what’s the difference?

A new category of solutions is now emerging around digitised cash, sometimes called distributed digital cash or cash-on-chain. Perhaps less known or understood, its key distinction is that it is issued and controlled by banks or regulated institutions, who can seamlessly back an encrypted digitised dollar with any government issued currency. The bank still needs DLT technology to support such digital cash but it does not require a separate, third party exchange.

Let’s take a deeper look at the differences between stablecoin and digitised cash. Despite claims that a stablecoin dollar is no different than a normal dollar, stablecoins are classified as a traded security with a bid-ask spread. They are issued by a private company, and as such, they require liquidity to maintain a one-to-one pairing to a national currency. As well, someone must bear the cost of the exchange(s) in addition to a private party holding reserves to maintain price stability.

Further, the assets backing the stablecoin should ideally be ring-fenced and stable. However, incidents such as the use of the funds behind Tether stablecoins to buy volatile Bitcoin in 2017, followed by its price crash in 2018, highlight the risks of a stablecoin.

By contrast, digitised cash requires no additional liquidity. An encrypted dollar is issued within a permissioned network (public or private) by a commercial bank. The bank ring-fences the corresponding unencrypted funds in an undesignated client monies account. At the conclusion of any transaction with digitised cash, the one-to-one value of the cash remains. There is no fluctuation (and the cost to the bank to ring-fence one account in a bank managing millions of accounts is negligible).

| Distributed digital cash | Stablecoin (cryptocurrency scheme) |

| Issued by bank or regulated institution. | Tradeable asset, which can be purchased by bank or other institutions. |

| Users of cash must follow existing regulations, e.g., anti-money laundering. | Users of stablecoin use as they see fit. |

| Permissioned, licenced issuers. | Third party issuers and liquidity providers. |

| Relies on segregated funds (no additional liquidity needed). | Relies on exchanges and additional liquidity reserves. |

| Value of currency managed by national central bank. | Asset of fluctuating value, programmed to automatically follow a defined price. |

Which solution will prevail? Three factors may shape the future:

- Ability to manage personal information.

Transaction details can be classified as personal data in some jurisdictions, and subject to data protection laws. This becomes a challenge for DLT / blockchain, as the very nature of a distributed architecture is that data is distributed and nodes are processors of data. This could create obstacles for regulated institutions who cannot let unauthorised processors handle personal data, especially for networks where transactions are publicly broadcast.

Digitised cash, with its ability to be issued and governed by regulated banks and other institutions, makes it both architecturally and legally feasible to address critical data protection issues. For example, rules can authorise only certain nodes to participate in transactions – while limiting access of non-relevant parties – and such specification would be part of the legal relationship between a client and the bank issuer.

- Interoperability with existing infrastructure.

At the most basic level, any solution for payments must be able to readily move in and out of currency formats – either physical cash or electronic card or other payment.

The advantage of a digital cash solution is that banks are already interconnected to both physical-to-digital (e.g., deposit at an ATM) and digital-to-physical cash networks. As such, no additional connectivity is required and furthermore, the DLT can be used to streamline clearing in the back office between a bank and a provider of physical cash.

With regard to foreign currency (FX), digitised cash levers the bank’s full balance sheet and the bid/ask spread is minimal. The obstacles for stablecoin multiply with the addition of each additional currency due to the need to add liquidity to avoid fluctuation of stablecoin values.

- Regulatory challenges.

In addition to regulations regarding personal data, payment and banking regulations also govern who can hold accounts and how they use them. Digitised cash solutions allow nodes and cryptographic key management to be tailored to existing payment and data regulations. And while no one wants to limit the power of an ecosystem, digitised cash architecture allows unwanted or malicious actors to be blocked or to facilitate the collection of additional information when necessary.

For stablecoins, there are multiple projects working to create schemes that regulators could accept. Stablecoin issuers will likely make the necessary adjustments to comply, but it is not clear if the resulting stablecoin solutions will be cheaper than traditional technology.

Future work in digital identity may lead to additional features and functionality that could be more effectively provided using DLT technology for either the stablecoin or digitised cash approach.

Keeping the DLT conversation – and innovation – going.

Both blockchain (the breakthrough technology underpinning Bitcoin) and DLT (levering blockchain technologies) continue to evolve. Stablecoin cryptocurrency is the subject of ongoing discussion as regulators, policymakers, governments and financial institutions around the world debate implementation. For less popular national currencies, this may be the innovation necessary to shift from physical to digital cash, and as such, stablecoin offers a viable solution. Fnality, the newly created consortium of banks using UBS’s stablecoin, is focused on such solutions and is making progress.

It is still early days on both approaches, though most experts seem to believe that both stablecoins and digitised cash are here to stay.

Terms to Know

- Altcoin is a non-frequently traded cryptocurrency. They are extremely volatile, like penny stocks.

- Bitcoin is the first broadly adopted form of cryptocurrency. It is based on the concepts of blockchain and distributed ledger technology published in an academic paper in 2008 by an entity calling itself Satoshi Nakamoto. It operates as a security, a commodity or a foreign currency in market transactions and is not legal tender.

- Blockchain is a growing list of records, called blocks, which are linked using cryptography. A blockchain is an immutable time-stamped series of records of data that is distributed and managed by a cluster of computers. Most, but not all DLTs, use blockchain.

- Cash-on-Coin is a synonym for digitised cash. (See below.)

- Cryptocurrency refers to the entire class of digital assets secured by cryptography and operating in a DLT architecture. It is a general term used to describe either a stablecoin or an altcoin.

- Digitised Cash is a digital asset tied on a one-to-one basis to legal tender and operating within a DLT system.

- Distributed Ledger Technology (DLT) is a distributed database that is consensually shared and synchronised by all participants (called nodes). It is the underlying technology used for all cryptocurrency as well as for a growing number of business and document management applications.

- Stablecoin is a digital asset that operates as a security in market transactions and is not legal tender. Examples include Tether and Libra.

- Virtual Coin is a term most often associated with gaming tokens. It is distinct from cryptocurrency and does not require blockchain or DLT.

By David Putts, chief growth officer, Billon Group

Nice Article to read

Nice Article