The allure of omnichannel: New functionality, seamless SMB journeys

SPONSORED INSIGHTS

Banking journeys and the touchpoints within financial institutions (FIs) are becoming more complex, starting and stopping across multiple channels that include a mix of physical and digital.

Even though digital engagement is growing, physical interactions and the mix between teller and self-service play important roles in many consumer journeys, especially in the small and medium-sized business (SMB) segment, where SMB owners often have physical storefronts and use financial services constantly.

Our research has found that 55% of SMBs use the branch teller twice a week and 59% use the ATM twice weekly. Although SMBs are using financial services frequently, 93% of FIs confirm that merchant customers can’t always fulfill all of their cash and coin needs. More than half of SMBs feel they spend too much time waiting in line and more than 75% of merchants say they would use automated or self-service technology for cash deposits and withdrawals, if the right technology was available.

As is usually the case with technology, interest and usage varies from one individual to another. SMBs, like every consumer, want to have the choice. In a survey Diebold Nixdorf conducted last year, SMBs expressed a desire to use more tailored self-service technology but would also consider switching banks if they were forced to use self-service instead of going to a counter.

That paradox underscores the importance of delivering an omnichannel experience, rather than focusing on one area, be it physical or digital. Self-service operates in the sweet spot between physical and digital channels, enabling fast and secure cash transactions 24/7 and helping banks drive visibility across their entire network. Regardless of whether FIs view their ATMs as a utility for cash management, or as a strategic touchpoint in their overall digital strategy, how to make the most of ATM interactions should be top of mind.

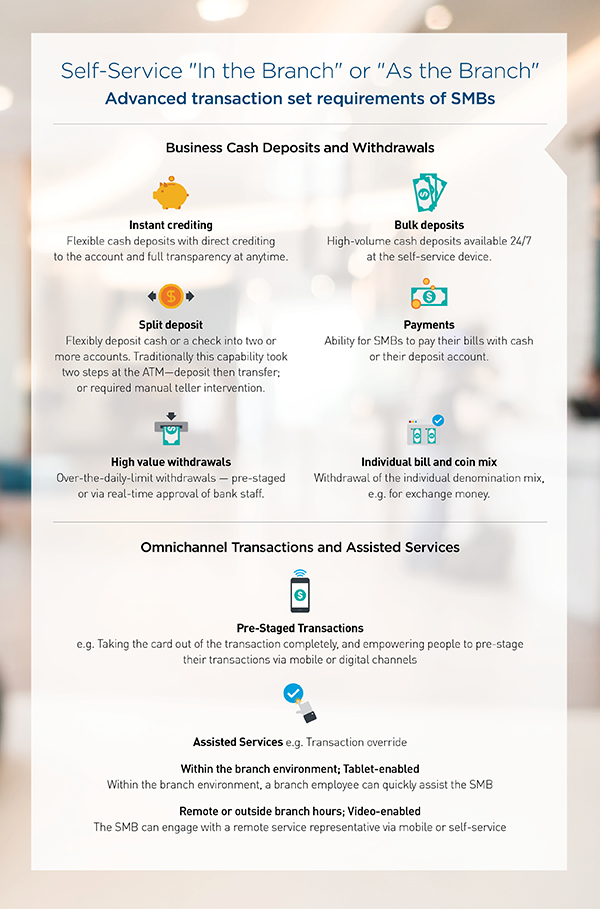

With the right software in place, the ATM can play a new role, not just “in” the branch but “as” the branch, fulfilling the advanced transaction set required by SMBs, like bulk deposit, split deposit, instant crediting etc.

Advanced transaction set requirements of SMBs

With the right self-service solution in place to automate additional transactions, employees are free to help develop SMB relationships; it’s a win-win situation for FIs and SMBs:

- FIs benefit significantly from cash automation due to reduced workload and costs of manual cash handling tasks.

- SMBs reduce their waiting time in the branch—which is one of their biggest concerns—and receive enhanced capabilities with 24/7 cash services, especially if they are able to pre-stage a transaction via mobile or any other digital channel wherever and whenever they want and complete the transaction in the branch or at the self-service device at a later stage.

Customers have the freedom of choice they demand, and FIs have enabled an ideal omnichannel experience.

Learn more about the benefits of modern self-service technology at DieboldNixdorf.com/SMB.

By Thomas Schulze, Vice President of Systems for the Americas, Diebold Nixdorf