Owning customer relationships is a key priority for banks in the era of open banking

Open banking has been at the top of the industry agenda for the last few years and continues to drive the innovation and technology conversation for retail banks worldwide. Given the potential for third-party access to data and services to completely transform the relationship customers will have with banks, this is entirely unsurprising.

The initial driver has been the regulations-driven requirement for open banking, with deposit-taking financial institutions in many markets (particularly Europe with the Second Payment Services Directive (PSD2)) required to open up customer data to third-party providers. Subject to customer consent, banks have been required to provide APIs that allows data to be accessed. Aside from Europe, there has also been regulatory drive in Hong Kong and Australia with other countries such as the US seeing open banking as a market-driven opportunity.

The number one concern, unsurprisingly, is ensuring online security.

Initial fears about non-financial institutions competing directly with banks to offer financial services as a result of open banking regulation have yet to materialise but to mitigate the risk, banks could stake a claim to become an aggregator of financial needs. By utilising third parties, banks can introduce digital services which are value-adding to consumers and sought after without having to build it from scratch. Singapore-based DBS has been an early adopter of this trend since launching a marketplace for cars, property and electricity in 2018, allowing customers to easily compare products and prices.

The bank has since launched its first integrated travel marketplace in 2019, in partnership with Singapore Airlines, Expedia and Chubb Insurance, which allows DBS customers to directly book and pay for trips whilst being provided complimentary travel insurance. Mox, a digital Hong Kong bank launching in 2020, has taken a slightly different approach since it is backed by Standard Chartered but in partnership with PCCW, HKT and Trip.com which will offer a comprehensive suite of retail financial services, as well as telecom, entertainment and travel products, all in one place.

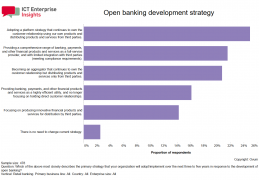

Owning customer relationship priority for open banking development strategy

Source: Omdia ICT Enterprise Insights 2019/20

Omdia (formerly Ovum), conducts an annual ICT Enterprise Survey – a study comprised of more than 6,600 interviews of CIOs and other senior IT decision-makers – which was conducted between July and September 2019. When asked about the technology strategy behind their open banking development, respondents specified that owning the customer relationship was critical with more than 66% of retail banks indicating this.

Open banking offers the opportunity to adopt a marketplace strategy whereby retail banks can offer new products and services beyond their core portfolio through third parties utilising APIs. There are many examples of how this is being currently utilised, the Commonwealth Bank of Australia has released a tool called ‘benefits finder’ which using open banking API technology that can identify unclaimed benefits or rebates for its customers. Similarly, Danish bank Nordea has launched a subscription management service which allows consumers to get an overview of all their subscriptions and unsubscribe straight from the bank’s interface. 2020 will follow in the same vein as retail banks look to expand their digital engagement product initiatives utilising open banking technology as a source of both maintaining existing relationships and acquiring new customers.

Although open banking does provide numerous opportunities going forward, the immediate focus for many retail banks is the challenges they face consequently. The number one concern, unsurprisingly, is ensuring online security and protecting against fraud with 28% of respondents in Omdia’s ICT Enterprise Insights Survey stating it was their top priority. Fraud checks will become more difficult when payment is initiated through third parties as information on device or customer information may be limited compared to the bank’s own channels. Retail banks must also ensure third party services are legitimate in order to protect customers and comply with open banking data and privacy regulation.

The banking marketplace model holds a lot of promise but neobanks will continue to lead innovation for now as they are more effective and nimbler at customer data collection compared to incumbents. Nordic challenger bank Lunar have announced they plan on generating 65% of their revenue through marketplace partnerships and it has long been Monzo’s ambition to be the marketplace for all customer financial needs. Established retail banks will continue to prioritise modernising legacy technology infrastructure before fully embracing the marketplace model, but it is clear that the customer will demand a shift in mindset and dictate the pace to which they expect it to happen.