A2A payments set to threaten dominance of online card transactions

Account-to-account (A2A) payments is nothing new; bank transfer services have existed for many years and traditionally been used by consumers to schedule regular bill payments, but through open banking and real-time payments, A2A has a genuine opportunity to become a credible rival to the card payment rail for everyday transactions too.

Financial services have undergone a digital transformation which has seen banks move from legacy infrastructure to modern cloud-based technology but payment rails, although evolving, largely rely on traditional card networks. The introduction of open banking allows third parties to initiate payments on behalf of consumers as a registered PISP (payment initiation service provider) and making payments directly from a bank account and potentially reducing fees for merchants, banks and the consumer.

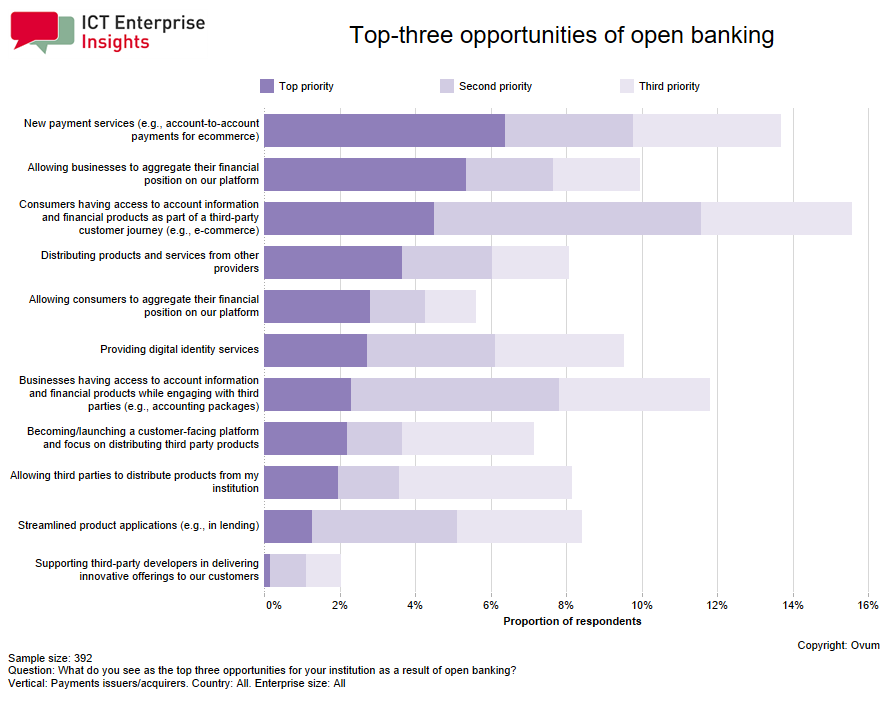

Despite it being early days for A2A payments it has already been identified by payment issuers/acquirers as the number one opportunity of open banking according to Omdia’s ICT Enterprise Survey (ICTEI) 2019/20—a study comprising more than 6,600 interviews of chief information officers (CIOs) and other senior IT decision-makers conducted between July and September 2019.

Bank transfers or Automated Clearing House (ACH) payments are already a popular payment method for online payments and estimated to account for 9% of global ecommerce payments in 2019 according to Worldpay’s 2020 Global Payments Report.

Source: Omdia ICT Enterprise Insights 2019/20

A2A payments could be an unintended beneficiary of SCA

The exponential growth of ecommerce transactions has also caused a surge in payment fraud which remains a critical challenge for banks with the card payment fraud the most common. In the UK alone card fraud totaled £671 million in 2018 representing 56% of total fraud losses according to UK Finance.

In Europe, fraud has been recognised as a huge problem across ecommerce transactions which is why they are implementing strong customer authentication (SCA) as a requirement for all online transactions above €50 from 2021.

SCA requires the consumer to have two forms of authentication in order to process the transaction which could cause friction for consumers. Utilising A2A payment will naturally meet the multi-factor authentication requirements as it requires the consumer to authenticate each individual payment through their banking app. Issuer banks may see a fall in card revenues but a reduction in fraud losses will have a transformative impact on the business model of a retail bank.

Payments industry is planning for a “cardless” world

Card issuers and networks are understandably reluctant to encourage consumers to adopt alternative payment methods because of the commercial interest in maintaining card revenue. However, it is clear that the legacy technology is not going to meet the needs and demands of the consumer in the future. Change is inevitable, predicated by open banking, which banks, merchants and ultimately consumers will adopt.

Legacy card networks are taking the threat of A2A payments to their existing payment rail business seriously by diversifying their product portfolio with a series of strategic acquisitions and product launches which should indicate to the rest of the industry the direction this is heading.

Mastercard has been quick to recognise the threat to their card payment business with the 2017 acquisition of Vocalink, the UK-based payments system company, and the 2019 purchase of Nets’ A2A payment business – although the acquisition of the Nordic platform is still subject to regulatory approval. American Express launched “Pay by Bank Transfer” in 2019 that enables UK consumers to make real-time payments for goods and services online direct from their bank account utilising open banking technology even if they are not American Express card holders.

A2A payments set to threaten dominance of online card transactions.

The future of banking services will occur at the checkout phase; for example, rather than taking out a personal loan or credit card to afford a holiday before purchasing, consumers will be offered finance options, insurance etc. at the point-of-sale during the checkout process. We have already seen with the explosion of the “buy now, pay later” trend, fronted by the likes of Klarna and Afterpay, that consumer demand is high thus there is no reason why banks can’t pivot their business model to cater for this type of overlay service.

There are already signs that banks are planning for a world that no longer relies on the card network duopoly of Visa/Mastercard, with the Eurozone’s major banks starting an initiative known as PEPSI (Pan-European Payment System Initiative) which looks to implement a standalone digital payments scheme. Account-to-account payments is one of many alternative payment methods that will rise in popularity as the shift away from card payment dominance gathers pace.

Find Philip’s views on payments and more via the links below:

LinkedIn: https://www.linkedin.com/in/philip-benton/

Twitter: https://twitter.com/bentonfintech