Embedded finance: a game-changing opportunity for incumbents

Summary

- Embedded finance offers a new, very large addressable market opportunity worth over $7 trillion in ten years’ time, twice the combined value of the world’s top 30 banks today.

- By abstracting banking and insurance functionality into technology embedded finance enables any brand or merchant to rapidly and at low cost integrate innovative financial services into new propositions and customer experiences.

- Fintechs, supported by VCs, are currently taking the lead in creating sophisticated embedded finance offerings via Banking-as-a-Service platforms.

- Incumbent banks and insurance companies now need to make bolder and more strategic moves to stake their claim.

- There are three key issues incumbents will need to address to grasp this new market opportunity effectively and use it as a catalyst for wider business model transformation.

What fundamental problem are we addressing?

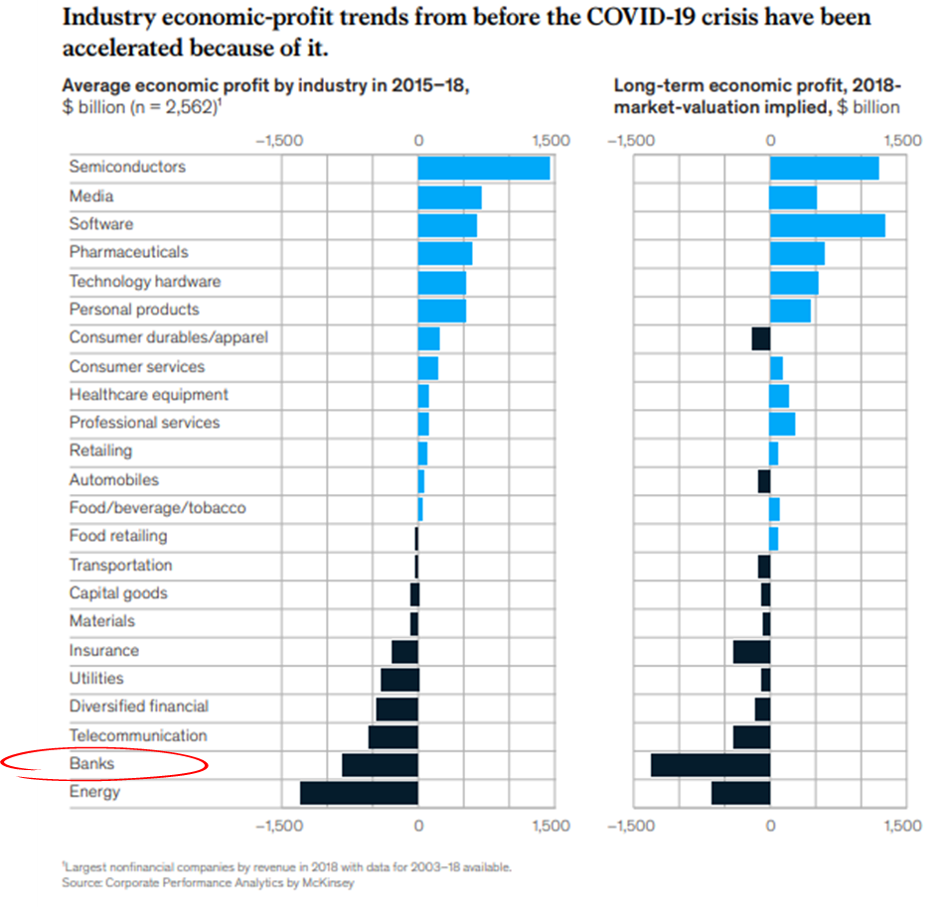

Even before the COVID crisis banking and insurance were two of the worst performing sectors worldwide. According to a recent report from McKinsey, the economic profit of the world’s top banks and insurance companies declined by $800 billion and $300 billion respectively between 2015 and 2018.

The COVID crisis is making these trends even worse.

“Economic profit” is profit after cost of capital. It is a measure of an organisation’s efficiency at resource allocation. In other words, it demonstrates the returns an organisation gets from the solutions it offers customers (and society more broadly) after paying back the costs of funding them.

It’s also a good measure of innovation effectiveness, and by this measure the industry is not delivering for its stakeholders.

The hard truth is that the financial services industry has not updated its core business model in centuries, and the urgency to do so now is even stronger than it was before COVID.

Banks and insurance companies have spent billions of dollars digitising their existing operations. But the time has now come to invest fully in creating digital business models, to help the wider economy recover from the COVID crisis too.

Embedded finance offers one of the most exciting new digital growth opportunities to incumbent financial institutions: an addressable market worth over $7 trillion, or roughly double the market value of the world’s top thirty banks today.

VCs, big tech and fintech entrepreneurs are excited about this market and are pouring more money and effort into it, following successes like Plaid, a seven year old start-up which was sold to Visa for over $5 billion recently, and the enormous growth of Square and Stripe.

It’s time for incumbents to play in this space too, wholeheartedly and at scale. But it requires a deeper understanding of the types of digital business models available and how to build a portfolio out of them.

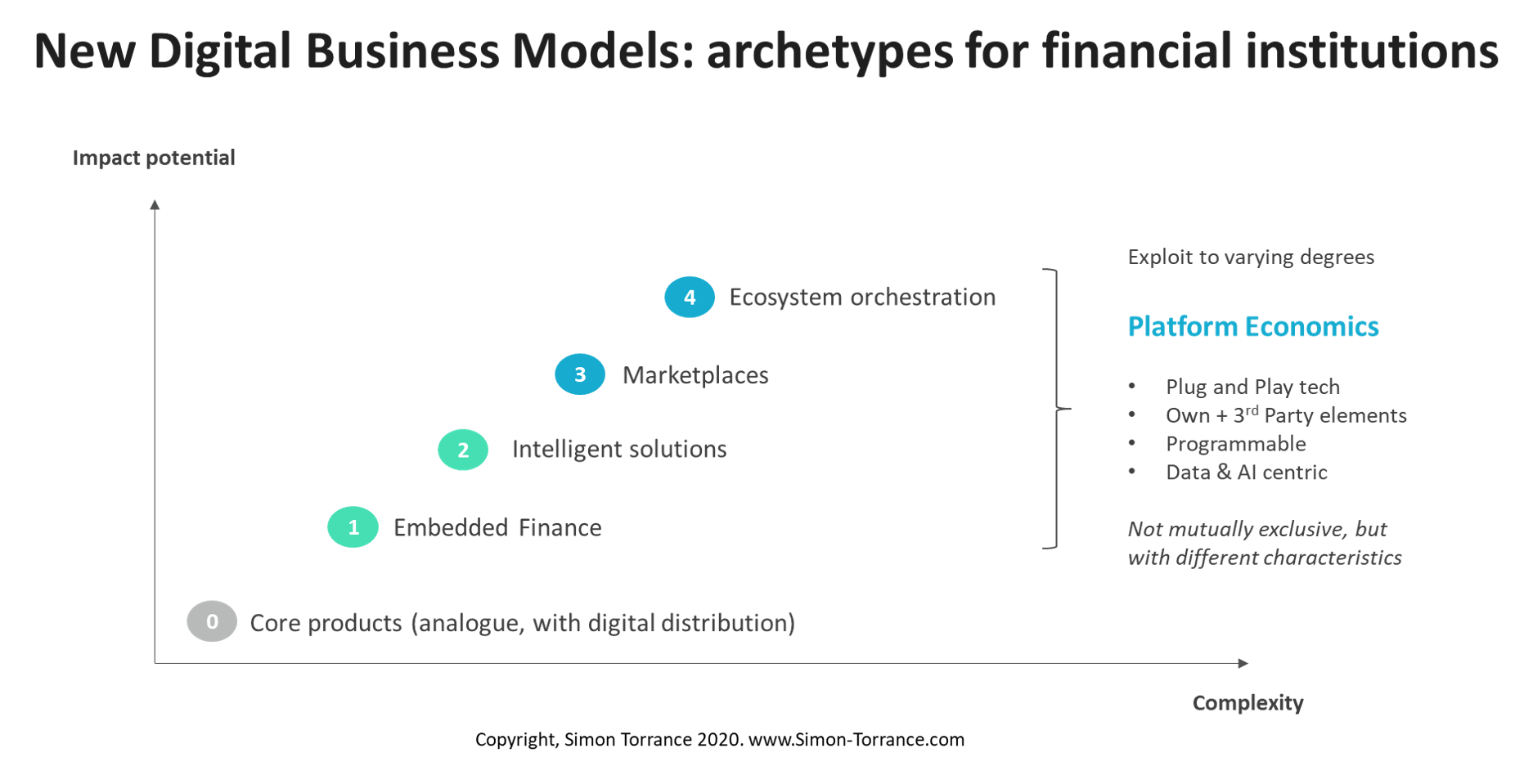

New digital business model archetypes

Embedded finance is about abstracting banking and insurance functionality into technology and enabling any brand or merchant to integrate innovative financial services into their offerings and customer experiences, rapidly and at low cost.

It is one of four new digital business model archetypes that are particularly relevant to financial institutions.

The four new business model archetypes in the diagram all exploit platform thinking and platform economics, and are highly suited to an increasingly platform mediated digital economy.

Platform thinking means leveraging the creativity and resources of third parties to create greater value for your customers and markets, rather than trying to serve customers only with your own products.

In practice, this means exploiting advanced digital technologies and different ways of capturing value.

Platform-based business models dominate in an increasingly hyperconnected digital world, due to their powerful underlying economics. Seven of the ten most valuable companies in the world, five of the top eight financial institutions and seventy percent of unicorn startups are driven by platform economics.

They focus on exploiting and monetising “intellectual capital” (encapsulated in software) and “relational capital” (connections between multiple parties), which have near zero marginal costs, rather than asset-heavy “human capital” (people) or “financial capital” (money).

While these concepts and principles are second nature to VCs, big tech and tech entrepreneurs, they are new and somewhat alien to most leaders at banks and insurance companies (and most traditional sectors) today.

As a result they have not incorporated – wholeheartedly, effectively and at scale – by the industry so far. Hence the economic profit figures.

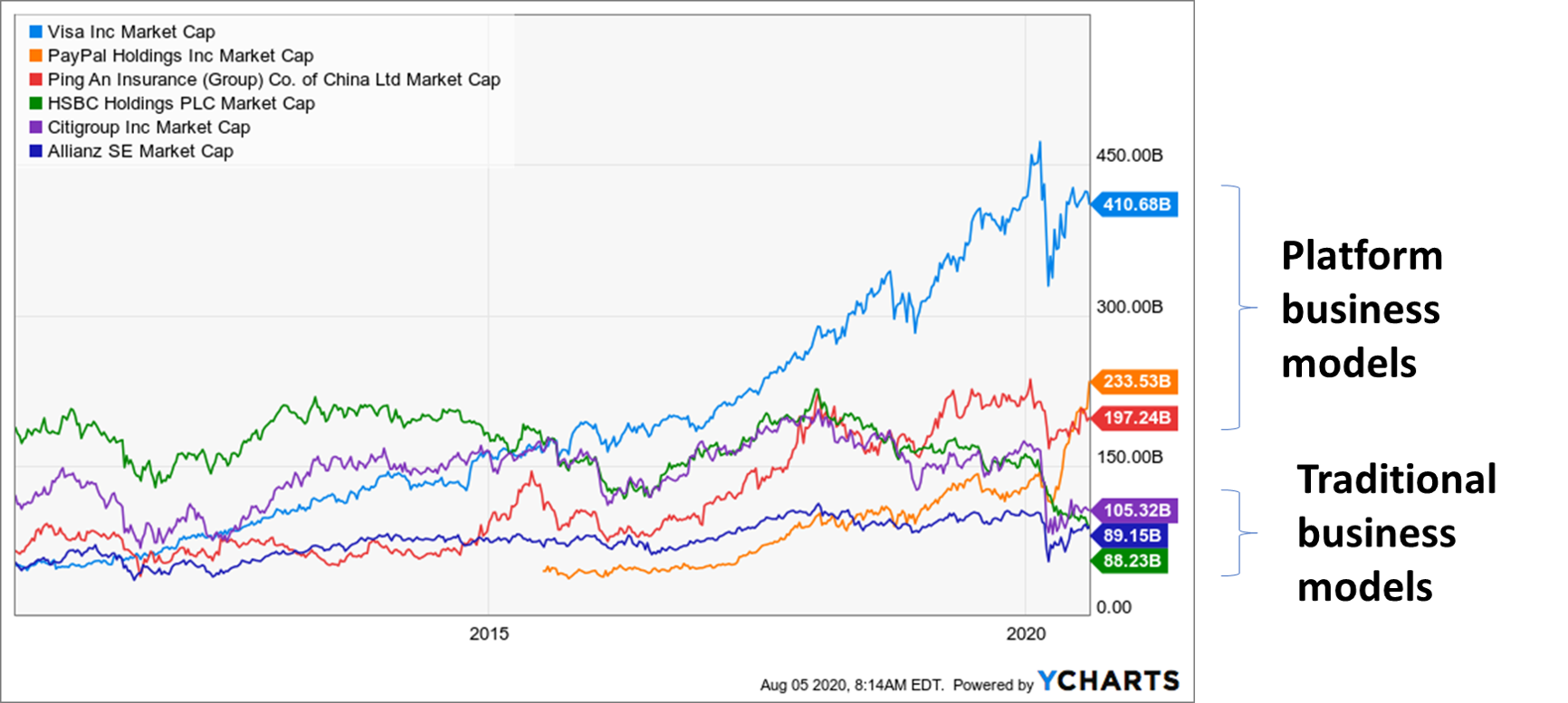

There are some notable exceptions, like PingAn, which fully embraced platform thinking some years ago. As a result it has grown rapidly and is now worth more than Citi, HSBC and has overtaken all local competition.

Platform business models (PingAn, PayPal, Visa) vs HSBC, Citigroup, Allianz

I’ll discuss in more detail the other business model archetypes and how to design synergistic portfolios in future articles. Let’s now look at embedded finance and why it could be a powerful catalyst for business model transformation for incumbent banks and insurers.

Embedded finance – how it works

Put simply, embedded finance is about enabling any business to manage and sell innovative financial services; seamlessly integrating creative forms of payment, debit, credit, insurance or even investment into their end user experiences.

The simplest example of this in action is paying for an Uber ride. You don’t get out your credit card at the end of the journey. Uber product designers have enabled payments to be embedded into your experience of getting a lift and, for the driver, into their experience of getting paid the right amount at the right time.

Payment facilitation companies like Stripe and Square have grown rapidly over the last ten years by enabling this sort of capability for digital companies. They are now worth $36 billion and $57 billion respectively and are expanding their capabilities into other areas.

Complexity increases as you move from payments to debit, credit, insurance and investments. But if you are a merchant or brand in any sector you want to make your propositions to customers as attractive as possible.

Today customers have to interact with their banks to get debit and credit cards, loans for a sofa, car or house, and there’s a lot of back and forth between the customer, the bank, and the merchant, with few options personalised to the needs of individual customers.

Klarna has grown into a $5.5 billion company by enabling brands to offer innovative credit solutions at the point of purchase, for example, by paying in instalments.

Lambda School provides online training for would-be coders. It offers various payment options, including an income sharing agreement, whereby the student is charged a cut of his/her future income rather than an upfront tuition fee. The student deals directly with the school for this and the other payment options offered, rather than seeking a loan from a bank. This may or may not be attractive to everyone, but it demonstrates the opportunities for creativity that embedded finance enables.

Embedded insurance is now fast emerging too, enabling your car share service, for example, to come automatically with mobility insurance, or your new camera to come with theft and damage protection right out of the box as part of the overall price.

Some of this happens already today, but it’s clunky. British Airways offers travel insurance on its website when buying a flight. But it’s not quick and cost effective for brands and merchants to integrate these offers and they tend to be generic and managed by the insurer rather than configured in real time by the brand. For banks and insurers who today “white label” their products and capabilities to third parties, the timeframes are months or years to conclude deals, and years to implement at scale and see a return.

Today white-labeling financial products for merchants is far from a digital business model for banks/insurers: it has high costs to serve, long RFP-based sales cycles and lumpy revenue.

Ultimately, financial services will disappear into the background of the solution being offered to a customer. British Gas has already stopped selling me “boiler insurance” – a dull product. It now offers “remote boiler maintenance” (enabled by IoT-optimised underwriting) – a much more attractive proposition.

Embedded finance – as opposed to reselling financial services – is attractive to digital brands and merchants because it creates new revenue opportunities at very low marginal cost (the brand already has a customer base). It enables new customer experiences that drive loyalty and repeat purchase and allows merchants to capture more of the economics of the relationship.

For pure software companies, it could potentially enable them to increase revenue per customer by two to five times, according to VC a16z.

For example, Shopify, a B2B e-commerce platform, now makes over $500 million per annum from financial services to its merchants (growing at over 50% per annum). The underwriting costs are much lower, as Shopify already has a huge volume of data about its users.

For many software and platform businesses, financial services are, and will increasingly be, a very lucrative addition to their core business.

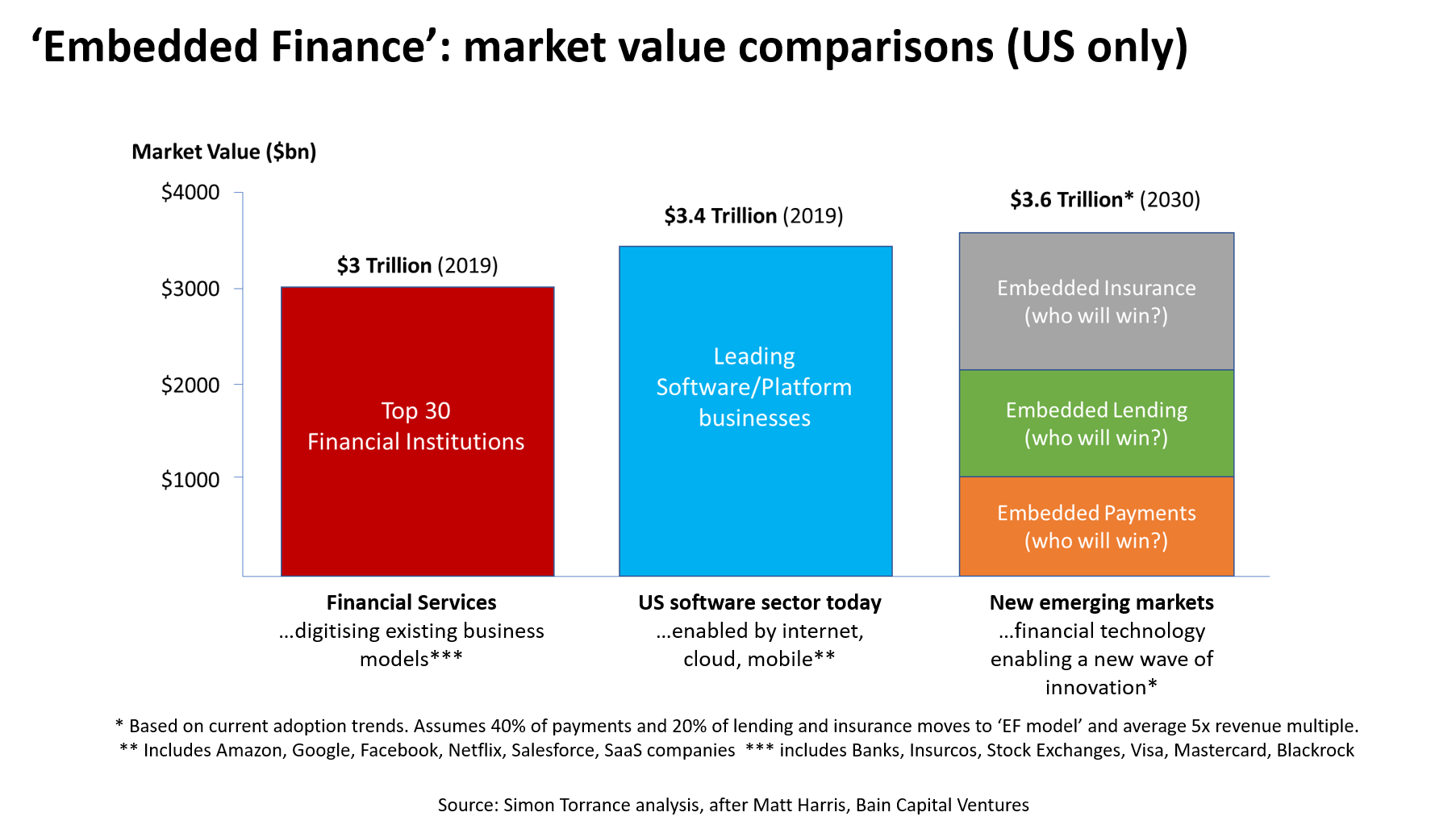

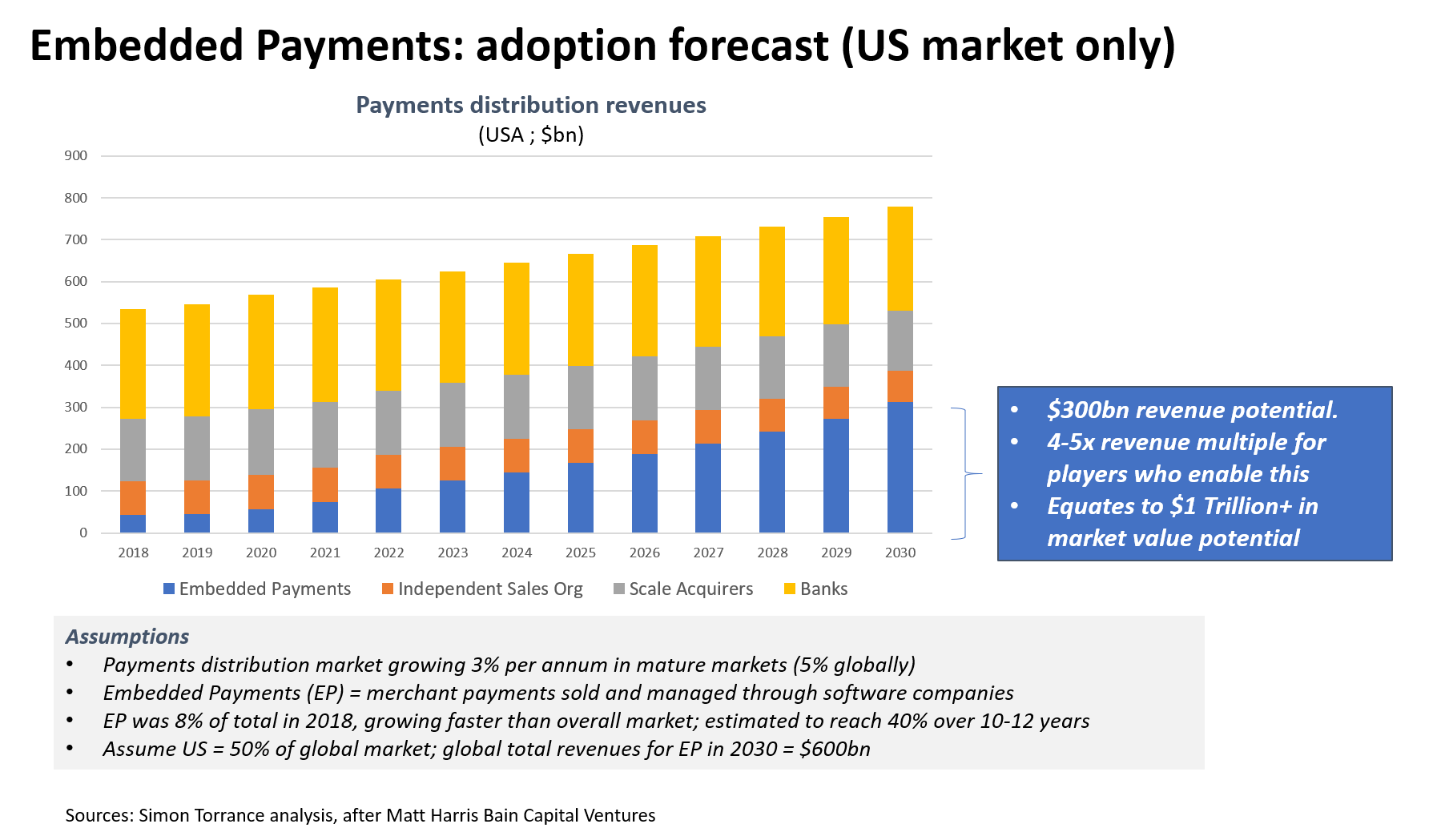

Addressable market sizing

According to analysis by Matt Harris from Bain Capital Ventures, if you extrapolate forward the current rates of growth in embedded payments, and make some assumptions about slower adoption rates but the larger market sizes of lending and insurance (lending is roughly double and insurance triple the size of the payments market, by revenue and profits), then assume that companies enabling embedded finance deploy SaaS based commercial models with valuation multiples of 5x revenues, you quickly get to a new market potential for entrepreneurs, investors, fintechs and incumbents of $3.6 trillion in ten years time… in the US alone.

To put this in perspective, embedded finance could potentially create businesses worth more than the total pre-COVID value of America’s top 30 financial institutions.

The diagram below demonstrates the assumptions behind payments.

Again, this is just the US. If we double these figures and those for lending and insurance to create a global addressable market (given lower market maturities and adoption rates outside the US), then we get to $7.2 trillion in ten years, about double the market value of the world’s top 30 banks today.

Or, put another way, embedded finance opens up the opportunity – for investors willing to grasp it – to create businesses worth more than today’s software and platform firms in half the time it took them… or ten times as quickly as it took the US financial industry to get to where it is today.

What underpins these assumptions, according to Matt Harris and other visionary analysts, is the emergence of financial technology as the next (fourth) development platform for the digital world.

The internet itself was the first platform. It bought “connectivity”. The cloud followed, and bought on tap computing power and “intelligence”. Mobile was the third development platform, which bought “ubiquity”. The fourth platform is financial technology (fintech), which enables entrepreneurs to create new businesses related to “value exchange”.

Many powerful new businesses took advantage of these phases in the evolution of the digital economy. Ebay, Amazon and Facebook leveraged the internet; Salesforce and AWS exploited the cloud; the Apple’s AppStore, Tencent and Uber required mobile; Lending Club, Stripe and Ant Financial have been born on top of fintech.

Ant Financial, as spin off from Alibaba, is planning to IPO this year at a valuation of circa $200 billion. Who will create the next Ant Financial? Could it be a spin-off from an incumbent bank?

Banking-as-a-Service platforms enable embedded finance

Banking-as-a-Service (BaaS) platforms are enabling sophisticated forms of embedded finance. They connect into core financial systems via APIs and give digital brands and merchants tools to rapidly configure financial service elements into their user experiences.

BaaS has been in development for about five years, has now become mature and is being deployed at scale. VCs are excited about this emerging market, and are funding more start-ups.

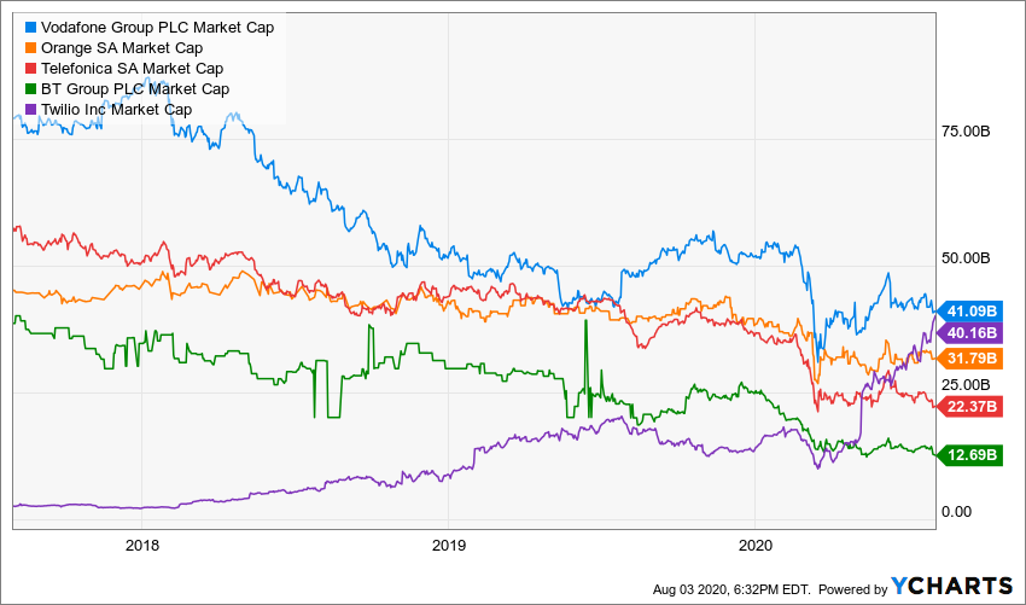

Notable examples of BaaS players include Galilleo (recently acquired by SoFi), Synapse, Marqeta, Bankable, Railsbank and Bond (a well-funded newcomer led by senior talent from Blackrock, Goldman, SoFi and… Twilio). The Twilio heritage is particularly relevant. Born out of the telecoms sector, Twilio pioneered Communications-as-a-Service, a precursor to BaaS, over ten years ago. It enables product developers within enterprises to embed communications (text, voice, chat) into their customer experiences. It enables rider-driver interactions on Uber, for example.

Twilio is worth $40 billion today, nearly as much as Vodafone Group, with a 30x valuation multiple compared to Vodafone’s 0.9x. You can see which type of business model investors prefer. Not bad for an “enabler”.

Railsbank, a four year old start-up led by successful serial tech entrepreneurs, originally nurtured by my friends at Startup Bootcamp and invested in by Visa, offers fintechs, financial institutions, digital banks, as well as non-financial brands and merchants a “single API into the global financial system”.

It enables them to create and prototype any financial use case in days and launch it within weeks. The potential to commoditise incumbent financial institutions, in the way Twilio did in telecoms, is significant.

Today, only a few major regulated banks are taking strong positions in this market at present: BBVA, an international Spanish bank, with its separate Open Platform business unit and Goldman Sachs, through its new digital consumer bank Marcus, which has sealed deals with Amazon to provide lines of credit to merchants and with Apple to provide credit cards. Standard Chartered has recently launched a dedicated BaaS offering, nexus.

Opportunities, threats and actions for incumbents

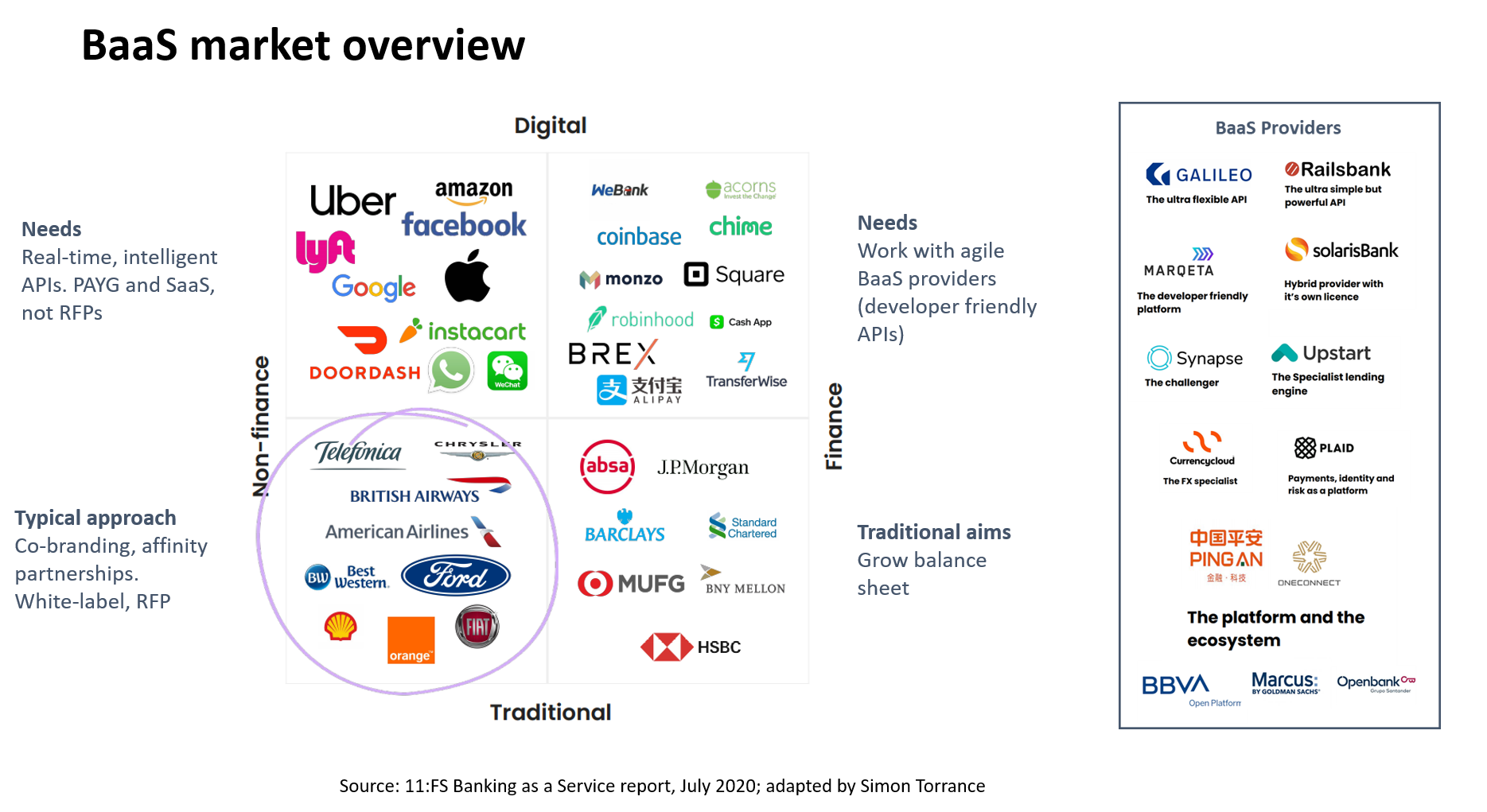

11:FS, in its recent report, “Banking as a Service – reimagining financial services with modular banking”, describes the emerging BaaS market, showing the different types of players, their needs and aims and lists some of the key providers.

Today, independent BaaS providers focus primarily on supporting digital companies, especially fintechs. But, we know that “traditional” and “non-financial” sectors will constitute the larger part of the future market as they digitise and they will also demand and expect developer-friendly solutions which are fast and easy to integrate.

This creates the perfect storm for those creating embedded finance solutions: the digitisation of every sector combined with mature financial technology and integration simplicity via Finance-as-a-Service platforms.

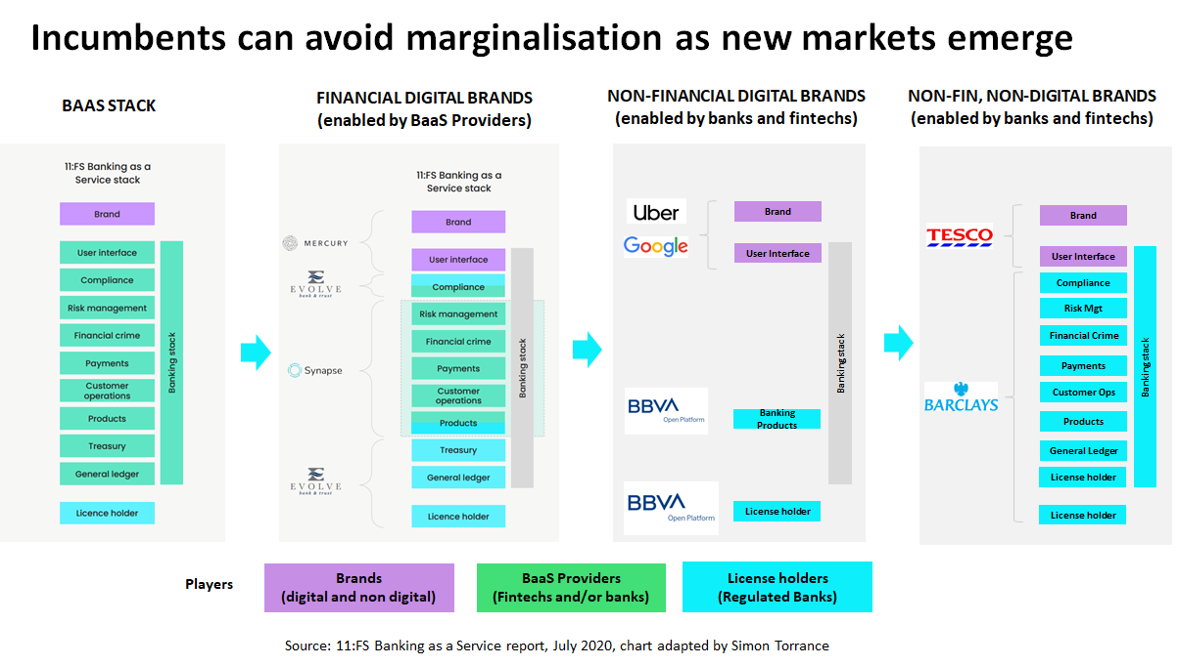

The danger for banks and primary insurance companies is that they could become marginalised and commoditised in this market. Due to open banking regulations and open APIs it’s now possible for more and more financial service capabilities to be delivered by non-regulated third parties. In its report, 11:FS presents the BaaS “stack”, and gives clear and useful examples of how the market is evolving.

You can see in the diagram below on the left that the only place where banks have a monopoly now is in their role as a regulated license holder. The green bars, which make up the “banking stack”, can now be offered by non-regulated BaaS providers.

The market to date has been focused on enabling new digital banks to emerge and to embed payments into digital services.

Mercury, for example, is a new digital bank for start-ups in the US. To deliver its services it accesses many of the capabilities it needs from Synapse, the aforementioned specialist BaaS provider. It also “rents” a licence and general ledger from Evolve, a small regulated “sponsor bank” based in Tennessee.

All parties win: Mercury gets to market fast with low cost and flexible infrastructure, Synapse grows its enabling business, and Evolve, a small local bank, has a new source of high margin revenues.

Sponsor banks who play in the US BaaS market are generating higher RoE/RoA multiples than those who don’t, according to a16z and 11:FS.

Since entering the market with its dedicated Open Platform business unit, BBVA has started to win business from leading digital companies like Uber and Google. In Mexico, Uber can now offer the 35% of its new drivers who have never accessed banking services before debit cards linked to their Uber accounts.

This type of innovation creates financial inclusion for the unbanked as well as enables the gig economy to operate more effectively.

Google Pay announced recently that it will now offer bank accounts and other financial management services to it users in collaboration with several banks including BBVA.

So, if we take this a step further, could Barclays (per the hypothetical case in the diagram above), for example, create a compelling BaaS platform that enables, for example, Tesco’s marketing teams to test and launch – within weeks – highly personalised savings, loan and health insurance offers to niche customer segments related to their profiles from Tesco’s ClubCard loyalty programme and spend at stores?

What about testing financing offerings for its supplier base, and orchestrating a more connected ecosystem between customers and suppliers – becoming a platform business itself? At the moment, Tesco Bank, formed in 1997, is costly, under pressure and sub-scale (it sold off its mortgage business recently to Lloyds Bank).

Rather than trying to be a traditional bank, why couldn’t Tesco use a BaaS platform to create new solutions for real untapped stakeholder needs.

Time for action, at scale!

Bank/Insurance/Investment-as-a-Service platforms will enable embedded finance. The examples in this article are just the starting point.

For incumbent banks the imperative is clear:

It’s time to fight back against the commoditisation and marginalisation of the current business model and upgrade it for the digital economy.

Embedded finance is one of four new digital business archetypes that, if combined within synergistic business model portfolios, will be very powerful.

In my experience of working with incumbents on this topic there are three key issues to address for a successful transformation:

- Leadership understanding and commitment. API-based BaaS platforms are new and alien to leaders of incumbent financial institutions. Helping them understand how they work, and the options they have in terms of where to play, how to win is critical to getting commitment to re-allocating sufficient capital and resources from other initiatives to support this market opportunity in a meaningful way.

- Organisational structure, operating model and skills. BBVA and Goldman Sachs created separate legal entities to tackle this market. New digital business models require radically different skills, technologies and metrics. Attracting experienced tech entrepreneurs who know how to develop and sell digital platform based solutions will be key. Establishing joint ventures with proven entrepreneurs, as PingAn does to kick-start its ventures, is one of the most effective approaches to reducing risk and increasing chances of success. Typically these are best managed away from the core, within anew organisational structure.

- Technical capability. As part of the strategy of where to play and how to win there are opportunities to quickly test and learn in the market by collaborating with startups in this space. This can help fast track customer engagement and internal understanding, create opportunities for acquisitions, and in so doing build technical capability faster. Combined with the separate business unit approach this sort of collaboration is an effective complement to relying on internal technical resources or external consultants.

There’s no time to waste when $7 trillion of value is at stake. It’s time to engage your executive team and board and get moving!

As the Chinese proverb says: “The best time to plant a tree was twenty years ago. The second best time is now”.

About the author

Simon Torrance works with leaders, executive teams and boards to create and implement new growth strategies and ventures based around the new disciplines of platform strategy, digital ecosystem management and corporate venture building.

Simon Torrance works with leaders, executive teams and boards to create and implement new growth strategies and ventures based around the new disciplines of platform strategy, digital ecosystem management and corporate venture building.

This is still a very relevant article. It would be good to get a series going in this space. Embedded finance is just one evolving modern business model as the article highlights. The obvious next focus has to be Intelligent Solutions.