If consumers welcome new payment options, why are they slow to adopt them?

The world of payments continues to evolve as traditional and challenger banks both race to offer consumers the latest innovation.

Consumers largely welcome a more diverse range of payment choices, but do not always take advantage of them when managing their money. These are some of the latest findings of the 2020 ING International Survey on new technologies which provides insight into how 13,000 consumers across 13 European countries spend and use their money.

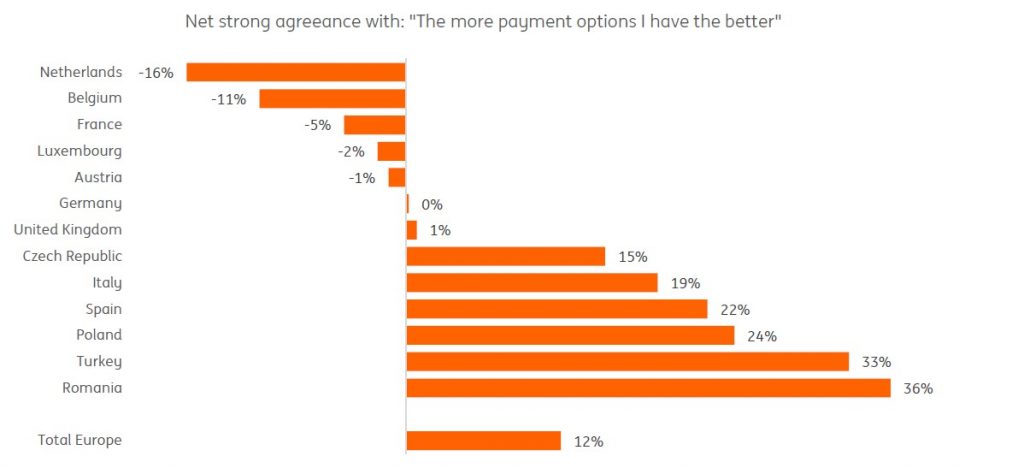

A quarter (25%) of Europeans completely agree that “the more payment options [they] have the better” which suggests many embrace innovations in this space. This is twice the proportion of those who consider the statement to be false (13%). Yet despite having a plethora of options available to them, in reality, on average, Europeans tend to use just a handful of ways to pay online and instore.

Attitudes do vary however across the continent, with Romanians valuing more choice most highly, and the Dutch most content having fewer options.

Use of different payment options is more likely to be driven by what’s on offer from the merchant rather than consumer demand, and unsurprisingly, tech-savvy consumers are the early adopters.

Those who own multiple devices use more options (owners of 8 devices use an average of 10.2 different forms of payment), whereas those who own just one piece of technology typically opt for three.

Socio-economic factors also play a part in determining how many methods people use, by impacting one’s ability to take advantage of digital options on offer. For example, those in full time employment use an average of 5.3 different payment methods, compared to 4 for those who are unemployed. Similarly, those earning more than €7k per month use an average of 6 different payment methods, twice that of those without an income.

Behaviour

Behavioural factors also play a role in payment use. For example, we tend to be overwhelmed by too many options, or stifled by ”choice overload”. As evidence of this, in the last six months, just three instore payment methods have dominated among respondents – cash (69%), chip and pin (65%) and contactless (57%).

For making online payments, the two favoured methods were entering card details (42%) or using PayPal (48%). It’s not necessarily irrational to want more options available, this is a risk-free arrangement for the consumer. However, juggling many different ways to pay, in reality, isn’t always efficient, and may be too much.

Secondly, shifting consumer behaviour takes time. People value convenience and security when managing their money, so the methods that prevail will be those offering both efficiency and trust. The trade-off between these factors when choosing how to pay relies a lot on the value of the purchase.

Small in-store payments are driven by convenience (40% choose their preferred payment method because it is quick, and 23% because it is easy). For higher ticket items, security is more influential. For medium and large expenses, 34% and 45% respectively say their payment preference was selected because it is secure. Online, security outweighs convenience across all payment amounts.

A challenge for new market entrants will be in overcoming consumers’ affinity for comfort and familiarity. This inertia can also be explained by notions such as sunk cost and loss aversion – we associate making a change with investment of time and risk the change doesn’t end up being any better than what we already have today.

People consistently say they anticipate using more payment options six months from now. But for a new payment option to truly take off, it must be adopted by networks. Positive social signalling can support acceptance in some people, and interest in others. Demand for having many payment options is there, but choice overload is real. Widespread adoption of new pays to pay will require, among other things, breaking habits and building trust.