A look inside MENA investor Global Ventures’ fintech portfolio

Between 2015 and 2019, fintechs in the Middle East and North Africa (MENA) landed $237 million-worth of investments, according to a Magnitt report with Abu Dhabi Global Market (ADGM).

This doesn’t seem like a lot compared to Checkout.com’s – close to double – $450 million mega-round last month.

But that doesn’t mean there isn’t money to be made from fintechs in this region. In fact, it means quite the opposite.

Global Ventures’ portfolio covers payment acceptance, digital wallets, credit and trading

Fintech investment landscape in MENA

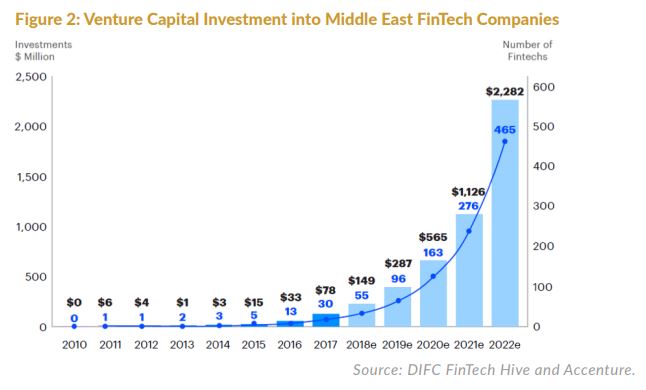

The Middle East’s fintech industry alone has a compound annual growth rate of 30%. Non-profit, Milken Institute, estimates that the region’s fintech scene will have raised $2.3 billion in venture capital (VC) funding by 2022.

That’s a jump of more than $1 billion between 2021 and 2022, meaning the Middle East is set for exponential fintech growth.

High-profile exits, such as Sukh.com to Amazon, and Kareem to Uber, compounded by governmental efforts to shift away from a heavy reliance on oil, points to brighter years ahead for fintechs in the region.

There’s little segmented data available for North Africa – a stretch which covers Algeria, Egypt, Libya, Morocco, Sudan, Tunisia, and Western Sahara.

Africa as a whole bagged $2.4 billion in deployed capital and acquisition value last year. Of that total, the largest individual slice – 31% – went to fintechs, according to Briter Bridges’ report.

That comes to around $744 million, ahead of the Middle East’s growth rate by a couple hundred million.

Early investors will certainly reap the rewards. One such backer is Global Ventures, co-founded by Basil Moftah and Noor Sweid. FinTech Futures sat down with Moftah to dig into its fintech portfolio.

Acceptance is “a huge opportunity”

Acceptance is “a huge opportunity,” says Moftah, using Egypt as an example, where less than 6% of the country’s 100 million population use digital wallets. This means a staggering 94 million don’t use digital payment methods.

“Egypt – until recently – has been the furthest behind globally in terms of digitalisation. This is perhaps best encapsulated in AAIB’s five-year go-live with Temenos.

Moftah adds: “It has the lowest credit card and debit card penetration rates. So, the first thing regulators are looking for is how to turn cash into digital. Cash in, and cash out.”

Paymob, one of Global Ventures’ portfolio companies, consolidates local payment methods through a single application programme interface (API) for businesses.

Back in September, PayMob’s co-founders, Alain El-Hajj and Islam Shawky, told FinTech Futures cash is their biggest rival.

“Day by day, there’s a consistency in new payment options getting added to the market – local card schemes, neobanks, digital wallets – and we onboard all these to our platform,” the co-founders said.

“[But] our major competitor is cash – that includes cash behaviour and the philosophy enshrining cash. When we build products, we try to attack what we call a cash pool.”

Moftah is confident that this groundwork by PayMob will allow the start-up to benefit long-term from the country’s shift to digital and non-cash payments.

“Where I see Paymob is in the 2.0 version. As debit and credit cards increase, you’ll need to use them in other places – that means acceptance online and offline. If you’re a new player or vendor, you need to be able to accept everything at point of sale, online and in-person. That’s what gives Paymob the edge.”

Digital wallets over digital banking

Global Ventures has also invested in Pyypl, a Dubai-based, blockchain-powered fintech trying to plug smartphone users into the financial system.

Whilst African mobile money providers such as MTN, Vodafone and Orange were around long before Pyypl, significant card penetration still hasn’t stretched beyond Nigeria or Egypt.

And it’s only in the last year that we’re seeing telco firms expanding into banking, which could lead to more cards.

In the Middle East, incumbent banks still place a “disproportionately high” value on debit cards.

This is according to Brandon Timinsky, founder of Pakistani fintech, SadaPay. He told FinTech Futures last May that many of the country’s debit cards still don’t let people shop online, and suffer high decline rates.

“The options today are mobile money or banks,” Pyypl’s co-founder and CEO, Antti Arponen, told FinTech Futures. “Mobile money services began 14 years ago – it’s old school. What’s missing is the in-between, the fintech companies.”

But instead of going down the digital challenger bank route, Pyypl is taking the payments-focused approach. It currently offers a digital wallet, prepaid card, mobile airtime top-up, as well as domestic user-to-user transfers.

Much like Mamo Pay, another Global Ventures portfolio firm, which processes instant everyday payments.

Moftah mentions that a lot of the digital banks in the region are evolving from the incumbents. Which is why fintechs are focusing predominantly on the payments play – where they see a bigger untapped opportunity.

Other than Bahrain and Saudi Arabia – where open banking has only just come into play – the MENA region lacks the regulation required for digital banking to take off.

Inventive approaches to credit

MENA also lacks no centralised credit scoring facilities for lending services, which makes it difficult for fintech lenders to launch in the region. Though Moftah acknowledges that “new players are trying to use alternative data sources”.

One such fintech in Global Ventures’ portfolio is Tabby, a buy now, pay later (BNPL) firm which raised $23 million in a debt and equity Series A. The raise closed less than six months after its $7 million seed.

“As banks across the region have tightened their credit policies and consumers increasingly seek ways to manage their finances, Tabby has seen tremendous market adoption,” the firm said last year.

Hossam Arab, Tabby’s founder and CEO, built the firm on data sources such as a telecom bill, or the type of phone a customer owns, in order to run valid, low-risk, credit checks.

Lean, a Global Ventures portfolio fintech, develops infrastructure to provide banks and other financial institutions with access to consumers’ financial data. Speaking to the investor’s desire to solve fintech at the infrastructure, as well as consumer, level.

As well as credit-based innovation, Moftah also cites a growing trading community across MENA.

Moftah says Saudi Arabia is home to the highest number of retail traders of all 22 MENA countries. Thndr, which Moftah dubs “the Robinhood of the Middle East”, is another one of Global Ventures’ portfolio companies.

Investors with decades of VC experience

Three-year-old Global Ventures, which started out in the United Arab Emirates, also employs team members on the ground in Saudi Arabia and Egypt.

Global Ventures partners Basil Moftah and Noor Sweid

“We see very different opportunities in these areas,” Moftah explains, pointing to the importance of locally informed investing. Global Ventures currently focuses on start-ups at the growth Series A stage.

“We’re a very research-driven VC, rather than just falling in love with entrepreneurs,” says Moftah. “Though we do fall in love with them too,” he laughs.

Of the VC’s 25 portfolio companies, eight are fintechs – making up roughly a third of its portfolio.

Before Global Ventures, Moftah grew a $400 million fund by the name of RVC for Reuters back in 1997. Colliding with the advent of the internet, it saw Moftah play a key role investing in the likes of Yahoo and Webex.

Moftah has known his VC partner, Noor Sweid, since they met at Harvard Business School.

Sweid is one of the only Arab women running a VC fund in the Middle East. She also became one of the first women in the region to head up an initial public offering (IPO) back in 2008 for the Dubai-based interiors contractor, Depa Ltd, which is co-founded by her father, Mohannad Sweid.

Sweid was also a founder of a yoga studio in Dubai, which she eventually sold to a private equity firm in 2014. She was then selected by the government to to lead investment for the Dubai Future Foundation two years later.

Read next: Pyypl’s regulation-first approach to MENA starts to pay off