Affirm’s IPO is a wake-up call for banks

Consumers possess more flexible purchasing power at the point-of-sale than ever before with the meteoric rise of embedded payments and financing options, which are easier and more transparent than traditional general purpose and private label credit cards.

Consumer demand for versatile payment options, coupled with a boom in e-commerce during a global pandemic, has led to 200% growth, signaling that we have arrived firmly in the consumer era of buy now, pay later (BNPL).

Affirm is placing pressure squarely on banks and fintechs to challenge its BNPL market share.

Affirm, one of the most recognisable brands in the space, has capitalised on these trends by blanketing the market with a core point-of-sale payment solution for consumers and merchants. With its recent initial public offering (IPO) filing, Affirm is placing pressure squarely on banks and fintechs to challenge its BNPL market share.

Affirm formally files to go public

So, how exactly did Affirm get here? More importantly, what does it mean for everyone else looking to hold court in the BNPL arena? Let’s take a closer look at some of the key disclosures provided in Affirm’s S-1.

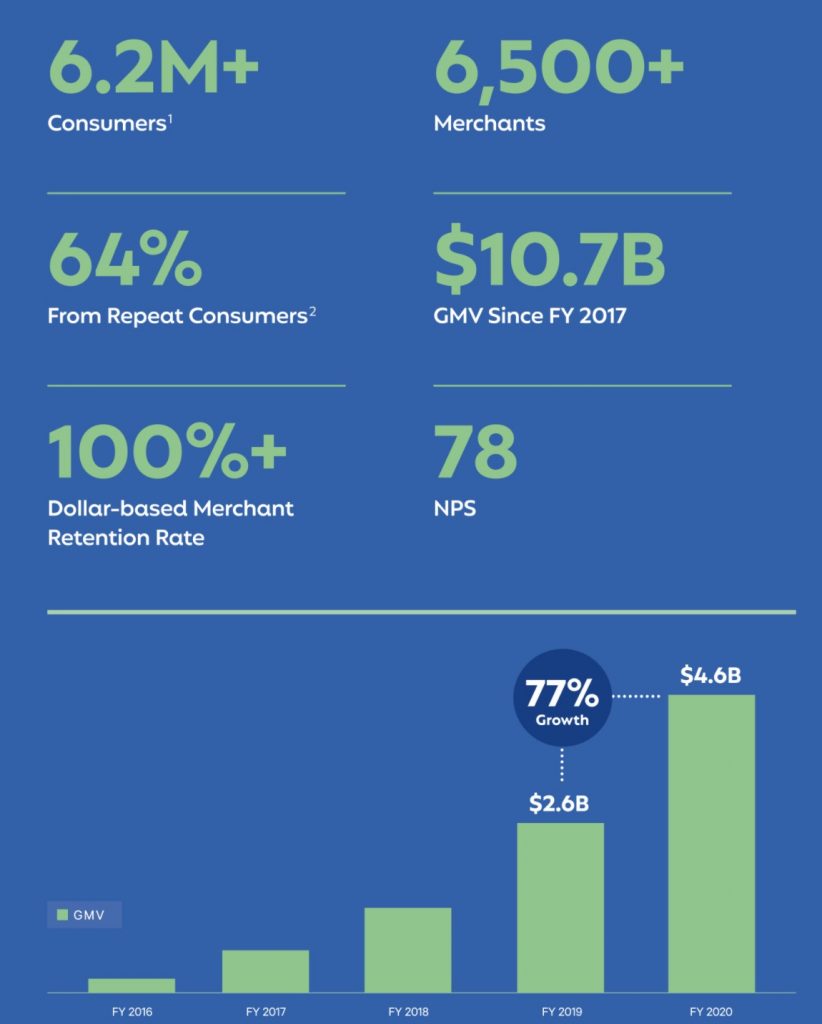

Numbers never lie. Affirm’s key statistics provide a clarion call to its competitors in the industry. As of September 30th, 2020, Affirm boasted 6.2 million customers and 6,500+ merchants, all while maintaining a net promoter score (NPS) of 78. The numbers are impressive and represent the key reasons Affirm is positioning itself to go public.

Source: Affirm

While these numbers signal a clear market presence for Affirm, the company still faces an uphill climb to correct annualised net losses of $112.6M.

The effects of the COVID-19 pandemic

Affirm’s success highlights how the COVID-19 pandemic accelerated the need for merchants to offer BNPL solutions.

Despite the pandemic, Affirm was able to grow its gross merchandise volume (GMV), the total value of transactions on the platform, to $4.6 billion. This growth represents a 77% year-over-year increase when compared to 2019. Growth numbers like these confirm the rapid acceleration of e-commerce growth that is occurring during the pandemic.

Interestingly enough, Affirm cites that it was also able to decrease portfolio delinquencies since the onset of COVID-19, highlighted by a tightening of its underwriting approval standards. Affirm’s approach was to purposefully hold back originations while concentrating on better performing assets, meaning growth could have been significantly greater without the de-risking of the portfolio.

The big picture? Affirm has successfully positioned itself as one of the key players in the BNPL marketplace. Having proven its ability to execute with merchants in a B2B model, the question remains whether Affirm can move toward meaningful profitability.

One thing is clear: Affirm’s announcement signals a wake-up call for banks to compete…and win.

What Affirm’s IPO means for banks

In my opinion, banks have been too slow to respond, but are ultimately well positioned to win. The time is now for banks to offer compelling BNPL solutions in order to retain their valuable merchant portfolios.

Affirm’s success has largely been driven by the broad consumer demand for financing options at the point-of-sale, most notably among younger generations of consumers. The filing cites a Harris Poll from 2020, stating that 64% of Americans would consider purchasing or applying for financial products through a technology company’s platform instead of a traditional financial services provider. That statistic rises to 81% for Americans ages 18 to 34 years. I suspect this increase is due to several factors:

- Greater access to budgeting tools, such as Mint and You Need a Budget (YNAB), are streamlining financial literacy for consumers across all generations.

- Younger generations are comfortable with subscription and pay-as-you-go models, with services like Netflix, Spotify and HelloFresh leading the way.

- Younger generations expect user-centered digital experiences to guide their interactions with leading consumer technology companies.

The most influential factor can be directly tied to the contrast of excess money in the pockets of younger generations compared to their predecessors. For example, annual salaries of Millennials are approximately 20% lower than that of the Baby Boomer Generation at the same age, after adjusting for inflation. In addition, the net worth of Americans ages 18 to 35 has decreased by 34% since 1996.

Simply put, consumers are sending clear signals. Keep them with you and your merchant portfolio by meeting the demand.

Online retail spending has increased by 77% year-on-year (YoY), with retail e-commerce revenue growth increasing by 68%, according to Forbes. By offering flexible financing options at the point-of-sale, merchants are able to further capitalise on this growth by acquiring consumers that may not have otherwise completed their purchase. At the same time, merchants are able to upsell and increase their average order value for those consumers already intending to make a purchase.

Simply put, merchants that offer flexible payment options to consumers increase their top line growth. Don’t you want them to share that success with your bank instead of a fintech challenger? I think so.

How banks can respond

The rise of BNPL presents an incredible opportunity for banks to deepen their relationships with both merchant partners and consumers. Legacy merchant brands are trusted by millions. By offering point-of-sale financing through these merchants, banks and financial institutions are able to grow their consumer base at virtually zero cost of acquisition.

Land and expand

It’s no longer enough for banks to hang their hats on revolving co-branded credit card offerings at the point-of-sale. Instead, banks have to be armed with both in order to compete in the current climate. Boasting a 20% compound annual growth rate, versus 3% with traditional co-branded credit card offerings, BNPL offers banks the asset growth they are seeking.

Leverage the expertise

Point-of-sale financing provides credit diversification for banks and financial institutions. Many banks have decades-worth of experience in marketing, analytics, underwriting and risk management that will enable them to compete, and ultimately win, in the BNPL space. The extensibility of these core competencies into point-of-sale is clear. The same reliabilities that banks have consistently relied upon through numerous economic cycles apply to this burgeoning opportunity as well.

A clear cost-of-capital advantage

The macro environment and markets are unpredictable. 2020 demonstrated that in spades. Traditional banks possess a clear balance sheet and cost-of-capital advantage. These large institutions are simply better equipped to offer greater stability as economic headwinds come and go.

Simply put: Fintech point-of-sale lenders do not have access to the low cost of funds stemming from deposits that banks enjoy. They rely on funding from capital markets, lines-of-credit and whole loan sales. These are the exact funding mechanisms that carry the most volatility in times of economic uncertainty.

Now is the time to compete and win

The opportunity is clear. Banks need to compete and ultimately win the battle for point-of-sale financing. BNPL presents clear value for all consumers, merchants and banks alike. Affirm’s success clearly illustrates the size of this market, but we are still in early innings.

It is ‘all systems grow’ for point-of-sale financing, but banks must grow the right way. Innovating swiftly with the right technology partner will enable smart growth.