FCA and UK Treasury “acting swiftly” to regulate fast-growing BNPL firms

The Financial Conduct Authority (FCA) and HM Treasury both released statements yesterday expressing their joint intent to reign in buy now, pay later (BNPL) fintechs.

The much-anticipated Woolard Review, published on Tuesday, calls on the UK’s government to address the “urgent need” for “amendments to legislation” in the unsecured credit market “as soon as possible”.

The Treasury, complimenting the review’s call to action, acknowledged BNPL firms are “rapidly increasing in popularity”, noting that the volume of BNPL transactions tripled in 2020.

“There is now a significant risk that these agreements could cause harm to consumers,” it states. “By announcing plans to legislate […], the government is acting swiftly to ensure people can continue to benefit from these products with the right protections.”

The Woolard review sets out the requirement for a public timetable to implement legislative change. As well as annual meetings of the FCA’s board to assess progress.

Current legislation is nearly 50 years old. The likes of Klarna, Clearpay, and Laybuy all say they fully support new regulation better suited to a digital age, despite benefitting hugely from the lack of regulation.

Why now?

Organisations, individuals, and campaigns have long called for more regulation around the unsecured lending space.

Luke Massie, CEO of UK fintech VibePay, tells FinTech Futures BNPL firms’ messaging is “glamourising credit and not educating on the risks”.

Resolver received 4,962 complaints about BNPL credit providers between April and September last year. That’s up 22% on the previous six months.

On Trustpilot, a common complaint is firms continue to withdraw payments even if an item is faulty or refunded. Other customers claim to have only received partial refunds – some as low as 25% of the original purchase.

The FCA is anxious about the number of citizens who will find themselves in debt

For Klarna, complaints have culminated in the birth of the “KlarNAA” campaign. But the fintech claims – according to its own data – that it receives just four complaints for every 10,000 purchases.

Last month, a group of more than 70 cross-party MPs – led by Labour’s Stella Creasy – tabled an amendment to the financial services bill to regulate BNPL firms.

The group wanted to push through regulations within three months of the bill passing, but the UK government voted down the bill.

The coordinated FCA and Treasury announcements yesterday seem to have renewed this temporarily lost legislative momentum.

Risk of debt

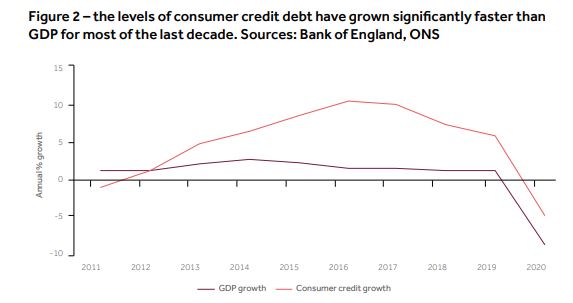

The BNPL market, which is now worth £2.7 billion in the UK alone, has served some five million Brits since the beginning of the COVID-19 pandemic.

According to the FCA’s review, more than one in ten people using BNPL products are already in arrears – i.e. have missed a payment due date.

With the post-pandemic recovery looming as the UK endures what it hopes will be its final lockdown, the FCA is anxious about the number of citizens who will find themselves in debt.

“COVID-19 will leave many open to financial shocks for some time to come. Increasing the demand for debt advice,” the review reads.

It estimates demand for debt advice will likely “more than double”, with 1.5 million more people needing it post-pandemic. Part of this, it says, is down to “the relative lack of mid-cost options for sub-prime customers”.

According to a study by money.co.uk, just 22% of the nation didn’t carry personal debt into 2021. The average British adult ended 2020 with £9,246 worth of total debt.

Comparison to Wonga

In January, Creasy said the likes of Klarna, Laybuy, and Clearpay are “the next Wonga waiting to happen”.

A Klarna spokesperson says it rejects the Wonga comparison

Payday lender Wonga collapsed in August 2018. Post-crash, thousands of customers were still trying to recover claims for compensation due to mis-sold loans.

But the Financial Ombudsman stopped investigating these claims when it became clear Wonga wouldn’t be able to pay up.

The fall of Wonga has seen a rapid decline in the number of payday lenders ever since on the UK high street. The likes of The Money Shop, QuickQuid, H&T, PiggyBank, My Money Partner and Swift Sterling have all since disappeared.

In the FCA review published yesterday, the regulator says that “while the emergence of unregulated BNPL products has provided a meaningful alternative to payday loans”, the market also “represents a significant potential consumer harm”.

A Klarna spokesperson reached out to FinTech Futures in January to say it “absolutely reject[s] any comparison to payday loans”.

“We are a fully licensed bank and, unlike payday loans, we charge no interest and no fees on our most popular products,” they added.

A better credit market

As well as calling for emergency legislation, the FCA’s review also highlights the opportunity to build “a better credit information market”.

“There is a genuine opportunity here not just to respond to the challenges elsewhere in this report, but to build a better system for the future,” it reads.

The regulator muses different plans of action. These include a mandatory reporting requirement. Assessing the barriers to “widespread use of open banking data”. The FCA updating its disclosure requirements. And adding a credit builder product focus to the FCA’s Regulatory Sandbox.

Freddy Kelly, co-founder of Credit Kudos, highlights the limited data available to lenders at present. “All lenders have faced challenges in assessing an individual’s affordability in these uncertain times. With traditional credit reports providing limited information on someone’s current financial situation.”

Whilst Ian Hooper, UK banking and payments head at Capco, thinks banks could help to balance the market.

“There is a clear opportunity for mainstream lenders to step into the ring and provide alternatives to high-cost credit in order to ensure a sustainable credit market.”

Read next: Affirm IPO sees shares surge 98%