State of play: account-to-account (A2A) payments

State of Play: Account-to-account (A2A) payments – in-depth analysis and understanding of the market landscape

Introducing a new regular column – State of Play – at FinTech Futures. Each month, fintech analyst Philip Benton explores a new topic and assesses the “state of play”, providing an in-depth analysis and understanding of the market landscape.

The first dive is into account-to-account (A2A) payments.

A2A payments is nothing new; bank transfer services have existed for many years and traditionally been used by consumers to schedule regular bill payments (i.e. direct debit), but through open banking and real-time payments, A2A has a genuine opportunity to become a credible rival to the card payment rail for everyday transactions too.

Financial services have undergone a digital transformation which has seen banks move from legacy infrastructure to modern cloud-based technology but payment rails, although evolving, largely rely on traditional card networks.

The introduction of open banking allows third parties to initiate payments on behalf of consumers as a registered PISP (payment initiation service provider) and making payments directly from a bank account and potentially reducing fees for merchants, banks and the consumer. With Mastercard announcing it will increase its interchange fees from October 2021 for UK consumers buying from Europe, and rumours that a merchant fee hike – delayed by the pandemic – will be reintroduced by Visa/Mastercard, A2A has a unique opportunity to capitalise.

Despite it being early days for A2A payments it has already been identified by payment issuers/acquirers as the number one opportunity of open banking according to Omdia’s ICT Enterprise Survey (ICTEI) 2020/21 – a study comprising more than 6,600 interviews of CIOs and other senior IT decision-makers conducted between July and September 2020. Bank transfers or Automated Clearing House (ACH) payments are already a common payment method for online payments and estimated to account for 8% of global ecommerce payments in 2020 according to Worldpay’s 2021 Global Payments Report.

Consumer adoption of A2A payments has be driven by merchants

Although there are encouraging signs, there is still a long way to go before A2A payments can be considered mainstream. According to researchers at UCL, it takes, on average, 66 days to get a consumer to change habits, with payment behaviour one of the most difficult habits to change – hence the longevity of cash.

Although A2A payments have many obvious benefits to the consumer, they will require incentives from the merchant to drive behavioural change.

Several stakeholders are starting to initiate such change, including Lithuanian payment start-up kevin. which is seeking to cut out the card networks at the checkout. kevin.’s software identifies the related bank when customers type in the first eight digits of their card number and gives the customer the option to switch to a bank payment, explaining that this is “faster, safer and easier” due to no card and CVV being required.

With A2A up to 90% cheaper for merchants, if a proportion of this saving was passed onto the consumer it would surely incentivise the consumer to switch. In closed beta testing, kevin. says 10% of customers chose to switch from debit to A2A payments.

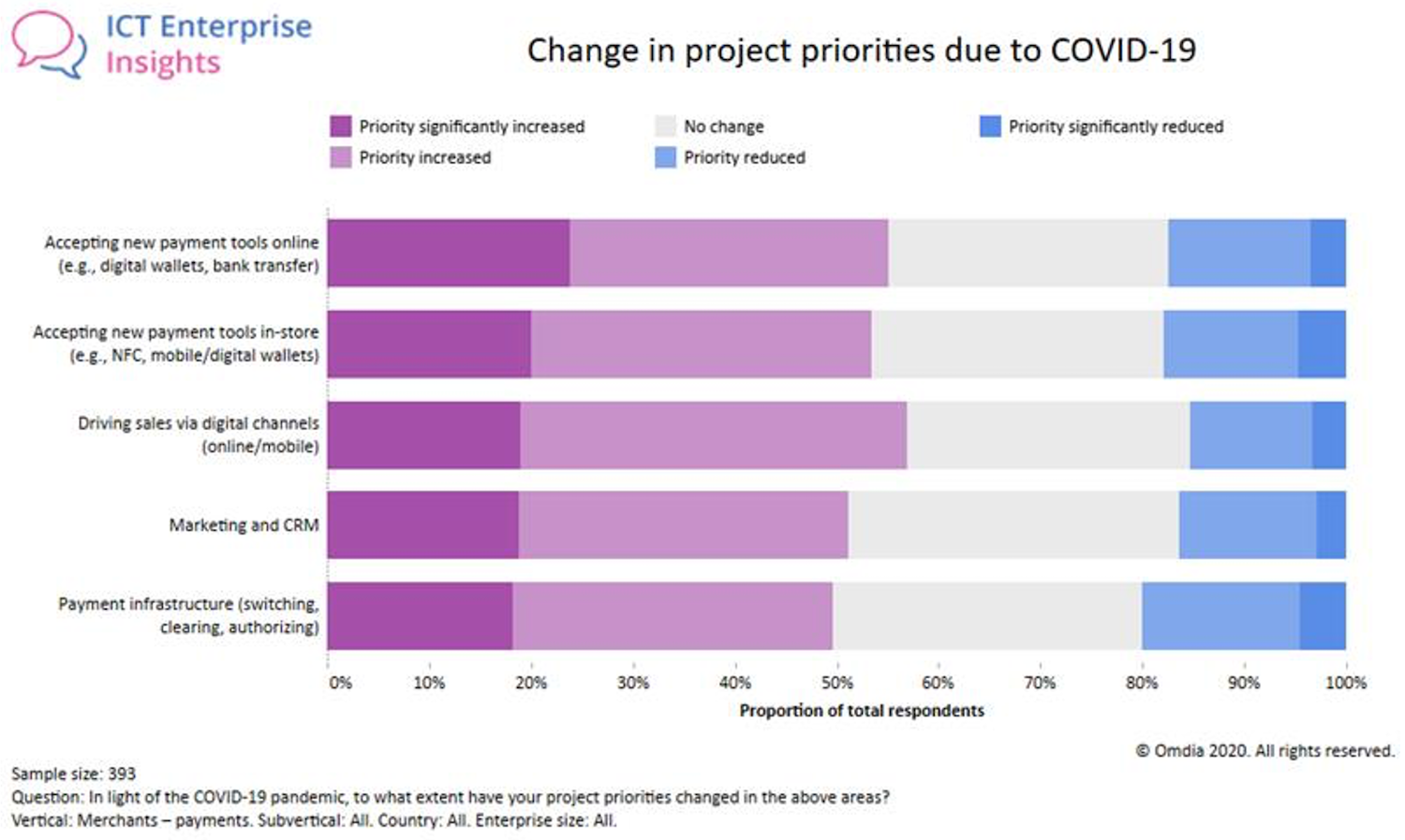

COVID-19 has prompted merchants to look beyond card payments

Source: Omdia ICT Enterprise Insights 2020/21

The pandemic has encouraged merchants to radically rethink their payment strategies, with one in four merchants surveyed by Omdia stating that accepting new payment tools online has significantly increased in priority. This is particularly true of the grocery sector (whereby three in four merchants stated the need to increase their capacity to accept new payment tools online), having seen such strong growth online, and are obviously deeply incentivised to reduce their processing costs on such frequent transactions.

A2A payments could be an unintended beneficiary of SCA

The exponential growth of e-commerce transactions has also caused a surge in payment fraud which remains a critical challenge for banks with the card payment fraud the most common. In the UK alone, card fraud totalled £621 million in 2019 and remote purchase (card not present) accounting for 76% of total card fraud losses, according to UK Finance. In Europe, fraud has been recognised as a huge problem across e-commerce transactions which is why they are implementing strong customer authentication (SCA) as a requirement for all online transactions above €50 in 2021.

SCA requires the consumer to have two forms of authentication to process the transaction which could cause friction for consumers. Utilising A2A payment will naturally meet the multi-factor authentication requirements as it requires the consumer to authenticate each individual payment through their banking app. Issuer banks may see a fall in card revenues but a reduction in fraud and chargeback losses will have a transformative impact on the business model of a retail bank.

Payments industry is planning for a “cardless” world

Card issuers and networks are understandably reluctant to encourage consumers to adopt alternative payment methods because of the commercial interest in maintaining card revenue. However, it is clear that the legacy technology is not going to meet the needs and demands of the consumer in the future. Change is inevitable, predicated by open banking, which banks, merchants and ultimately consumers will adopt.

Legacy card networks are taking the threat of A2A payments to their existing payment rail business seriously by diversifying their product portfolio with a series of strategic acquisitions and product launches which should indicate to the rest of the industry the direction this is heading.

Mastercard has been quick to recognise the threat to its card payment business with the 2017 acquisition of Vocalink, the UK-based payments system company, and the 2019 purchase of Nets’ A2A payment business – completed this month after regulatory approval. American Express launched its Pay by Bank Transfer service in 2019 that enables UK consumers to make real-time payments for goods and services online direct from their bank account utilising open banking technology even if they are not American Express cardholders.

New wave of challengers investing in the A2A payment rail

Banks themselves are seeking to gain more control of the payment rails that no longer relies on the card network duopoly of Visa/Mastercard with the Eurozone’s major banks starting the European Payments Initiative which looks to implement a standalone digital payments scheme. As it was designed, open banking also enables access for a range of new competitors to compete for a share of the A2A payments ecosystem including start-ups Banked, Trustly, Finx, Trilo and Token as well as established market players ACI Worldwide, Worldpay and BNP Paribas all launching A2A-focused platforms.

A2A payments is one of many alternative payment methods that is gaining prominence. QR payments, digital wallets, buy now pay later (BNPL), cryptocurrency and stablecoins are just a few of the emerging payment methods as the shift away from card payment dominance gathers pace.

A2A payments can underpin a digital wallet, QR payment or even a cryptocurrency transaction at a fraction of the cost of the card networks and 2021 will likely see A2A payments adopted on a much wider scale by merchants and consumers alike.

About the author

Philip Benton is a senior fintech analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

Philip Benton is a senior fintech analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

In this column, Philip will discuss the technological implications and consumer expectations of the latest fintech trends.

You can find more of Philip’s views on fintech via LinkedIn or follow him on Twitter @bentonfintech.