State of play: digital wallets / super apps

Introducing a new regular column – State of Play – at FinTech Futures. Each month, fintech analyst Philip Benton explores a new topic and assesses the “state of play”, providing an in-depth analysis and understanding of the market landscape.

This month we are diving into digital wallets / super apps.

Digital wallets are exactly what you expect, a way of storing everything you would find in your physical wallet but online. The earliest iteration of a digital wallet was PayPal, founded in late 1990s, designed as a means of storing credit card details to make payments online. However, it wasn’t until the birth of the smartphone that digital wallets developed into mobile wallets and gained mass popularity both for online and in-store payments that spawned rapid adoption worldwide.

Digital wallets adoption have been steadily growing for a number of years but COVID-19 accelerated the trend for online and in-store payments as merchants number one priority shifted to increasing acceptance of new payment tools (such as digital wallets), according to Omdia’s Merchant Survey.

Accepting new payment tools key IT priority for merchants

Digital wallets are also an unintended beneficiary of the Strong Customer Authentication (SCA) regulation – which is being rolled out in Europe throughout 2021. Digital wallets, particularly when used on mobile, naturally meets multi-factor authentication rules and provide a more seamless experience for the consumer thus improving conversion rates for the merchant compared to traditional payment methods such as debit/credit cards.

In fact, digital wallets have now become the world’s leading payment method for both e-commerce and point of sale (POS) transactions, according to Worldpay’s 2021 Global Payments Report, and are forecast to account for more than half of e-commerce payments and a third of POS transactions by 2024.

In some regions, digital wallets have evolved into so-called “super apps” whereby they have diversified beyond money management into restaurant bookings, taxi hailing, food delivery and even gaming. However, the use cases driving adoption of digital wallets/super apps is variable across the world and different revenue drivers have emerged which I’ll explore in depth.

Birth of wallets: seamless payment journeys

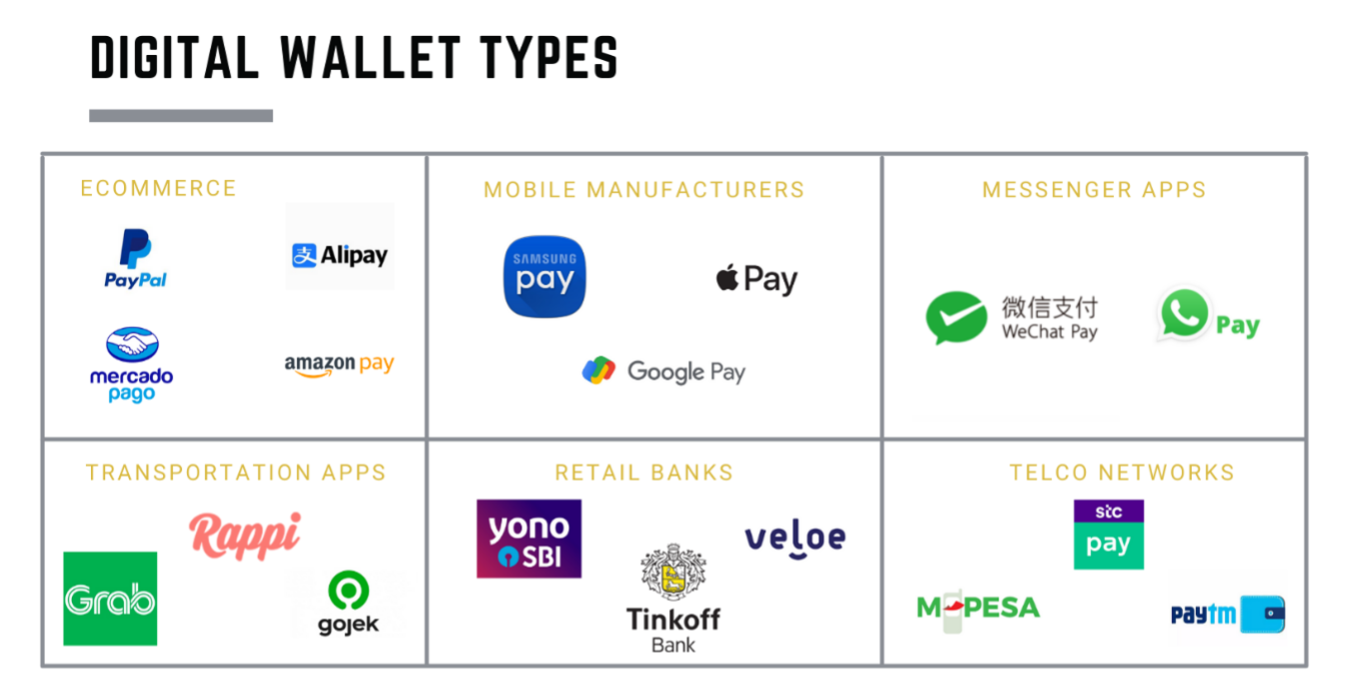

There are hundreds, possibly thousands of digital wallet providers worldwide all designed to make payment easier and more efficient. However, very few wallet providers start off in payments with many coming from adjacent industries which have added payment functionality to their portfolio usually to enhance the user experience and keep the customer in their ecosystem. The main types are outlined below, or at least where they started out. I have largely ignored peer-to-peer (P2P) wallets (i.e. Venmo, Zelle, Wise) and focused my attention on wallets which have broad merchant acceptance.

A digital wallet was conceived to be effectively a “card-on-file” which enabled the consumer to avoid having to enter card details multiple times as the wallet simply required the user enter a single password to authenticate payment. Thus, commerce sites such as Alibaba, Amazon and Mercado set up their own digital wallets to make it easier to make payments on their own sites before recognising the benefits of extending this to third-party websites. PayPal, as the first global wallet brand, is relatively unique that it wasn’t initially tied to a specific website (although eBay’s acquisition in 2002 saw PayPal become synonymous with the online auction site). Increasingly there have been wallets launched which are not tied to a specific merchant, for example Shopify (Shop Pay) and FIS (GoCart) have both recently added checkout payment functionality to its suite of e-commerce platform tools.

Although digital wallets were initially designed to make online payments more seamless, it was the introduction of QR codes in Asia and NFC technology in Europe and North America which saw mobile digital wallets take off as an in-store payment method, too.

AliPay and WeChat Pay have led the adoption drive in China with digital wallets now accounting for 72% of e-commerce transactions and 50% of POS transactions.

In Europe, QR codes are not as prevalent but NFC technology was widely utilised which led initially to a boon in contactless card payments during the early 2010s. Apple Pay and Google Pay utilised the same NFC technology to enable consumers to use their mobile to make contactless payments which was quickly adopted by merchants and consumers alike as a new payment method.

North America, on the other hand, was initially slower to adopt new payment methods and COVID-19 has acted as a major accelerator of the digital wallet trend which saw adoption increase to 29% in 2020 from 24% in 2019, according to Worldpay’s Global Payments Report 2021.

Serving the unbanked community

Although it is rightly assumed that digital wallets have largely replaced card payments in regions which have highly banked populations, they have also appealed to unbanked consumers who previously relied upon cash. M-Pesa is the best example of such a trend, with the Kenyan mobile money service being launched by the country’s leading telecommunications operator, Safaricom in partnership with Vodafone at a time when the banked population in Kenya was very low. Payments on M-Pesa are made via SMS utilising USSD technology meaning anybody with a mobile phone can use the service.

Latin American start-up Rappi and Indonesian transportation app GoJek have also diversified into payments by targeting unbanked consumers with an alternative to bank accounts. RappiPay even provides its customers with their own payment cards that can be used to spend outside of the Rappi ecosystem.

Banks have, in turn, used digital wallets as a spur to accelerate their own customer acquisition. Dashen, an Ethiopian bank, created its own digital wallet – Amole – in 2018 and was able to grow its digital customer base from 50,000 to over two million by the end of 2020. State Bank of India (SBI) launched YONO (You Only Need One) as a separate entity in November 2017 and now has over 27 million registered users with the app allowing customers to bank, shop, travel, pay bills and invest all in a single app.

The “super app” trend is being increasingly adopted by banks globally with Tinkoff, the Russian neobank, focusing on “lifestyle banking” as a means to compete with other digital wallets and enables its customers to bank, invest, book trips and restaurants all whilst earning loyalty points such as cashback, bonuses and air miles.

Rise of the super app

What does it take for a digital wallet to achieve the “super app” status?

Digital wallets are increasingly attempting to morph into “super apps” as the fintech world looks to emulate the success of WeChat and AliPay – which account for more than 90% of digital payments in China. WeChat started life as a messaging app and sought to add gaming, shopping and payments to its portfolio as an incentive for users to stay in its ecosystem.

WhatsApp is attempting to replicate the success of WeChat by adding payments to its service in Brazil and India as well as in partnership with Nedbank in South Africa.

Ultimately, the success of the Chinese super apps has been due to the high volumes of data they have harvested which allows them to launch services that are highly relevant for specific users as well as being more affordable and convenient to purchase on their ecosystem. Stricter regulation outside of China (although Chinese regulators have recently taken a much stronger stance on WeChat/AliPay) means it is much more difficult for other digital wallet providers to achieve such duopoly success.

Digital wallets have been increasingly adopted thanks to the convenience of making payments, whether the consumer was previously accustomed to paying by card or cash. Whilst digital wallets have largely benefited from the growth of e-commerce, the introduction of QR codes was the fundamental reason behind success as an in-store payment in Asia which is beginning to become more prevalent in other regions too – particularly as the world adjusts to a post COVID-19 environment.

Digital wallets will continue to thrive in the open banking era which creates new opportunities to build services on top of banking data that enable financial services to be more accessible, relevant, valuable and affordable to consumers.

New payment methods such as buy now, pay later (BNPL) and account-to-account (A2A) payments have emerged as well as cryptocurrencies and central bank digital currencies (CBDC) which require a common platform to flourish – digital wallets fit the bill.

Many digital wallets have the existing user base but ultimately need the consumer’s trust if they are willing to manage their finances and lifestyle in a single ecosystem and for the digital wallet to achieve “super app” status.

About the author

Philip Benton is a senior fintech analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

Philip Benton is a senior fintech analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

In this column, Philip will discuss the technological implications and consumer expectations of the latest fintech trends.

You can find more of Philip’s views on fintech via LinkedIn or follow him on Twitter @bentonfintech.