Sibos 2021: Minna Technologies – making subscriptions management easy

The rocketing subscription-based revenue model is lucrative for merchants; recurring, smooth cash flows make for great projections and growth. Consumers benefit from an ease of choice and flexibility of purchasing options and cadence. A win, win. But is it?

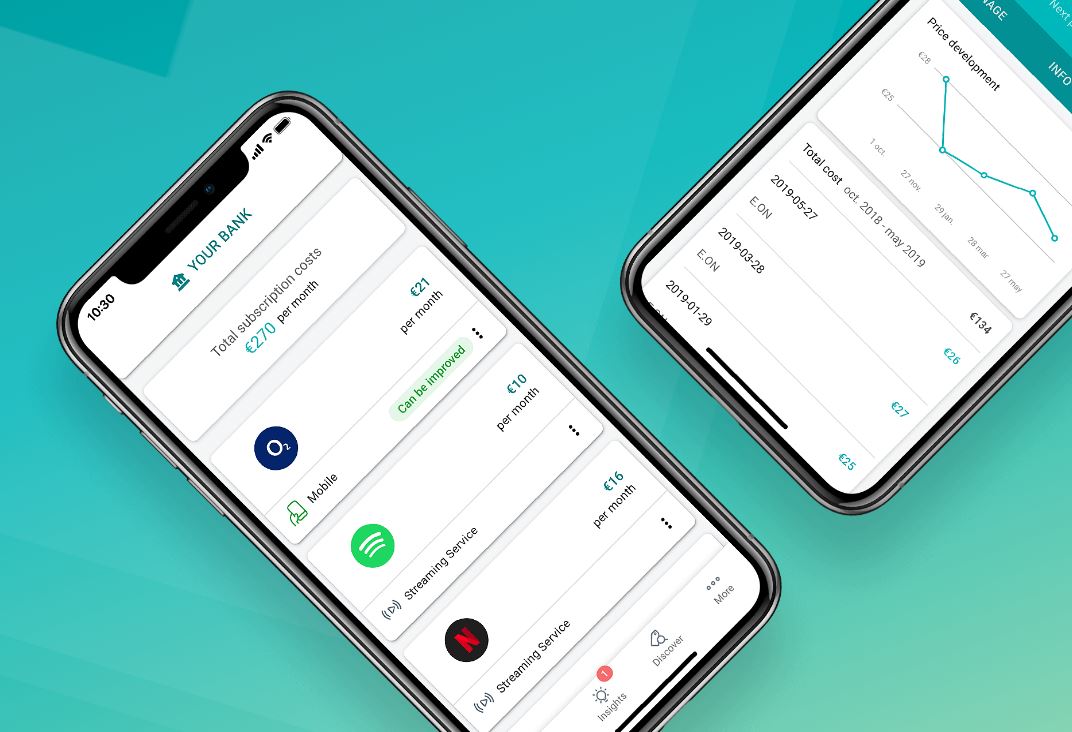

Minna’s solution has reach and global ambitions – around 20 million people already benefit from it

There is friction.

Consumers, although willing to sign up to trials and subscriptions, can become overwhelmed, oscillating between “subscription addiction” and “subscription fatigue”. They lack the means to easily see and manage their subscriptions, and ultimately, their spend.

The process for pausing and cancelling a subscription can be time-consuming and frustrating, if you can manage to find your subscription spend in the first place.

In the UK and the US, banks are mandated by the regulator to get involved and mediate these transactions in hopes of consumer protection This is good news in an open banking world because, especially with the trends of embedded fintech, services can be layered into native banking environments to help customers stay “subscription savvy”. But given the velocity of the subscription trend, the unforeseen consequence is an increase of management cost and a decrease in operational efficiency.

But, what seems like a simple process, actually leads to a few lesser known outcomes. When a customer goes through their bank, merchants receive a block payment for 13 months before they can engage with that customer again.

Furthermore, if a consumer cancels this way, very little insights are shared; do they just want to put a pause because it is no longer “seasonally” appropriate e.g. as a football fanatic, you want to pause your streaming sports subscription but you will be back next season. Are you a subscription “tourist” or a “local” who is here to stay? With blocks, little is known. In a world of soaring customer acquisition costs, a retained client regularly trumps a new client.

It’s not much fun for banks either. Fielding phone calls and disputes around subscriptions costs money, and that amount is only increasing. By way of context, Minna Technologies’ UK-based client Lloyds Banking Group, in 2021 received around 100,000 calls each month for subscription services, estimating the annual cost to the bank of more than 70 million for subscription calls alone.

As subscriptions continue to take up a wider share of wallet, how can the market keep up?

Happily, help is at hand.

Our solution solves these problems. It fills the connectivity gap between the bank and that of the consumer and merchant. By providing subscriptions management that sits within a banking app, the consumer can see all of his or her subscriptions and cancel or pause them him or herself. Being able to self-direct and have control, the customer becomes empowered and more confident in using subscriptions services.

Joakim Sjöblom, CEO & co-founder, Minna

Merchants, of which Minna holds relationships with more than 10,000 globally, can retain and better understand their clients. Rather than losing clients, it empowers them to retain their existing customers while increasing the life-time value of each user. In a world of subscription fatigue and rising customer acquisition costs, retention is key.

Finally, banks save costs while having happy, digitally engaged and self-served customers. Lloyds Banking Group saw a 27% reduction in call volumes within the first three months of implementation. Banks know that customer experience is king and are increasingly open to fintech partnerships to achieve this. By providing a banking experience that is open, connected, and intelligent, they gain the customer’s trust, which promotes longevity in the relationship. Best of all, through the efficiency of the connectivity, customers can unlock capital, theoretically freeing it up for allocation elsewhere, say, into a savings or investment product.

Our solution has reach and global ambitions. In terms of merchants and banks – around 20 million people benefit from our subscription solutions. Currently partnered with top-tier European and UK banks such as Lloyds Banking Group and its component parts, Swedbank, Danske Bank and ING, 2022 strategy includes expansion into the US and Australia. We are supported by some of the biggest financial companies in the world, having completed Series B funding in January 2021 to the tune of €15.5 million (£14 million).

In addition, Minna is a member of the Visa Fast Track Programme in Europe, and joined Visa’s Global FinTech Partner Connect Program in the US and Australia in July 2021.

![]()

Click here to read Minna Technologies’ 2021 US Mobile Banking Benchmark Report