State of play: central bank digital currencies (CBDCs)

Introducing a new regular column – State of Play – at FinTech Futures. Each month, fintech analyst Philip Benton explores a new topic and assesses the “state of play”, providing an in-depth analysis and understanding of the market landscape.

This month we are diving into central bank digital currencies (CBDCs).

It’s safe to say that 2021 has been a breakout year for cryptocurrency.

Bitcoin has hit all-time highs multiple times, almost all the incumbents are starting to recognise crypto as much more than just a fad or meme, and every tech company is hiring a cryptocurrency team from Twitter to Bumble.

Now, governments are engaging in crypto too through the exploration of central bank digital currencies, also known as CBDCs.

The ideation of CBDCs first emerged decades ago, but in recent years, discussions have ramped up amongst central banks after Facebook (Meta Platforms) announced their Libra (now Diem) project in 2019, with 80% of the world’s central banks now exploring CBDC projects, according to the Bank of International Settlement.

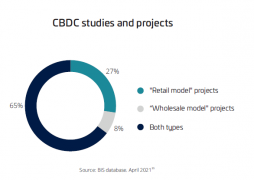

There are clear benefits to the use of CBDCs for both retail and wholesale payments, which is reflected in the majority of CBDC studies and projects looking at both model types.

Despite most central banks still planning their frameworks for what a CBDC might look like, there are already several CBDCs that have gone live, the most established of which being the Bahamian Sand Dollar which launched in October 2020.

The Sand Dollar was launched in the aftermath of Hurricane Dorian and the COVID-19 pandemic which forced the Bahamian central bank to accelerate its CBDC project and enable its citizens to easily access relief in the event of cash being hard to access.

The CBDC is available through a digital wallet and payment card but doesn’t require a bank account to utilise the digital currency, with the initiative designed to encourage financial inclusion.

Cambodia (Project Bakon), the Eastern Caribbean States (DCash) and most recently Nigeria (eNaria) have followed, with the Nigerian government swiftly introducing eNaira in an effort to stamp out cryptocurrency trading and maintain control of their own money infrastructure.

El Salvador has taken an altogether different approach by being the first country to adopt Bitcoin as legal tender. In terms of developed nations, China (e-CNY) and Sweden (e-krona) are the most advanced with extensive pilots having already taken place, and China is expecting to further test its CBDC – digital yuan – during the Winter Olympics in early 2022.

Is CBDC the first step towards a cashless society?

Central bank digital currencies aren’t necessarily going to be a replacement for cash. Despite the growing calls for cashless societies, cash is likely to survive for decades to come.

So, what is the point of CBDC? Well, it is about designing money systems which are cheaper, more efficient and more accessible. The adoption of alternative payment methods such as crypto, account-to-account and QR payments are becoming increasingly important to payment issuing and acquiring banks (see below chart).

This has been in part accelerated by the pandemic, as merchants and consumers adopted emerging and more convenient forms of payments and reduced their reliance on traditional payments such as card and cash.

Source: Omdia ICT Enterprise Insights 2021/22

Central banks have also recognised this changing landscape and realise that if they don’t adapt, they will lose control over their own money infrastructure.

Facebook (Meta Platforms) certainly spooked money regulators worldwide when they announced the Libra (now Diem) project as central banks foresaw the threat a decentralised currency poses if a platform with almost 3 billion users could create a payment method that is widely adopted. Despite early setbacks to the Diem project, with major partners like PayPal, Visa and Mastercard pulling out, the cryptocurrency is still set for launch in 2022.

CBDCs can be issued in two forms, either directly through bank accounts or tokenised through a digital wallet. If account based, CBDCs could be issued either directly by central banks or indirectly through commercial banks. Most governments are likely to adopt the indirect model due to fears around liquidity risks for commercial banks if the CBDC was issued directly by the central bank.

CBDCs are also able to be issued as tokens via a digital wallet, which would operate much like existing private cryptocurrency transactions and could be adopted by the unbanked population.

Digital wallets are prime vehicles for distributing CBDCs as it is already the world’s leading payment method for both e-commerce and point of sale (POS) transactions, according to Worldpay’s 2021 Global Payments Report.

Public and private partnerships key for the success of CBDCs

Governments realise that cryptocurrencies are here to stay and the majority of CBDCs are being introduced to ensure their monetary system stays relevant to consumer demands and not necessarily to eradicate the use of Bitcoin and other private cryptocurrencies.

China is the obvious exception (also Nigeria as earlier mentioned), with their stance on crypto becoming increasingly aggressive – banning overseas crypto exchanges in September 2021, for example – in order to drive adoption of the digital yuan (e-CNY).

Other governments are instead seeking to regulate cryptocurrencies, with the European Central Bank (ECB) recently approving a new oversight framework for electronic payments which will include coverage of stablecoins and other crypto assets.

CBDCs should coexist and interact with other payment schemes, but central banks must also ensure they aren’t in direct competition with commercial banks. The CBDC framework is required to balance the needs of central banks and governments with consumers, merchants and corporations.

Central banks will therefore need to cooperate with commercial banks to ensure mass adoption – China is collaborating with both state-owned banks and MYBank (Alibaba) to maximise the rollout potential of its digital yuan.

Interoperability with existing payment systems is the very minimum requirement, but the real benefit for CBDCs is cross-border functionality for global transactions. For this to happen, governments need to agree on common standards for CBDCs to be as ubiquitous as the internet. These standards should build upon the principles of decentralised cryptocurrencies that operate today and seek to provide a global monetary system that is efficient, flexible and accessible yet affordable.

Building this infrastructure will require the collaboration of both public and private companies with CBDCs necessitating new payment rails to be designed to facilitate interoperability between different crypto and digital currencies.

Visa has recognised the opportunity for a network to connect different digital currencies and is working on a ‘universal payment channel’ (UPC) that will act like a hub, interconnecting multiple blockchain networks and allowing for the transfer of digital currencies.

In the public sector, the multiple CBDC bridge project (mBridge) – which includes the monetary authorities of Hong Kong, Thailand, China and the UAE as members – is working on a prototype which can lead to faster money transfers when combining CBDCs with blockchain infrastructure.

Outlook for CBDCs

How quickly central bank digital currencies are launched and thereafter adopted will be dictated by the success of two major digital currency projects, Diem and e-CNY, which policymakers worldwide will be observing closely to ascertain the societal, economical and political demand for CBDC.

Wholesale CBDCs are likely to be adopted more quickly due to immediate cost savings and efficiencies of transacting international payments on blockchain/distributed ledger technology. Over 20% of respondents stated this was in their top three priorities for the next 18 months according to a Omdia Corporate Banking Survey, but retail CBDCs will follow soon after.

CBDCs are a natural evolution of the money system and to be successful, they must have interoperability at their core if they are to be adopted at mass scale with the same enthusiasm that consumers have for private cryptocurrencies.

About the author

Philip Benton is a senior fintech analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

Philip Benton is a senior fintech analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

In this column, Philip will discuss the technological implications and consumer expectations of the latest fintech trends.

You can find more of Philip’s views on fintech via LinkedIn or follow him on Twitter @bentonfintech.