Should digital banking platforms be fraud prevention solutions by design?

As banks race to keep up with the latest fraud threat vectors, they should focus on driving technological as well as commercial outcomes from their investments by converging digital banking platforms into a complete, well-integrated, and agile fraud solution.

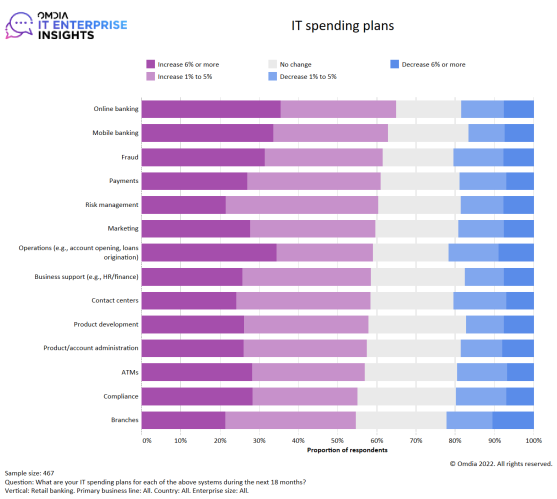

According to Omdia’s IT Enterprise Insights 2022/23 Survey, more than six in 10 retail banks plan to increase their IT spending on fraud management in 2023 and nearly a quarter of them plan to increase it by 6% or more. This is partly driven by increasing customer protection requirements. The growth of synthetic ID, application, and authorised push payment (APP) fraud require strong transaction monitoring and wider analytical approaches in detecting suspect activity.

IT spending plans for retail banks. Source: Omdia IT Enterprise Insights 2022/23 Survey

However, many existing fraud solutions currently used by banks are poorly integrated with the organisation’s broader objectives, which is detrimental to customer satisfaction and the bank itself. As regulators continue to become more interventionist, institutions should seek out opportunities to gain both technological and commercial outcomes from their fraud platform investments.

Banks that continue to rely on legacy systems will expose themselves to greater risks

Online and mobile banking have been the most high-profile elements of technological investment in recent years, with banks prioritising personalised (23%) and consistent customer experience (22%) as well as cross-channel visibility of customer activity (20%) to achieve success in their front-office omnichannel banking strategies.

As they strive to ward off competition from neobanks and meet customer expectations for a seamless and good-value banking experience, they must balance product and service innovation with the evolving risk of fraud. Those that continue to rely on legacy systems will be exposing themselves to greater risks and potentially damage to their brand. The pace of technological advancement means that banks must incorporate and exploit newer technologies quickly to remain competitive without creating or enlarging areas of risk. By focusing on converging their digital banking platforms into a complete and adaptable fraud solution, they will meet their regulatory requirements and future-proof their services for success.

As regulators take note, banks should focus on commercial outcomes of fraud investments

The UK was the first country in the world to introduce a payments-specific regulatory body, the Payment Systems Regulator (PSR), with responsibility to oversee payment systems including Faster Payments, which is owned by Vocalink, a Mastercard company. Recently, it was announced that the PSR has proposed for Pay.UK, a recognised operator and standards-setting body for the UK’s retail interbank payment systems (including the Bacs Payment System, the Faster Payment System and the Image Clearing System), to be in charge of enforcing reimbursement of APP fraud, which accounted for 41% of total fraud losses over H1 2022, according to UK Finance. The implications of this new reimbursement scheme for the design and specification of future digital banking platforms are that getting it right could be transformative for victims of fraud because banks are very slow to take action and the process is flawed at present. However, if delivered imperfectly, it may simply create a different set of complexities and failures for customers.

Banks can rely on regulators to tell them the right thing to do and wait for them to act before they adapt their systems to meet new requirements. However, a smarter strategic approach would be to always try and be ahead of the regulator and set the standards for what anti-fraud should be – so driving the agenda rather than looking at it as a problem to fix. Therefore, banks need to ensure their platforms are able to work effectively under this scheme and look at it as a way to improve their platform approach, as otherwise it will just add another layer of complexity. The challenge for institutions is that some current fraud systems used by banks inhibit their ability to meet their wider goals and are inflexible, slow to adapt, and expensive to run. Those banks that focus on gaining both technological and commercial outcomes from their fraud platform investments will pivot to a new position of strength and grow their revenue.

Vendor solutions need to keep pace with regulatory developments to address banks’ needs

A variety of vendor solutions are currently available to help firms address fraud, including those offered by well-established providers and newer fintech entrants who are using a range of approaches including biometrics and behavioral analytics. The expansion of cloud solutions and the desire of players to outsource their fraud detection without the need to develop their own capabilities has also led to a rise in Software-as a-Service (SaaS) cloud deployments. As adoption of solutions using advanced analytics is increasing, vendors should be aware of the need to provide more accountability and transparency for regulators, which not all vendors may have grasped.

Technology vendors view developments in a different way to regulators, with regulators having no complete oversight on what vendors are doing and how they design systems to be compliant. Banks, on the other hand, that are regulated and accountable, have an opportunity to take charge and step in to fill the gap when it comes to the appropriate design and specification of fraud platforms as a preventative measure for having to reimburse victims of fraud in the future.

Banks need to adopt an integrated approach and encourage sharing of data and best practice

Despite economic uncertainty, those banks that can successfully prevent fraud while delivering a strong customer experience will drive higher rates of engagement and loyalty and grow revenue. Banks need to increasingly put modern technology and integrated solutions into practice while sharing real-time attack data with key stakeholders to mitigate fraud threats and improve their chances of success.

As regulators demand more transparency in the way that firms manage fraud, industry collaborations seem like the most robust way to combat the onset of newer methods of financial crime and should be considered as part of a banks’ platform strategy. Though they remain faced with a difficult macroeconomic outlook, banks should look to use technology to not only curb financial crime but to gain a competitive advantage, which is always the best strategy.

About the author

About the author

Ouliana Smith is a senior research analyst in Omdia’s Enterprise IT Financial Services Technology team and has 10 years’ experience in financial services. Since joining Omdia in 2022, she has focused on digital transformation in retail banking and fraud solutions with a strong interest in alternative payments.

Ouliana started her career as an associate analyst with Datamonitor, now GlobalData, a global market intelligence provider, where she specialised in cards and payments before later moving into wealth management.

Ouliana holds a first-class honours degree in mathematics from Coventry University and an upper-second-class honours degree in art history from the Open University.