Open banking: why the time is now for UK banks to act

In a speech at the Innovate Finance Global Summit taking place between 17 and 18 April 2023, City Minister Andrew Griffith MP announced a far-reaching census of companies involved in the broad financial services and technology landscape in the UK.

Commentators were quick to note that this was a much more modest announcement than had been the case at previous iterations of the conference. Gone was the blue-sky thinking and bold, over-reaching promises for fintech in the UK, replaced instead by the announcement of a large administrative task.

It would be a mistake to assume that this represents a backward step for the fintech space in London. A period of data collection, analysis and consolidation might be the most beneficial thing in a challenging market. However, the unrealised potential of open banking and technological innovation combined with a more challenging venture capital (VC) environment as interest rates rise has left investors uninspired, meaning a change in approach may be required.

Is regulation hindering the progress of open banking in the UK?

On 17 April 2023, the Joint Regulatory Oversight Committee (JROC) published its recommendations for the next phase of open banking in the UK. The report covers the ways that open banking might be expanded and improved for the benefit of consumers, businesses and regulators, and the steps that the committee believes are necessary to deliver on that ambition.

However, the report is striking in that it acknowledges that the structure to actually deliver the roadmap is not yet in place. Section 2.2 of the report gets to the nub of the problem – almost all that the committee wants to do through the roadmap requires a mix of primary and secondary legislation to achieve.

The report notes that some pieces of minor and related legislation are before parliament, but that the substantial legislative requirements are not yet tabled, and there is no clear idea of when they will be. Given that there will likely be a general election within a year or thereabouts, and the probability of a change of government is non-trivial, then it leaves the whole roadmap without proper foundations for, potentially, years.

The latest figures from Open Banking Implementation Entity (OBIE) show that both businesses and consumers in the UK made up more than 7 million active users of open banking services in January 2023, of which 1.2 million were first-time users. In March 2022, there were 21.1 million open banking payments, compared to 6.1 million a year previously, representing a growth of 245%.

The challenges of data silos and API integrations

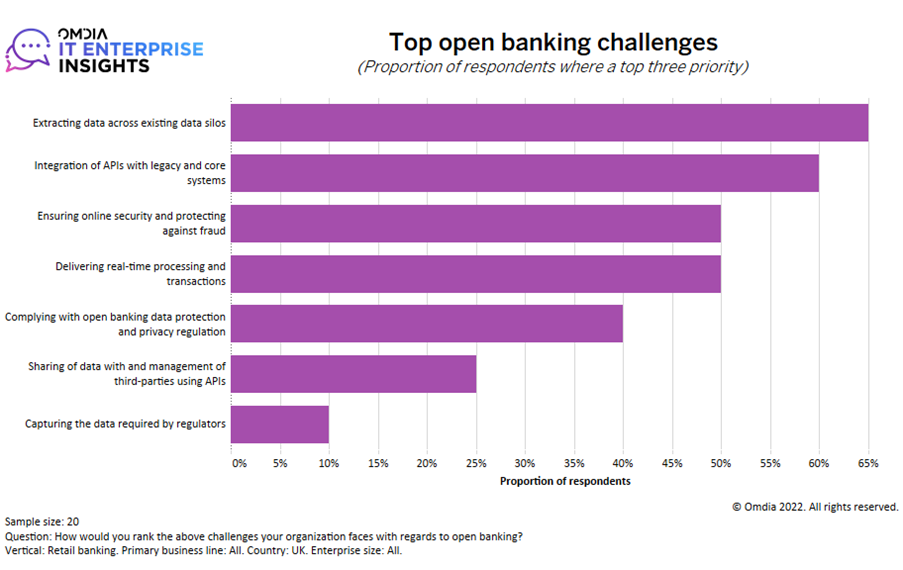

According to Omdia’s IT Enterprise Insights (ITEI) survey, extracting data across existing data silos and the integration of APIs with legacy and core systems are key challenges for open banking overall for 65% and 60% of respondents respectively. Ensuring online security and protecting against fraud as well as delivering real-time processing and transactions are also key concerns for at least half of respondents, as the image below shows.

Our research also found that the majority of UK banks are prioritising quicker product creation and launch to drive investments in their core banking systems rather than supporting their open banking strategy, likely to be driven by the growing desire to be better placed to compete with neobanks.

Top open banking challenges for retail banks in the UK. Source: Omdia IT Enterprise Insights 2022/23 survey

Greater use of the cloud is needed to bring a meaningful change to the finance industry within the new framework of open banking, while also addressing the challenge of data privacy and security. Currently, a lack of global industry standards has given rise to an API security market and collaborations such as the OpenAPI Initiative (OAI) to actively promote standardisation of APIs.

The European Banking Authority’s recent response to a call for advice on the review of Payment Services Directive 2 (PSD2) indicates the direction of open banking as it seeks to explore the possibility of having a common API standard across the EU to be developed by the industry, which is likely to have an impact on the adoption of the initiative in the rest of the world.

There are important decisions to be made that will set the strategy for the industry across the UK

There is a real sense that we’re at a crossroads in the UK – a feeling of ennui and uncertainty. To date, a lot of product innovation in fintech has not really been innovation. It essentially amounts to sticking a digital frontend onto a legacy industry. Therefore, a step up in modernising core banking is required to move the industry ahead with open APIs. In financial services terms, the UK exists in a global ecosystem of emerging payments systems that leverage technology in a multitude of different ways, and the UK needs to be leading that global race.

Given the anticipated growth in real-time payments and open banking use cases, banks should consider next-generation core banking platforms, developed as real-time, API-first and cloud-native solutions, to improve their existing capabilities. What Omdia’s data and the analysis of the open banking roadmap show is that the majority of work needs to go into the backend. Hopefully, the combination of data from the fintech census, the realities of the venture capital environment and the lobbying of the roadmap will push investors and policymakers to drive that agenda forward.

Many companies, therefore, need to have a clear strategic vision of what the future of finance, payments and services will look like, and not have their heads turned by what’s fashionable, the whims of VCs or panic when the banking system comes under stress. As we work with our clients and partners, we see how these challenges and tensions play out, as companies seek to develop a compelling commercial offer in a competitive and heavily regulated market space. In this period of reflection and review of what fintech is all about, companies need to have access to the right data to inform their analysis and make timely decisions.

About the author

About the author

Ouliana Smith is a senior research analyst in Omdia’s Enterprise IT Financial Services Technology team and has 10 years’ experience in financial services. Since joining Omdia in 2022, she has focused on digital transformation in retail banking and fraud solutions with a strong interest in alternative payments.

Ouliana started her career as an associate analyst with Datamonitor, now GlobalData, a global market intelligence provider, where she specialised in cards and payments before later moving into wealth management.

Ouliana holds a first-class honours degree in mathematics from Coventry University and an upper-second-class honours degree in art history from the Open University.