Non-Cash Transaction Growth Surges Worldwide, Surpassing GDP in All Regions (Oct. 6, 2015)

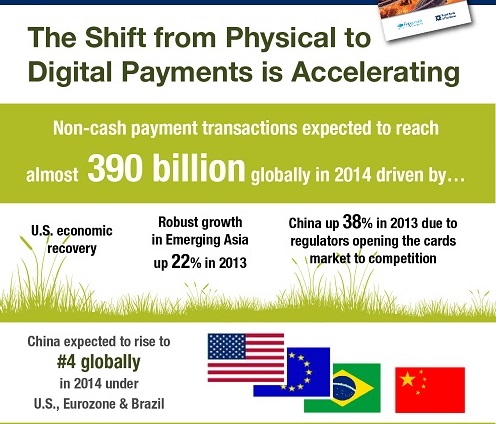

The rise of mobile and contactless payments technology caused non-cash payment volumes to soar last year, surpassing the growth rate of GDP in all worldwide regions, according to a new report from Capgemini and the Royal Bank of Scotland. Non-cash payments in 2014 grew at a rate of 8.9 percent to reach a record high of 389.7 billion transactions, topping 2013’s growth rate of 7.6 percent.

The rise of mobile and contactless payments technology caused non-cash payment volumes to soar last year, surpassing the growth rate of GDP in all worldwide regions, according to a new report from Capgemini and the Royal Bank of Scotland. Non-cash payments in 2014 grew at a rate of 8.9 percent to reach a record high of 389.7 billion transactions, topping 2013’s growth rate of 7.6 percent.

Factors driving growth of non-cash payments last year include the continued economic recovery in developed economies—along with strong economic growth in China—plus the adoption of mobile and contactless payments technology, and the push for faster payments worldwide, the report indicates. In emerging economies in Asia, non-cash transactions are estimated to have grown by 27 percent in 2014, compared with a 22 percent growth rate in 2013. China leapt to fourth position in non-cash payments worldwide in 2014, surpassing Germany, the U.K., France and South Korea.

Nations ranking highest in non-cash transactions for 2014, according to the report, are:

- U.S.

- Eurozone

- Brazil

- China

“Hidden” payments—payments processed via nonbank systems, including closed-loop cards, mobile apps, digital wallets, mobile money services and virtual currencies—now account for about 10 percent of non-cash transactions. This category of payments drove about 40.9 billion non-cash transactions in 2014.

Compared with alternative financial services providers, banks still occupy the best competitive position to efficiently provide customers with a broad array of payments services, if they embrace innovation, according to the report. Adopting same-day or immediate payments could be a key strategic move for banks looking to add value to existing products and drive new business, the report’s authors suggest.

The global push to speed up intra-country and cross-border payments continues, but the interoperability of systems and standards, plus existing regulations in different nations, are major obstacles. Financial regulators in different nations could help break down these barriers by working together and guiding development of standards that could support global interoperability of immediate payments, according to the report’s authors. Blockchain technology also eventually will help to improve payments efficiency by promoting transparency and decentralization, the report concludes.

Click here to see the full infographic.

Related stories:

{kind=link}