Ask the expert: your questions on growing the business answered

Greg Watts, DCP

FinTech Futures is introducing a new fortnightly column, Ask The Expert! The column is designed to provide readers with practical advice on how to grow their businesses.

Greg Watts is our resident expert. He is the founder of Demand Creation Partners, a London-based growth consultancy that helps fintechs and payment firms to scale. He was previously head of market acceleration at Visa Europe.

Have a question? Let us know! Post it in the comments section below, email Greg Watts and/or FinTech Futures’ editor-in-chief, Tanya Andreasyan, or get in touch with Greg on LinkedIn.

QUESTION: How can I better understand and navigate the complexity of the financial services market?

Professionals from fintech start-ups and fast-growing paytechs are often daunted by the complexity of the financial services industry and the prospect of making necessary connections within it.

Having worked in the industry for a number of years, it’s fair to say there are a number of dynamics which need to first be understood.

Open Banking – otherwise known as the European Union’s PSD2 directive – has ushered in a number of new entrants to the market. This column provides a broad summary of the new and traditional players, need-to-know market dynamics, and tips for establishing partnerships.

- First, understand the industry basics.

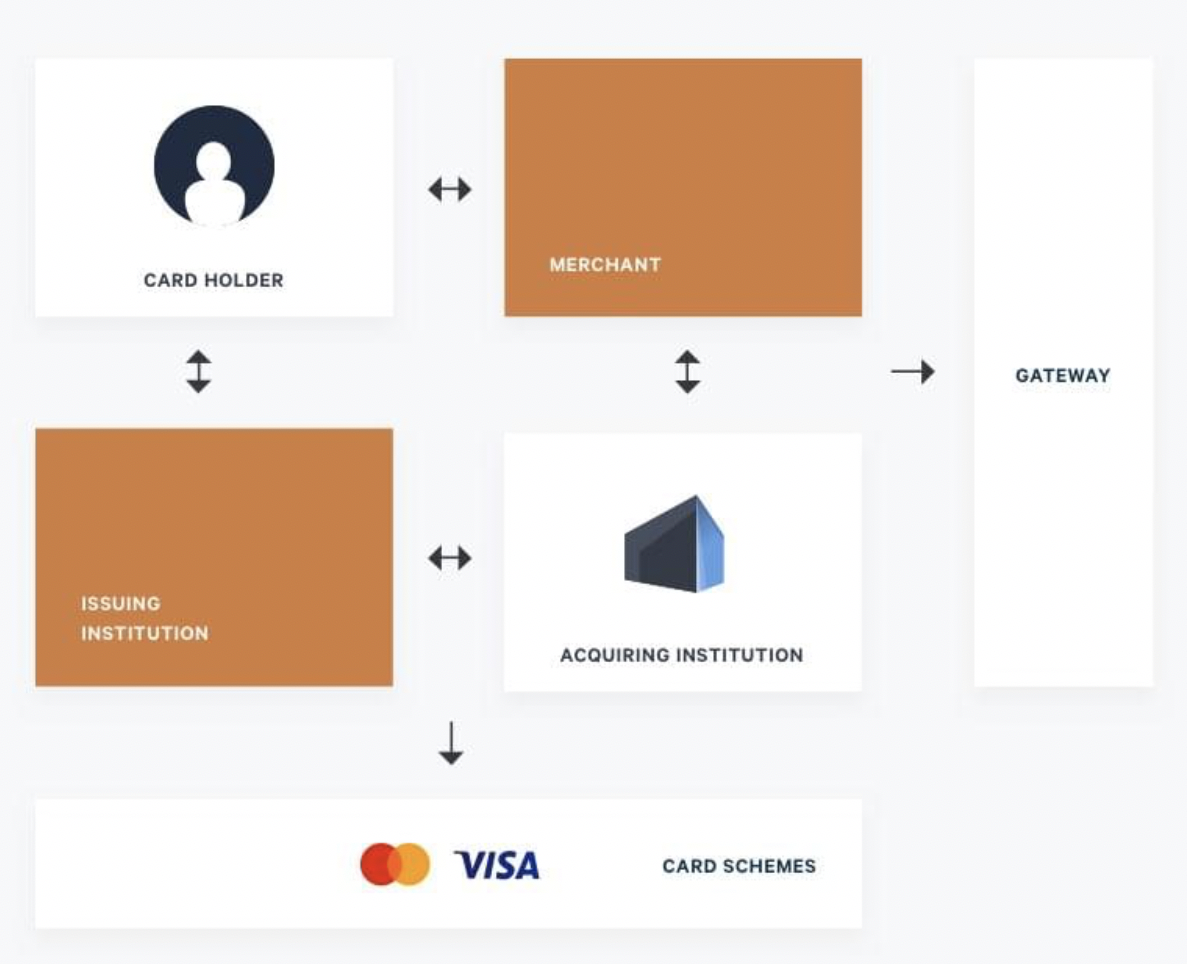

Card processing consists of two main processes: authorisation and settlement. These processes are together known as the “four party model” (referring to the merchant, acquirer, card scheme/network and issuer) and apply to all Visa and Mastercard credit and debit transactions. The processing of other card schemes, such as American Express, is simpler in that the scheme and the issuing bank are the same. This is known as “closed loop” or the “three party model”.

In e-commerce transactions, a fifth party is involved in card processing: the payment gateway supplier. Payment gateway suppliers are positioned between merchants and acquirers. Their role is to capture and send merchant transactions to the acquirer, at which point settlement is made between the acquirer and the merchant.

- Identify key companies to connect with.

There are countless established organisations and new entrants operating within the financial services space. Here are some you should know about:

- The main payment networks are Visa, MasterCard, American Express and Discover. They sit at the centre, facilitating transactions between consumers, merchants, processors and banks. To receive processing information, a fintech will need to build a relationship with one of the networks or work with an aggregator such as Fidel which can potentially provide a quicker route to market.

- Card issuers are financial institutions that provide network payment cards to consumers – for example, an HSBC Visa card. These institutions also issue payments to the merchant bank (or acquiring bank) on behalf of customers. In the UK, card issuers are a mixture of high street brands such as Barclays, HSBC, Lloyds and Santander, and new players such as Monzo, Starling and Tide. (I’ll detail these new card issuers in an upcoming column).

- For merchants to be able to accept payments, they need to work with financial institutions – also known as merchant acquirers. Established players include Elavon, First Data, Ingenico, Paysafe and Worldpay; while newer entrants include iZettle, Square and Stripe.

- Finally, payment gateways provide a secure way for customers to enter payment information such as credit or debit card details onto a website. They encrypt customer data via SSL and work with the issuing bank to determine if the payment can be made (e.g. if the customer has sufficient funds). Payment gateways include Klarna, PayPal, SagePay and Shopify.

Each player has different strengths and areas of expertise, so it’s worthwhile spending time understanding their businesses and identifying potential areas for collaboration or partnership.

- Sign-up to industry news and become a serial networker.

There’s no better way for a fintech or paytech to get to grips with the financial services market than to plunge in and start meeting potential partners, clients and suppliers.

An easy way to start is by following industry news organisations such as Fintech Futures, which provide daily news and insights, along with helpful tools and resources.

In addition, join forums through which you can connect with others. Examples include the Emerging Payments Association (EPA), European Women’s Payment Network (EWPN), and techUK; as well as conferences such as Finovate. These are great places to meet contacts and influencers, build your knowledge and understanding of the industry, and identify new partners and potential clients.

Finally, use LinkedIn to follow key influencers and relevant companies, and to engage stakeholders within them. It’s amazing what an offer of a 30-minute coffee can achieve.

Bringing it all together

Understanding how the financial services industry works can be challenging at first. However, by developing an awareness of the key players and their role in the ecosystem; and understanding how they can potentially add value to your business, you’ll be better equipped for success.

![]() If you have a question for Greg and would like a practical, no-nonsense answer/advice, please get in touch! We’ll be answering your questions in this column – free and open to everyone.

If you have a question for Greg and would like a practical, no-nonsense answer/advice, please get in touch! We’ll be answering your questions in this column – free and open to everyone.

You can post your questions in the comments section below, email Greg Watts and/or FinTech Futures’ editor-in-chief, Tanya Andreasyan, or get in touch with Greg on LinkedIn.