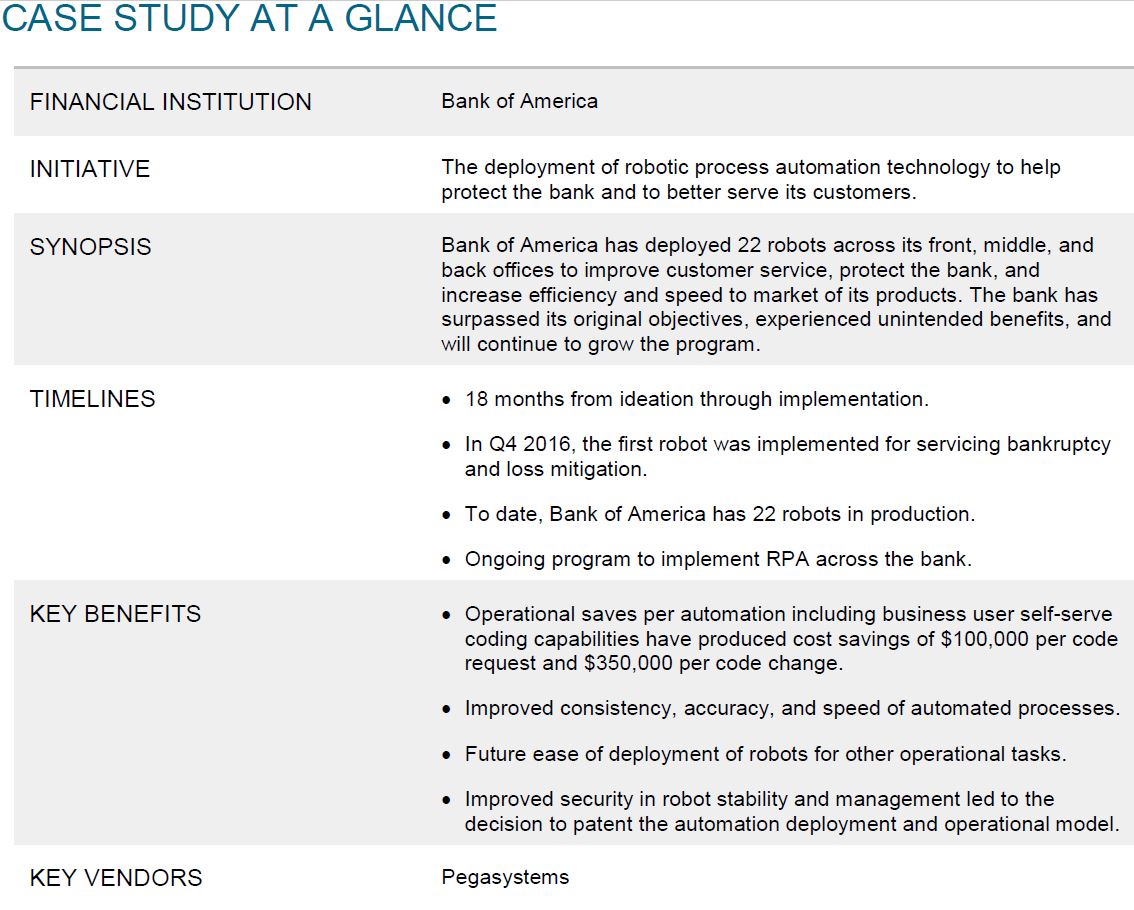

Case study on Bank of America: How robots help serve and protect the bank

Dan Latimore, Celent

Robotic process automation (RPA) is a crunch technology that is relatively easy and quick to implement and promises a strong return-on-investment (ROI), but a recent string of failed RPA projects across the industry has us all resetting our expectations. Launches and pilot projects have become stuck for several reasons – all of which can be avoided.

Dan Latimore, chief research officer at Celent, explores the use of RPA at Bank of America.

It starts with the misuse of the word “process” in robotic process automation. Robots are purposely designed to automate tasks, not to fix end-to-end business processes. Pedantic but an important distinction, because the automation of manual tasks is critical to the streamlining and improvement of end-to-end processes.

- Bank of America’s RPA programme is successful because it is predicated on strong governance and advanced planning, with the ability to make simple changes through development, testing, and when the robot is in production.

- In a bank of this size, there are many potential areas that would benefit from the automation of repetitive tasks that are currently carried out manually. Bank of America has established best practice business and technology criteria that filter and prioritise use cases.

- Bank of America recognises that RPA is a tool within a tool box. Alone, it will not modernise the bank’s processes, but layered on top of a robust foundation it can automate and streamline current burdensome and inefficient processes.

Introduction

Bank of America deployed robots in a challenging environment across multiple use cases, resulting in cost efficiencies, increased productivity, and reduced risks. For a large incumbent bank, Bank of America shows that a culture of innovation, spread across many parts of a large and complicated organisation, can yield impressive results.

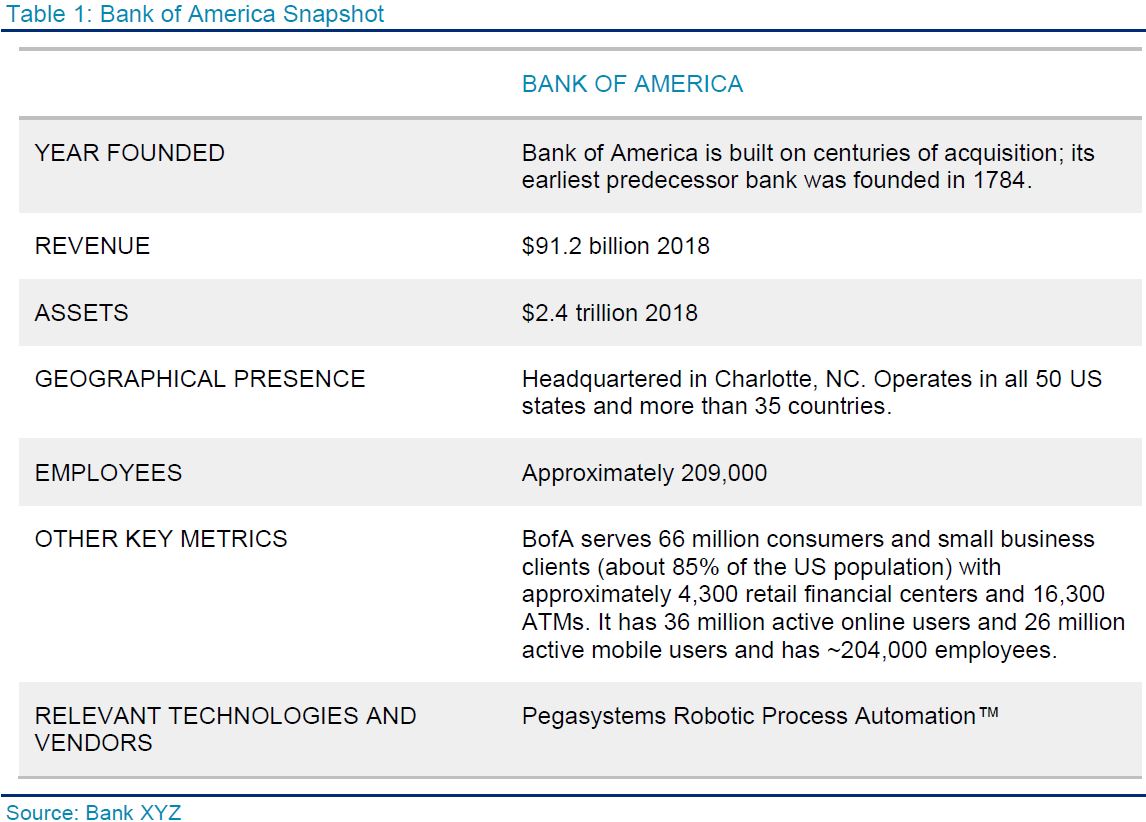

Table 1 gives an overview of the bank.

Since 2010, Bank of America has invested roughly $25 billion in new technology initiatives. Investment is driven by operational excellence – creating efficiency and investment in the future. This includes the reworking of the bank’s major systems and adding innovative capabilities, while also building an internal cloud and software architecture for maximum efficiency and speed to market. Part of the reworking is the upgrade of integration across systems and investment in robotic process automation.

Opportunity

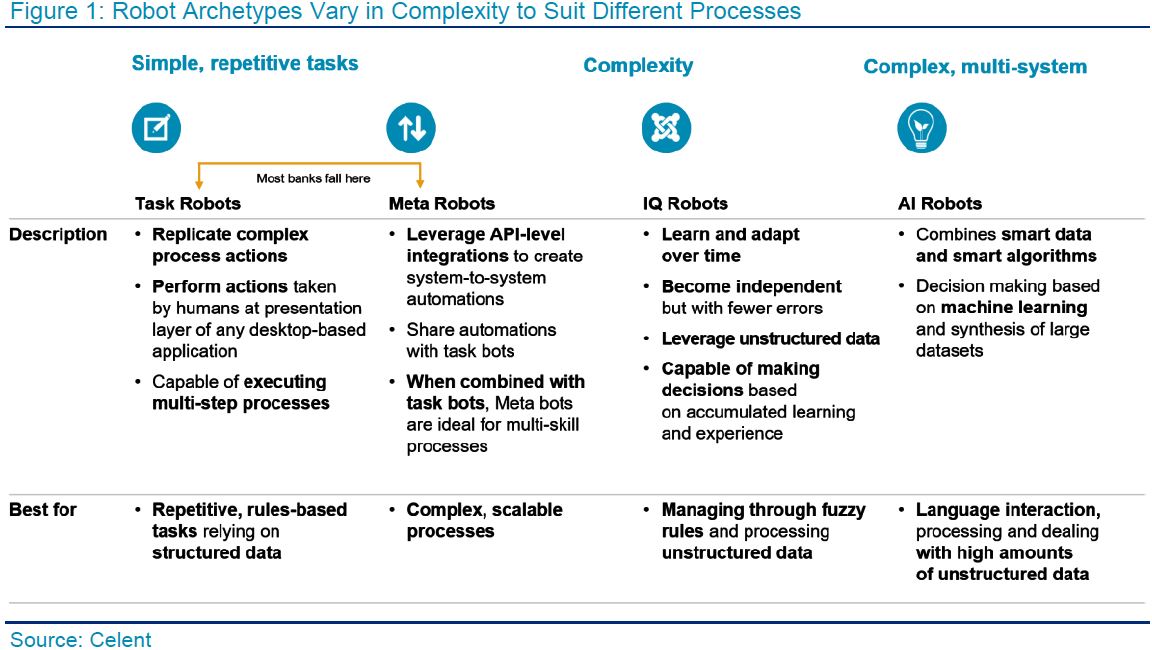

RPA has become a go-to technology across the banking industry. At its simplest, it’s the next generation of automation tools: the application of software-coded scripts governed by business logic and structured inputs that mimic routine user tasks such as interpreting interfaces, transforming data, and initiating and responding to events. At its most complex, it is smart automation powered by algorithms and decision-making, based on machine learning and synthesis of large data-sets.

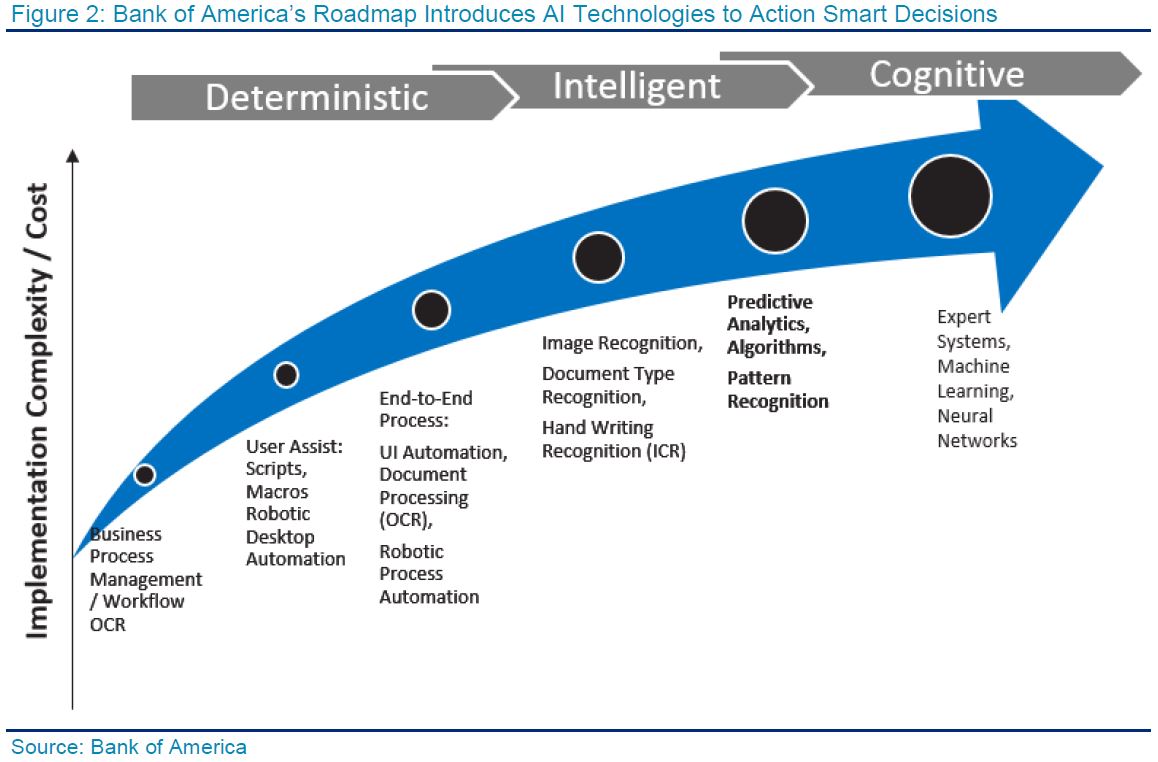

Figure 1 shows the degrees of automation complexity aligned to process complexity. AI-powered RPA is the Holy Grail of process automation. It automates tasks that require algorithms and language interaction on processes of large amounts of unstructured data. Examples of suitable use cases for AI-powered RPA are trade surveillance and communications, transaction triage and data analysis, and the closure of batch false positives. Most banks that have initiated RPA projects fall in the first column and have deployed a basic task robot, while a handful of leading banks have deployed meta-task robots to automate tasks across more complex and scalable processes by leveraging application programming interfaces (APIs).

Although Bank of America only uses task and meta-robots, it has put in place a program that will quickly expand the use of RPA in-house across the front, middle, and back office functions and sets up the bank to be able to introduce machine learning and AI techniques. RPA is proving to be a good jump-off point for the use of AI. There are numerous functions across Bank of America where decisions are reached through data-intensive processes and highly manual repetitive tasks. The bank prioritised RPA as an enabler of business transformation across customer servicing operations, regulatory compliance, and foreign money transactions.

The sponsor of the RPA initiative is Bank of America’s executive for consumer and shared services operations technology group, Prasanna Gopalkrishnan, and the stated objectives are:

- Create more reliable and consistent experience for customers and clients.

- Improve transparency with regulators.

- Increase efficiency and speed-to-market of services and products.

- Reduce operational risk.

- Improve and reduce the cost-to-serve.

- Build capability to expand RPA use cases across business areas.

- Gain knowledge to responsibly move to machine learning and AI-powered RPA.

- Continue to build expertise in Agile methodologies to implement new process quickly and securely.

Solution

Bank of America worked with Pegasystems and deployed its Pega Robotic Automation solution. The solution features robots that interpret applications for processes that involve manipulating data, executing transactions, triggering responses, and handling exceptions. It has a non-invasive object-level integration that equips the bank to bridge legacy systems, close data integration gaps, and wrap legacy system integrations, without making changes to their underlying technology. Using an event-driven approach to automation it integrates with business process management and case management to improve straight through processes and operational efficiencies.

A management console allows the user to orchestrate, manage, and prioritise the queuing of work and processing activity of the software robots. Dashboards, reports, and drill-downs monitor robot health, work status, service-level agreement (SLA) compliance, and auditing. Automation authoring has a visual design surface that makes it easy for Bank of America to create workflows and apply business rules through shapes, or by recording workflows.The ability for businesses across the bank to implement simple changes without having to engage IT represents a considerable saving to the bank. This is particularly important in areas where laws and guidelines are subject to frequent change.

So far, Bank of America has implemented RPA across the following operations, and it intends is to continue to grow the programme:

- Mortgage and vehicle servicing.

- Enterprise Shared Services for exceptions.

- Servicing customers for mortgage and card disputes.

- Foreign money transaction operations and global payments operations.

RPA is most suited to high-volume throughput of structured data, with a clear processing flow that is driven by business rules and does not change frequently. In the most basic case, the employee receives inputs, examines those inputs, applies a rule to them, with no discretion in this scenario, and then sends the output forward to the next step in the process.

The “yes” decision and prioritisation of use cases is made jointly by the business group and by the shared services operations team, which acts as the gatekeeper to what is a practical use case. It is the intent of Bank of America to continue to grow the program and add more robots where there is a business case and the process meets the criteria of the program. Technology qualification requirements for a “Yes” decision are based on the complexity of the following components:

- Activities to be automated.

- Processes.

- Data.

- Transaction volume.

- Technology compatibility.

- Scalability.

Project team and milestones

The project was run by Bank of America’s global technology & operations organisation and involved multiple stakeholder and team members from mortgage and vehicle servicing operations, consumer banking, global information security, and enterprise architecture groups.

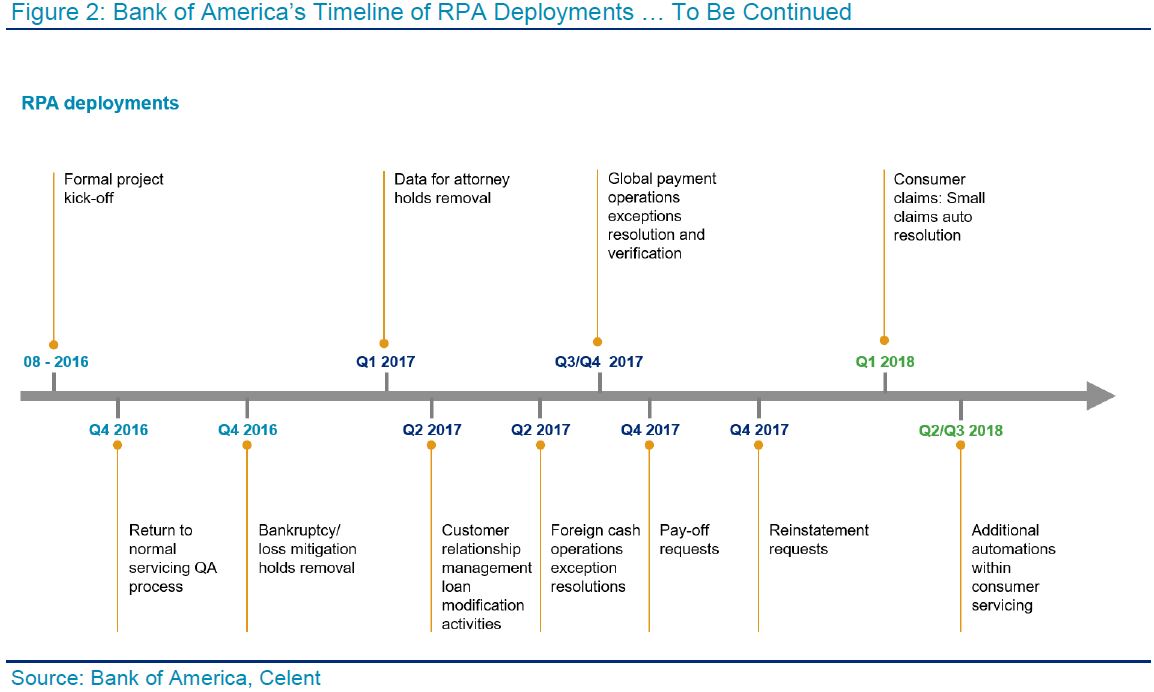

The project took 18 months from the idea’s inception to production, and the formal project kick-off was in 2016. Figure 2 shows the chronology of RPA deployments by the bank.

The fast-paced nature of RPA requires agility, accuracy, and flexibility. The shared operations services team quickly realised that Agile methodologies for development, testing, and deployment of the robots would be the best approach to managing the program. Agile provides full visibility, enables flexibility of constructing software code, and keeps the management of risk at the forefront. Agile also drives short development cycles that deliver incremental, iterative work sequences that work well with the structure of RPA technology.

The use of strong security and deployment model along with Agile deployment practices led the team to make the decision to patent its intellectual property around its lifecycle approach. Furthermore, through the initiative, Bank of America has developed internal knowledge and expertise of RPA techniques that will play well with new AI techniques such as machine learning.

Results, lessons learned and future plans

Bank of America has derived substantial benefits from the ability to reuse RPA, components, design, and methodologies across businesses and different use cases. As a lightweight tool that pulls from the presentation layer of information systems, it does not carry the same risks of full system implementations.

The deployed robots directly integrate into existing infrastructure and don’t require invasive actions to any of the bank’s underlying systems. It doesn’t touch the business logic of the system or the data access layer, and investment levels required are much less than would be needed for full system integration.

The results have simplified its operating environment and improved productivity and efficiency. Its ease of use has meant that business users are trained to configure scripts, and this has reduced the costly dependency on the bank’s IT group for implementation and support. Where robots are in operation the bank has seen a marked improvement in customer service, risk management, and cost reductions.

Immediate qualitative benefits include:

- Greater consistency, speed, and accuracy of key processes across mortgage and vehicle servicing. For example, the bank has implemented higher standard servicing routines for bankruptcy hold removals, payoff and reinstatement requests, and CRM for loan modification activities.

- Within foreign cash operations and global payments operations, RPA has automated wire repaid exceptions and verifications, and data collection for potential anti-money laundering. Again, improving standards, consistency, and speed of operations. Importantly, the ability to extract and manage large amounts of data has lowered the number of anti-money laundering false positive alerts.

- Automating dispute resolutions for mortgage disputes on credit reports, as well as credit card disputes, has improved the experience of its customer, and improved operational efficiencies of the department.

Metrics from the RPA project have also been substantial, and continued improvement of key measurements are expected.

Immediate quantitative benefits include:

- The bank achieved 95% of targeted benefits under budget.

- Within its Enterprise Shared Operations Services group, RPA deployment has reduced manually worked exceptions by 95% and aged exceptions of more than 15 days by 70%. This has resulted in a 40% reduction in manual repairs/workarounds, and defects per million fell from 30 to 0.

- RPA across mortgage and vehicle servicing has reduced the average time taken to service 4,000 cases per month from 20 minutes per case to 4 minutes: 1,975 cases were reduced from 5 minutes to real time, and 5,302 cases were reduced from 2 minutes to real time. This has led to an 89% reduction in the need for manual reviews. The improvement in the mortgage and vehicle services functions was delivered via a single robotic desktop automation for about 300 user desktops. It also reduced per-call savings (24,000 calls per month) by 20%.

- Operational saves per automation including business user self-serve coding capabilities have produced cost savings of $100,000 per code request and $350,000 per code change.

- RPA has reduced customer service call time by 10–15% and ensured compliance.

- Operating hours are far more predictable, and therefore service hours are more manageable, which has led to a reduction in overtime required.

- Notable improvement in error rates by up to 95% manual exceptions on a weekly average.

Future plans

Bank of America believes its initiative has positioned the bank to introduce more advanced technologies such as machine learning and advanced analysis to power its robots. AI-powered RPA is the next stage in the evolution of process automation. Smart process automation (SPA) joins robotics with artificial intelligence (usually machine learning) to enable the automation of workflow tasks that currently require inference and decisions, truly allowing its employees to focus on high-value activities.

Summary

The scope of Bank of America’s initiative is by its nature very large and complex. It was a work in progress to identify potential RPA use cases. Starting from a blank sheet, the Shared Operations Services team was able to plan with strong governance and project management excellence in mind. Adopting such an approach has meant that Bank of America avoided the common pitfalls we are seeing across the first flurry of RPA proofs of concept and launches in banking — poor governance, lack of planning, skunk work, prescriptive controls at launch of the automation initiative, and one-size-fits-all projects. Moreover, the use of Agile methodology is far better suited to RPA than the Waterfall approach. It has created the ability for easy configuration and code changes in an iterative and visible approach.

Bank of America has positioned itself to continue the roll-out of robotic process automation in an efficient, streamlined manner with low risk, and the bank is setting itself up for the same approach to the introduction of more advanced machine learning and AI techniques.

God this is such bs… bofa has has put a mentally deranged robot in charge of everything and now customers cant do anything. everything takes 10 times longer than it used to. God help you if you call and have 2 things to do. They have split departments to the point that none of there staff can do anything, even worse the deranged robot seems to be in charge of the call center. There is no operator, just the dumbest AI on the planet constantly putting the users into 20 minute long menu selections, infinite logic loops or just repeating the same thing at you over and over. After 30 years with BofA, I have closed all my accounts and will continue warning others of their greedy and incredibly stupid and short sites operations.