Santander launches ISA mobile app

Santander has launched the UK’s first standalone ISA mobile app , which was designed and developed with mobile specialist company Monitise.

Santander has launched the UK’s first standalone ISA mobile app , which was designed and developed with mobile specialist company Monitise.

Türk Ekonomi Bankası is to launch a mobile contactless payment application using Visa Europe’s host card emulation functionality to provide secure contactless payments.

Misys has launched a banking app prototype for the upcoming Apple Watch, which is due to launch in April, that allows users to make transactions by speaking at their watch.

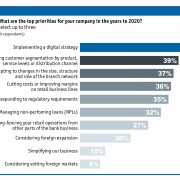

The need for a digital strategy has leapt to the top of retail banks’ agendas over the past year, replacing regulatory issues, as they look to fend of competition from tech and e-commerce rivals.

A company’s Net Promoter Score has become an important measure of customer satisfaction. It asks them a simple question: how likely they are to recommend that company to a friend. The responses split the audience into three groups: promoters, passives and detractors. By subtracting the percentage of detractors from the promoters, banks obtain their NPS. NPS has been a valued metric in many consumer-facing industries for several years, but its importance and influence in financial services is growing fast.

Protecting your banking infrastructure from cybercriminals is one of the toughest IT challenges in banking. It keeps getting harder, even though banks are working tirelessly to protect both customers and assets. Attacks are growing in size, and new developments such as the Internet of Things mean attack surfaces are growing, as well as the number of endpoints that can be used to launch attacks.

As many more tech companies begin offering bank-like services, mainstream banks are searching for ways they can fight back

Britain’s banks have reliably serviced the banking needs of millions of customers for more than a hundred years; providing a safe place to store hard-earned cash, mortgages to buy dream homes, and great interest rates to accumulate savings

For banks, a race to remain relevant is on. In the past few weeks, Lloyds Banking Group has announced its intention to double-down on digital banking, closing branches and cutting costs. In the US, BBVA Compass announced that its agreement with startup Dwolla to offer real-time payment facilities to customers makes it the first mainstream bank to open its technology platform to digital developers like Dwolla

Following its success during the Black Friday and Cyber Monday shopping frenzy this year, alternative currency Bitcoin is gaining popularity and could be poised for major growth in 2015. But the currency still has a long way to go before it catches up with rivals such as PayPal, Visa and MasterCard.

Monitise plans to raise £49.2 million through extensions of its relationships with Santander, Telefónica and MasterCard. The money raised will be used to ‘support the development and accelerated roll-out of its global platform capabilities’.

The time is right for a new breed of digital-only banks to enter the market and steal away share from the established players, according to a new report by Monitise.

Banks will be judged on how well they provide mobile services and social media interaction in the coming years. Instead of being just another channel, these forms will be the first point of contact for customers, according to a new report by analyst firm Celent.

Banks in fast growing and rapidly developing markets have greater ambition to innovate and invest more in research and development on customer experience than those in mature markets, though all are increasing their investments.

As banks develop new retail styles, they face new security challenges as the changing use of space in-store means surveillance and alarm systems must evolve in tandem.

The digital era is changing your bank rapidly. Is your mobile testing & assurance practice ready? P Venkatesh, director of the product division, and Srivatsan TT, vice president of the solutions group, at Maveric Systems discuss the issues

Despite the significant challenges faced by the UK’s banking sector over the last decade, there has been a dramatic evolution in the customer experience following the introduction of online, telephone and mobile banking. While the branch remains an important channel, especially for older customers, mobile technology is rapidly redefining how customers interact with their banks.

Apple may have lined up the chief executives of Bank of America and JP Morgan Chase to laud the launch of Apple Pay, but reaction from the wider industry was more muted – disappointed, even.

With the penetration of mobile devices, such as smartphones and tablets constantly growing, attention is increasingly turning to mobile marketing, mobile commerce and mobile payments. It is still the case, however, that these trends are largely played out in specialised media, and do not influence the actual behaviour of consumers. This is especially true for mobile payments, with consumers very sceptical about this concept

One of the most distinguishing features of the current wave of financial innovation is how the innovators are often not banks, but small fintech firms often led by former bank employees.

Growth in the volume of debit and credit card purchases in the UK continues to outstrip the growth in value as consumers use their cards more frequently for lower value payments. A threefold increase in contactless payments was a factor in the trend.

The UK Government is to examine the potential of digital currencies as positive force in the wider economy and as a means of encouraging innovation in financial services.

After a decade of being the ATM maker you’ve never heard of, Diebold is returning to Europe and a year into his tenure as president and chief executive at the firm, Andy Mattes thinks that the company’s profile is about to change.

Setting up a bank in the UK is costly, time-consuming, heavily regulated and not easy. As a result, the dynamic, start-up culture that drives innovation in many other sectors is less prevalent within banking and financial services.

Analyst firm Juniper Research reckons more people will be using mobile apps for banking than web-based options by 2019, as the 800 million people who used their phones for banking more than doubles to 1.75 billion in five years.

Banks are continuing to spend money on branches, but they are dramatically changing their role to become centres for sale-oriented advice rather than service-oriented transactions, driven by the rapid growth of digital banking.

Banks need to do more to educate consumers about the ways in which they may be exposing themselves to fraud risks, according to a new report by Aite Group using data from ACI Worldwide, which notes that one in four consumers has been victimised by card fraud in the past five years.

The speed at which the mobile market evolves is staggering. Just as we started to look at mobile first, where banks need to align their services and strategies to cater for mobile before desktop or other traditional channels, the notion of mobile-only is now creeping to the fore.

Given that bank customers are unlikely to increase significantly their usage of ATMs and now that opportunities to deploy large numbers of additional dispensers are limited, what does the future hold for the ATM and where does its next phase of growth lie?

The banking industry is complex by its nature but banks and bankers should look up from their budgets, listen to their customers, stop whining about regulations and collaborate on industry issues.

While established banks struggle with their legacy systems, smaller players and new entrants are quickly adopting new technologies – but there are some trends in digital banking that are being slowly adopted by the banking industry as a whole.

Mobility has risen to such a level of importance that many people believe it deserves its own C-level position to advance and align mobility strategy throughout the enterprise. In no other industry is this more pressing than in banking where financial institutions are increasingly using mobile apps to set themselves apart from their rivals.

At the end of last year, Yahoo was hit by a malware attack. It affected over two million clients, mainly in Romania, Great Britain, France, Italy and Spain, putting their personal data at risk. Upon visiting the website between 27 December and 3 January, users received advertisements, some of which were malicious and infected users’ devices without even a click.

Mobile payment isn’t about reinventing the wheel – it’s about making merchants and customers’ lives better by establishing a relationship built on knowledge and trust, according to mobile payments platform Znap.

Bitcoin, gamification and Personal Financial Management are “generating more heat than light” in debates about the future of retail banking and banks should not be distracted from other major challenges including digital channels and legacy transformation.

MasterCard has partnered with mobile technology specialist Syniverse under an audacious plan that aims at nothing less than “bringing mobile financial services to every single mobile user on the planet”.

What do taxis, the weather, mobile wallets and raincoats have in common? They are all potential variables in determining a person’s daily spend – and they provide a great opportunity for banks to use data to save customers money, according to Aman Narain, global head of digital banking Singapore at Standard Chartered.

The acquisition of digital banking specialist IND Group will give Misys access to parts of its rivals’ customer base that it intends to exploit as it develops its offerings in the digital banking channel, while the closer integration of the IND capabilities will also shore up Misys’ defences against encroachment of its own ageing user base.

The likes and dislikes of mobile banking customers around the world suggest that there is an opportunity to expand mobile services globally – but providers need to be careful they are targeting the right information to the right people, according to a new survey by analytics firm FICO.

A new role for CIOs in the banking sector was highlighted at the recent Gartner Symposium: to maintain their future relevance and position, they need to be seen as consultants in the technology space, not just providers.