Rise up women – you can do it, you really can!

Be bolder, take risks, network, and challenge unconscious bias!

Be bolder, take risks, network, and challenge unconscious bias!

It’s important to remember the positives that cryptocurrency and blockchain technology brings to the world.

What if, by treating the core capabilities as utilities we could totally change the game?

Living as a digital nomad certainly has its perks.

How to secure a meeting with a prospect, the difference between demand and lead generation, and more.

Tapping into new source markets is an exciting way forward. But where to start?

Entrepreneurs, local governments and socially minded enterprises spark innovation in their communities.

Exploring the potential impacts of the IoT for insurers and underwriters.

It’s time to stop demanding data, and start asking around instead.

Practical steps and examples of how to deliver differentiated, superior customer experiences.

“Iron Man” – super-powered, not totally automated.

Revolutionising call centres, and harnessing AI to address challenges such as the demise of Libor.

Find your legacy. Find your own flavour of useful. Dust it off. And make it better.

Superyachts, with turnovers of millions, should be viewed as floating multi-million-pound businesses.

Sophisticated technology offers a more cost-effective answer in the long-term.

Collaboration for incumbents is the only way to catch up with the market and become truly consumer-centric.

And I will be able to pay for a surfboard with my new Apple Card.

Practical advice for any fintech wanting to accelerate growth.

The intent is revolutionary. The path is non linear.

Fintech as an industry has a problem with language: namely, we don’t have one.

Four areas where you can make the biggest impact both quickly and in the long run.

A “technological arms race” to digitise processes and drive efficiencies is on!

In the face of mounting competition, financial institutions must go a step further to stand out from the crowd.

Open banking and real-time payments are turning the traditional retail banking model on its head. Are you ready?

But if you try sometimes, you find, you get what you need. And need is bigger than want.

What will happen to bank branches as consumers increasingly go digital?

The trio of financial, actuarial and management reporting: technology revolution or evolution?

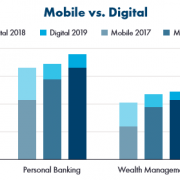

Years of digital transformation are now paying off, with over 57% of worldwide accounts featuring digital capabilities.

Giving constructive, actionable feedback is not easy. But man oh man is it essential.

Cyber risk presents an important test case as to the adaptive capability of insurance industry.

The unprecedented in-depth analysis enabled by graph analytics can produce risk warnings faster and better than ever.

To get the level of interest a fintech needs to be successful, a lot of time needs to be spent focusing on messaging.

So I had to go to the bank today. And the day’s surprises began.

In our rush to digitally transform, it seems we’ve tried to automate the human, rather than humanise technology.

Shaping corporate cultures to be more inclusive and making a positive social impact.

As technology gets more intrinsically tied into the underwriting process, where does that leave human underwriters?

It is key women recognise they hold much more power than they think they do.

Fintechs must stop squabbling with the regulators for real progress to be made.

I have been both a witness to and a participant in a conversation about something going wrong.

Fintechs don’t have to be disruptive to be innovative.